Whistleblower Programs: Building an Effective Compliance Framework

Published on

Nov 13, 2025

16

min read

A whistleblower program is one of the most practical tools a fintech or financial institution can have for identifying risk early. In an industry where compliance gaps can lead to enforcement actions, license revocation, or reputational damage, providing employees and contractors with a trusted means to report misconduct is crucial.

An effective whistleblower program helps surface problems before they reach regulators or the public, protecting both the company and its customers. In recent years, global regulators have made whistleblower protections and reporting mechanisms a central part of corporate compliance expectations.

This article breaks down how to build a whistleblower program that actually works, not just on paper. It explains what regulators require, the challenges that derail many programs, and the practical steps to create one that fits your organization’s scale and risk profile.

Why a Whistleblower Program Matters in Financial Services

For fintechs and financial institutions, compliance is about maintaining trust. A strong whistleblower program reinforces that trust by giving employees and partners a confidential way to raise concerns before they escalate.

A well-designed whistleblower program helps your organization:

Detect issues early: Identify misconduct, policy violations, or control failures before they turn into regulatory breaches. Early detection allows compliance teams to respond before problems affect customers or attract regulators’ attention.

Protect the business and customers: Address problems internally, limiting reputational and financial damage. This approach reduces the risk of external whistleblowing, which often triggers wider investigations and public scrutiny.

Demonstrate governance maturity: Show regulators, investors, and partners that compliance is built into operations. Firms with mature governance structures are viewed as more credible and lower risk, which supports long-term growth.

Encourage transparency and accountability: Build a culture where speaking up is valued and retaliation is not tolerated. Over time, this strengthens ethical decision-making and reduces the likelihood of repeat violations.

Support scalable compliance: Provide a structured process that grows with the organization as it expands across jurisdictions. A well-integrated whistleblower program adapts to new markets, regulatory frameworks, and business models without slowing operations.

In a sector where innovation often moves faster than regulation, a whistleblower program serves as an early warning system. This begs the question:

What Happens When You Don’t Have a Functional Program?

When whistleblowing channels don’t exist or work, problems stay hidden. Employees who feel ignored or unsafe reporting internally often take their concerns directly to regulators or the media.

Once that happens, the company loses control of both the narrative and the outcome. A dysfunctional or poorly managed program can also damage morale, as employees perceive that integrity isn’t valued.

Regulatory investigations triggered by external whistleblowers can lead to larger fines, harsher scrutiny, and long-term reputational damage. For example, SEC whistleblower awards and enforcement activity have surged in the US, often following tips from insiders at financial firms.

Without trusted internal reporting, compliance teams lose a vital source of insight into operational risks, customer issues, and potential fraud. A working whistleblower program helps in maintaining control, credibility, and resilience in a high-stakes regulatory environment.

Regulatory Landscape for Whistleblower Programs

Regulators worldwide have elevated whistleblower programs from optional ethics tools to essential compliance infrastructure. It doesn’t matter where you are in the world; the landscape has evolved in the US, EU, UK, and beyond.

Below is a breakdown of the key US requirements, followed by guidance from other major regulators shaping global expectations.

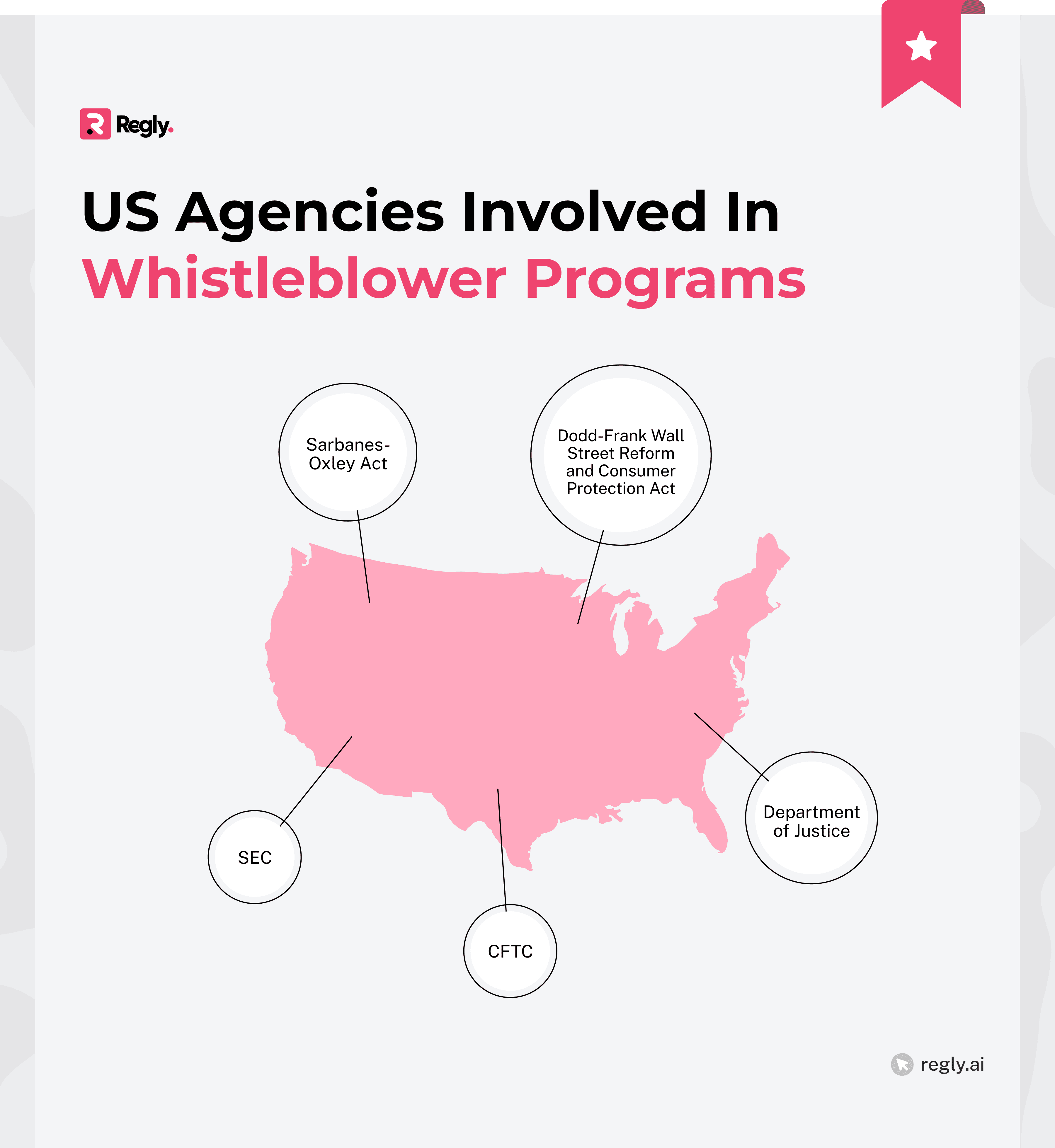

US Requirements

The US has developed one of the most comprehensive whistleblower protection and reward systems in the world. Several agencies oversee these programs, each focused on different areas of financial misconduct.

Together, they form a framework that fintechs must understand and align with. Here are the key players in the regulatory landscape of US whistleblower programs:

SOX

The Sarbanes-Oxley Act of 2002 was the first major federal law to require internal whistleblower procedures. Section 301 mandates that public companies establish confidential and anonymous channels for employees to report accounting or auditing concerns.

For fintechs that are subsidiaries of public holding companies or plan to go public, SOX compliance means formalizing internal reporting mechanisms and anti-retaliation policies. Even private firms often adopt SOX-style structures to demonstrate strong governance and prepare for investor or regulatory scrutiny.

Key points under SOX:

Requires audit committees to create and oversee internal reporting procedures.

Protects employees who report suspected fraud or misconduct from retaliation.

Falls under enforcement by the Department of Labor’s Occupational Safety and Health Administration (OSHA), which handles retaliation claims.

Dodd-Frank

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 significantly expanded whistleblower protections and incentives. It established formal reward programs at the SEC and CFTC, offering 10–30% of monetary sanctions collected in successful enforcement actions.

The law matters for fintechs even if they’re not publicly listed. Many enforcement actions start with insider tips from fintech employees or service providers.

Key points under Dodd-Frank:

Extends anti-retaliation protections beyond SOX to include contractors, agents, and affiliates.

Offers financial incentives for reporting securities and commodities law violations directly to regulators.

Prohibits companies from using NDAs or severance agreements that limit employees’ right to report externally.

SEC

The SEC’s Office of the Whistleblower administers one of the most active programs globally. Since its inception, it has awarded billions to individuals whose tips led to successful enforcement actions.

Fintechs involved in securities, digital assets, or broker-dealer activity fall within the SEC’s oversight. Importantly, the agency also enforces Rule 21F-17, which penalizes companies that obstruct or discourage whistleblowers from contacting the SEC.

Key points under SEC rules:

Whistleblowers may report violations confidentially or anonymously through the SEC’s online portal.

Companies cannot retaliate or require employees to waive whistleblower rights.

In 2024, the SEC fined multiple firms for using confidentiality agreements that restricted employees from reporting potential violations.

CFTC

The CFTC operates a parallel whistleblower program for commodities, derivatives, and certain digital asset markets. Like the SEC, it pays monetary awards for tips that lead to enforcement actions resulting in sanctions exceeding $1 million.

Fintechs offering crypto derivatives or commodities-related products are increasingly subject to this regime.

Key points under CFTC rules:

Covers misconduct in commodity and derivatives markets, including digital asset trading.

Offers confidentiality protections and rewards similar to the SEC’s model.

Has pursued several cases where whistleblower information led to enforcement against trading platforms and intermediaries.

DOJ Guidance

The Department of Justice (DOJ) does not operate a formal whistleblower “reward” program (except under its pilot initiative), but its compliance guidance directly influences corporate expectations.

The DOJ’s Evaluation of Corporate Compliance Programs states that prosecutors assess whether companies have effective, accessible reporting channels and evidence of employee trust in those systems. Since the program was updated in 2024, it remains highly relevant in today’s program.

Key points from DOJ guidance:

Companies are expected to provide confidential and accessible reporting channels.

Prosecutors consider hotline usage, investigation response times, and cultural indicators when evaluating program effectiveness.

In 2024, the DOJ launched a three-year pilot whistleblower awards program, offering financial incentives for individuals who voluntarily report corporate crimes involving financial institutions, sanctions, or bribery.

AML and sanctions whistleblower programs (FinCEN)

The US Treasury’s Financial Crimes Enforcement Network (FinCEN) operates a newer but rapidly expanding whistleblower program focused on anti-money laundering (AML) and sanctions compliance.

Established under the Anti-Money Laundering Act of 2020 and strengthened by the AML Whistleblower Improvement Act of 2022, the program is designed to incentivize insiders to report violations of the Bank Secrecy Act (BSA) and US sanctions laws.

In overview, FinCEN’s whistleblower program:

Applies to a wide range of financial institutions, including banks, money services businesses (MSBs), and crypto platforms registered under the BSA

Protects whistleblowers from retaliation and confidentiality breaches

Encourages reporting of AML, counter-terrorist financing (CTF), and sanctions violations to FinCEN or the Department of the Treasury

Reflects regulators’ growing expectation that fintechs treat AML oversight as a board-level responsibility, not just an operational function

For fintechs handling funds, payments, or digital assets, this program is highly relevant. It covers activities such as weak Know Your Customer (KYC) controls, failures in suspicious activity reporting (SARs), and transactions involving sanctioned entities.

Employees or contractors who provide original information leading to enforcement can receive awards of up to 30% of collected penalties. FinCEN’s approach mirrors the SEC and CFTC models but extends to areas fintechs often find complex, including:

Cross-border transactions

Beneficial ownership verification

Sanctions screening

In practice, the program underscores a clear trend: regulators increasingly rely on insiders to identify compliance gaps in fintechs operating in high-risk or emerging markets.

FINRA, Investment Advisor, and Broker-Dealer Expectations

For firms registered with the Financial Industry Regulatory Authority (FINRA) or operating as investment advisers or broker-dealers, whistleblower programs play a direct role in maintaining supervisory and compliance standards.

While FINRA does not impose a specific rule requiring internal hotlines, it expects member firms to maintain mechanisms that allow employees to escalate compliance concerns without fear of retaliation.

In practice, FINRA views internal reporting as a sign of strong supervision. Firms that ignore internal warnings or fail to investigate misconduct risk violations of

Rule 3110 (Supervision)

Rule 2010 (Standards of Commercial Honor and Principles of Trade)

The regulator’s Office of the Whistleblower also accepts tips directly from employees, meaning any gap in your internal process can quickly become an external enforcement lead.

Investment advisers and broker-dealers registered with the SEC face similar expectations. Examiners often review how firms document, investigate, and resolve internal complaints. When a whistleblower tip exposes compliance failures that the firm knew or should have known about, penalties are typically higher.

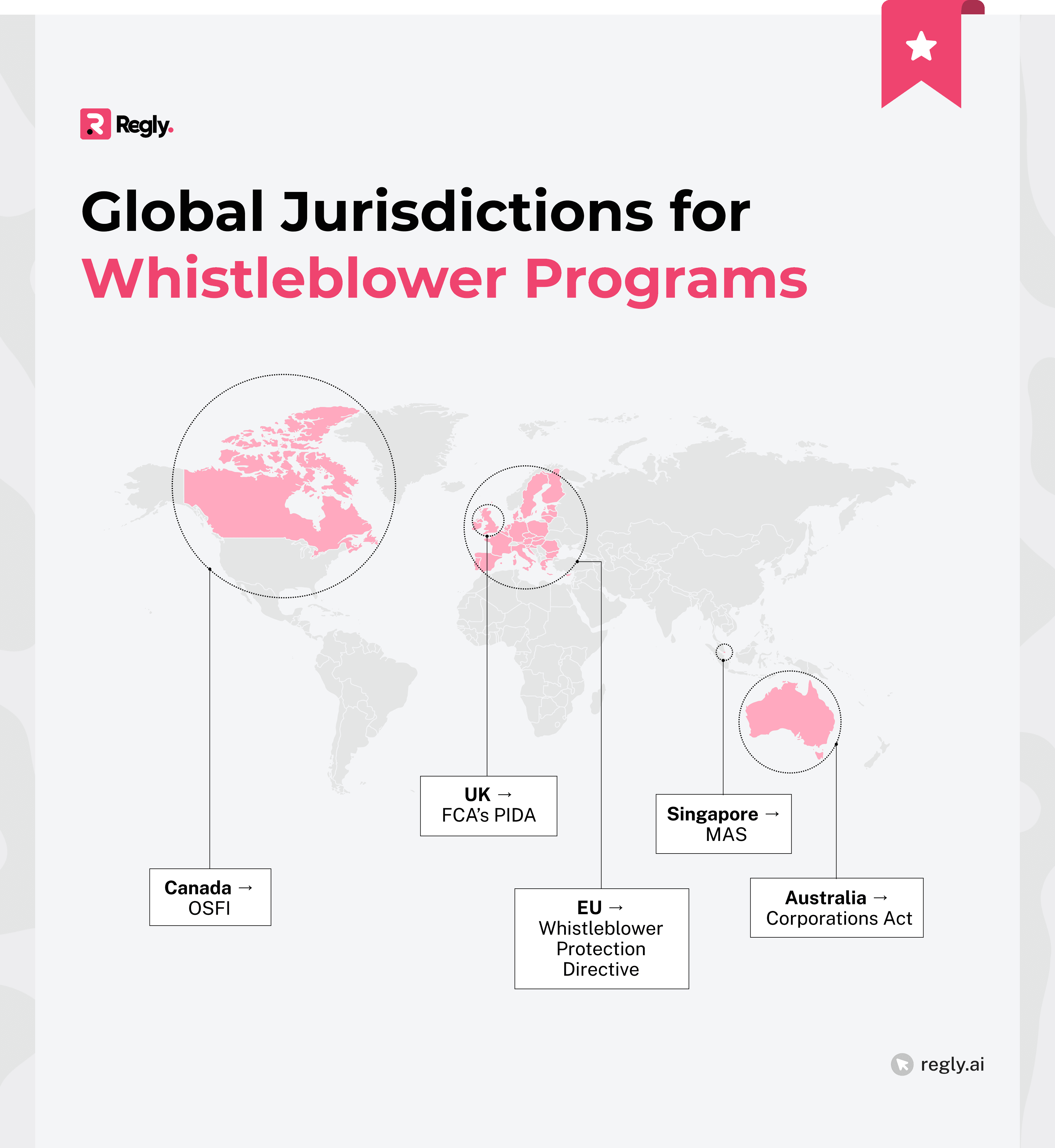

Global Framework

Outside the US, several major jurisdictions have adopted detailed whistleblower protection frameworks. If you are operating internationally, understanding these frameworks helps you maintain consistent compliance standards and avoid fragmented reporting structures.

European Union

The EU Whistleblower Protection Directive (2019/1937) requires companies with 50 or more employees to establish internal reporting channels. Reports must be acknowledged within seven days and provide feedback within three months.

Whistleblowers are protected from retaliation, and breaches can lead to administrative penalties. For fintechs with EU operations, this means building formal, confidential channels and ensuring data handling complies with the General Data Protection Regulation (GDPR).

United Kingdom

The UK’s approach combines the Public Interest Disclosure Act (PIDA) with the Financial Conduct Authority (FCA) whistleblowing rules. Large financial firms must appoint a “whistleblowing champion” at the board level and maintain clear internal reporting procedures.

Even fintechs outside the FCA’s direct scope benefit from aligning with these standards, as they demonstrate proactive compliance and strengthen investor confidence.

Australia

Australia’s corporate whistleblower regime, updated in 2019, mandates written whistleblower policies for public and large proprietary companies.

It extends protections to employees, contractors, and suppliers, covering disclosures of misconduct, breaches of law, or unethical behavior. Regulators emphasize confidentiality, non-retaliation, and prompt investigation, setting expectations similar to US and EU standards.

Canada

Canada’s system is fragmented but evolving. Securities regulators and the Office of the Superintendent of Financial Institutions (OSFI) protect employees who report misconduct within federally regulated financial institutions.

While there’s no single nationwide whistleblower law, fintechs operating under Canadian oversight are expected to maintain internal channels that meet regulatory best practices.

Singapore

The Monetary Authority of Singapore (MAS) encourages firms to maintain confidential internal reporting systems as part of good governance.

MAS guidelines emphasize accountability and board oversight, requiring firms to handle reports objectively and protect whistleblowers’ identities. For fintechs in Asia, these standards offer a practical model for establishing a culturally and operationally appropriate reporting process.

Aligning confidentiality rules, retaliation protections, and investigation timelines across jurisdictions not only reduces regulatory risk but also signals strong governance to partners and regulators alike.

What Regulators Expect from an Effective Whistleblower Program

Regulators don’t just want companies to have whistleblower policies. They want to see that those programs actually work. They expect firms to provide accessible reporting channels, prevent retaliation, and take demonstrable action when concerns are raised.

For fintechs, we can break down these expectations into five key elements:

Confidential and Anonymous Reporting Channels

Regulators expect companies to maintain secure systems that allow employees and third parties to report concerns without revealing their identity. This includes hotlines, web portals, or third-party providers that support anonymity and multilingual access.

An effective program also makes these channels visible; employees should know how to use them and trust that their identity will be protected. Examiners frequently review how these systems are promoted internally and whether staff actually use them.

Anti-Retaliation Protections

Every major regulatory framework emphasizes non-retaliation. The SEC, CFTC, DOJ, and EU authorities all require that whistleblowers be protected from dismissal, demotion, harassment, or discrimination after making a report.

Fintechs should formalize these protections in policy and practice. This includes investigating alleged retaliation promptly and taking corrective action against those responsible. Regulators increasingly view retaliation as a separate compliance failure and have imposed penalties for it.

Evidence of Employee Compliance Trust

A whistleblower program that no one uses is a red flag. The DOJ and SEC routinely assess program “effectiveness” by reviewing usage data, employee compliance surveys, and investigation outcomes.

Healthy programs show consistent internal reporting activity because they feel safe speaking up. For fintechs, tracking reporting patterns across departments can help identify cultural or operational weaknesses early.

Investigation and Remediation Protocols

Regulators want to see that every report is logged, reviewed, and acted upon. That includes defining who reviews allegations, how independence is maintained, and how outcomes are documented.

Strong programs categorize reports by risk level, set investigation timelines, and escalate serious issues to compliance leadership or the board. Regulators often request evidence of this process during examinations, especially if a firm is already under investigation.

Data Handling and Recordkeeping Expectations

Whistleblower data must be protected like any other sensitive information. Regulators expect firms to restrict access to reports, secure evidence, and comply with applicable privacy laws like GDPR.

Maintaining consistent documentation via report logs, investigation notes, and outcomes also supports defensibility during audits or enforcement reviews. For multinational operations, harmonizing data handling across jurisdictions helps demonstrate both diligence and control.

Common Challenges and Misconceptions

Even with a formal whistleblower program in place, many firms struggle to make it effective in practice. Common challenges usually stem from cultural barriers, resource constraints, or simple misunderstandings about what a whistleblower program should achieve.

Recognizing these pitfalls is the first step to building a system that people actually use and trust:

“We’re Too Small to Need This”

Smaller firms often believe that whistleblower programs are only necessary for large corporations. In reality, early-stage companies face equal, if not higher, compliance risks due to lean teams and rapid growth.

Even a simple reporting channel, like a confidential email managed by compliance or an external ombuds provider, can protect the firm from reputational and regulatory fallout. Establishing this process early also sets the tone for transparency as the company scales.

Confusing Anonymity With Confidentiality

Anonymity means a report is submitted without revealing the reporter’s identity. Confidentiality means the person’s identity is known but protected. Fintechs sometimes conflate the two, which can erode trust.

Best practice is to offer both options: anonymous reporting for those who prefer complete privacy, and confidential reporting for employees who are comfortable being identified. Either way, the company must communicate how each type of report is handled and protected.

Mistaking “No Reports” for “No Problems”

A quiet hotline doesn’t always signal a healthy culture. More often, it indicates employees don’t trust the system or fear retaliation. Regulators like the DOJ view a lack of reports as a potential red flag during examinations.

Regular awareness campaigns, leadership communication, and feedback loops help normalize reporting. When employees see that reports lead to fair investigations and real outcomes, participation rises naturally.

Retaliation Risks and Subtle Forms of Punishment

Retaliation isn’t always as clear as firing someone. It can look like exclusion from projects, poor performance reviews, or a stalled promotion. Even small acts of retaliation can undermine the entire program.

Fintech leaders and managers should be trained to recognize these behaviors and avoid them. Clear anti-retaliation clauses, anonymous reporting of retaliation, and consistent disciplinary measures reinforce a culture where employees feel protected when they speak up.

Failing to Close the Loop With Whistleblowers

When whistleblowers never hear back, trust declines quickly. Even if the investigation outcome can’t be shared in detail, acknowledging the report and confirming that action was taken matters.

Follow-up communication shows employees their concerns are taken seriously. It also signals organizational maturity, which regulators increasingly associate with strong compliance governance.

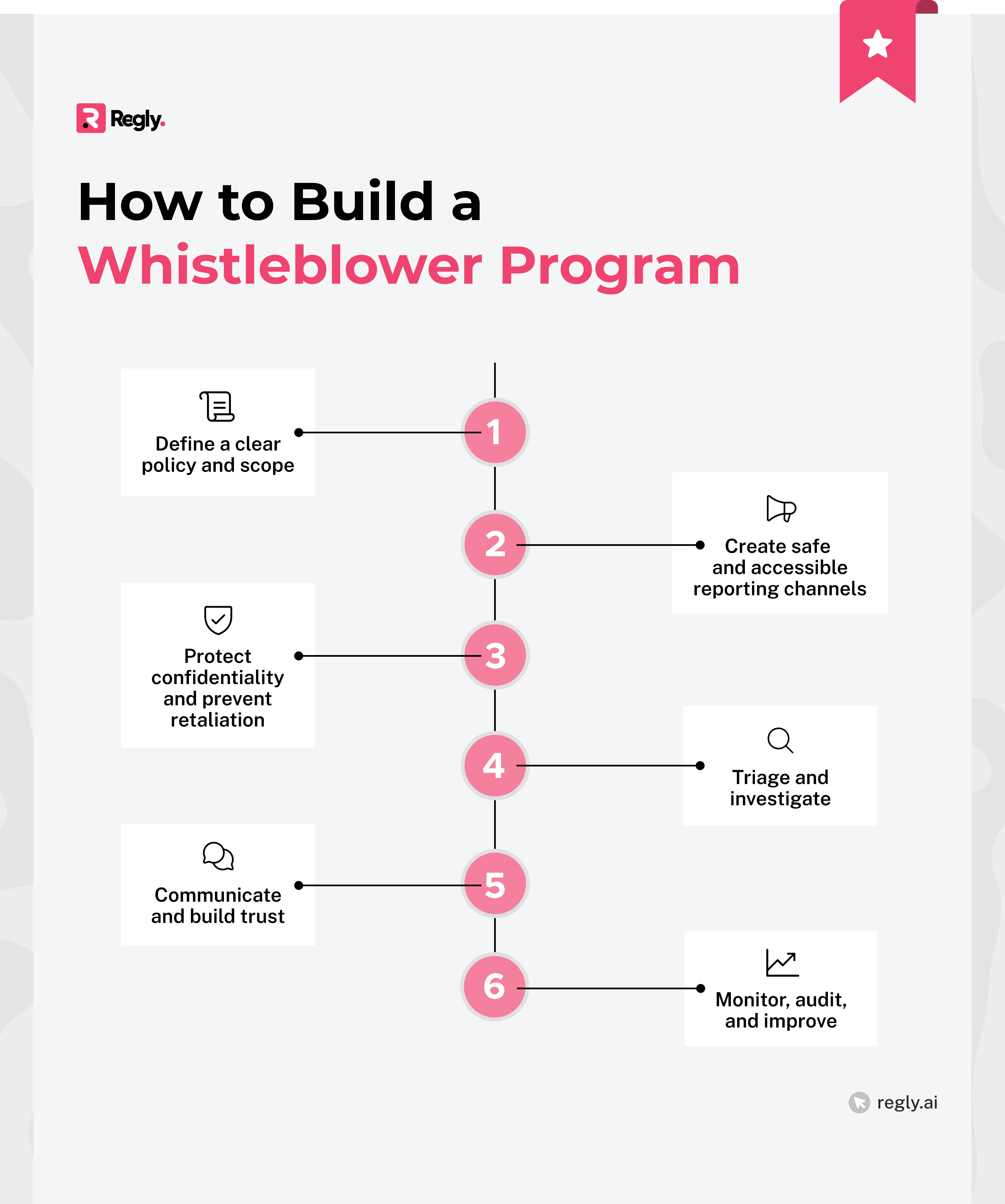

How to Build a Whistleblower Program for Your Firm

A strong whistleblower program doesn’t have to be complicated. What matters most is that it’s practical, accessible, and trusted. These six steps outline how fintechs and financial institutions can create a program that works in practice:

Step 1: Define a Clear Policy and Scope

Your whistleblower policy is the foundation of the entire program. It should explain who can report, what can be reported, and how reports are handled.

A good policy:

Defines reportable issues clearly (e.g., fraud, regulatory breaches, data misuse, unethical behavior)

Explains where reports go, whether to compliance, HR, or an external provider

States how investigations will be handled and how confidentiality will be maintained

The policy should also include whistleblower rights and legal disclosures. This means acknowledging employees’ right to report externally to regulators like the SEC or FinCEN and prohibiting any contractual language that limits that right. Clarity and transparency at this stage set the tone for trust later.

Step 2: Create Safe and Accessible Reporting Channels

Multiple, easy-to-use reporting options increase participation. Fintechs can use hotlines, encrypted web portals, dedicated email addresses, or external reporting vendors. What matters is that employees believe the system is secure and free of bias.

Consider offering:

Anonymous and confidential reporting options

24/7 accessibility through online or phone platforms

Language support for international teams

If your company operates in more than one jurisdiction, you should develop a reporting process that complies with local laws such as the EU Whistleblower Directive or GDPR. Accessibility and visibility are key. If employees don’t know where or how to report, the system won’t be used.

Step 3: Protect Confidentiality and Prevent Retaliation

Every program must guarantee that whistleblowers are protected from retaliation in all forms: direct or subtle. To make this real, train managers and executives on how to respond to reports and interactions with reporters.

Fintechs should document a clear procedure for investigating retaliation claims. Retaliation reports should be prioritized and reviewed independently from the business unit involved.

Reinforce protection through consistent communication: emphasize in training sessions, policy updates, and leadership messages that retaliation will not be tolerated. Culture matters as much as procedure here.

Step 4: Triage and Investigate Effectively

Not all reports carry the same level of risk. A structured triage process helps allocate resources efficiently while maintaining fairness. Assign a responsible team or committee to review each case objectively. This can be your compliance, legal, or internal audit team.

Best practices for triaging include:

Logging every report in a secure system

Categorizing cases by risk and urgency

Setting clear investigation timelines

Escalating serious matters to senior leadership or the board

When the investigation concludes, document findings and corrective actions. Regulators often request evidence that each report was tracked, investigated, and resolved. Proper documentation also helps identify recurring issues or process weaknesses.

Step 5: Communicate, Train, and Build Trust

Awareness drives participation. Communicate your whistleblower program frequently through onboarding, internal communications, and compliance training.

Training should cover how to report, what protections exist, and what happens after a report is made. Include examples and simple language; employees shouldn’t need legal expertise to understand the process.

Leadership visibility is essential. When senior executives endorse the program and talk openly about ethics and transparency, employees are more likely to trust it. Consistent, human communication helps turn policy into culture.

Step 6: Monitor, Audit, and Improve

A whistleblower program requires continuous evaluation. Some of the key metrics you can track in this process are:

Metric to Track | What They Show |

|---|---|

Number of reports | Indicates employee trust and engagement. A consistent reporting flow suggests people feel safe using internal channels. |

Response times | Reflects how quickly the compliance team acknowledges and investigates reports. |

Resolution outcomes | Shows how effectively the company addresses issues, identifies root causes, and applies corrective actions. |

Repeat report trends | Highlights recurring issues or departments that may need additional oversight, training, or policy review. |

Retaliation complaints | Measures the effectiveness of anti-retaliation policies and whether employees feel genuinely protected after reporting. |

In light of these metrics, look for trends that reveal deeper issues, such as repeated concerns from one business line or location.

Periodic audits, either internal or third-party, help assess whether procedures are being followed and whether employees still trust the system. Use findings to adjust training, policies, or reporting tools.

Regular review signals to regulators that compliance is a living, evolving part of the organization. For growing fintechs, this approach keeps the program aligned with both operational reality and regulatory expectations.

Tips for Creating Your Whistleblower Program

While building a whistleblower program, fintechs can make the process efficient, credible, and sustainable.

These practical tips can help fintech founders, compliance officers, and legal teams strengthen their programs and keep them adaptable as the company grows.

Align Your Program With Your Risk Profile

Your whistleblower framework should reflect your specific business model and regulatory exposure. A payments company, a broker-dealer, and a crypto platform each face different risks and reporting priorities.

Start by mapping the areas most vulnerable to misconduct and tailor your policy and training accordingly. These key areas are often:

Customer onboarding

Data security

Aligning the program with your risk map makes it more relevant and effective.

Integrate Whistleblowing Into Compliance Workflows

A whistleblower program works best when it’s part of the broader compliance ecosystem. Connect reporting channels with existing tools such as case management systems, compliance dashboards, or risk registers.

This integration allows for better tracking, analytics, and escalation. It also helps compliance teams identify recurring themes, such as gaps in customer due diligence or sales supervision, and address them proactively.

Turn Internal Reporting Into a Competitive Advantage

Strong compliance governance builds credibility with investors, regulators, and clients. When employees feel empowered to report issues internally, the organization detects risks early before they reach regulators or the press.

Highlighting a robust whistleblower program can also strengthen due diligence narratives during licensing, audits, or fundraising rounds. It shows that your company approaches compliance as a strategic function, not an administrative burden.

Key Takeaways

A strong whistleblower program is both a compliance requirement and a business asset. It helps fintechs identify issues early, strengthen governance, and build a culture of accountability.

The most effective programs are simple, trusted, and integrated into daily operations. They make it easy to report, protect confidentiality, and act quickly on findings.

For fintechs ready to take that next step, Regly can help. Built by compliance experts who’ve supported hundreds of fintechs, Regly’s platform can help automate your reporting workflows, track investigations, and embed compliance into day-to-day operations.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.