Compliance reporting is becoming more complex. Reporting volumes are increasing, timelines are tightening, and compliance teams are often asked to do more with fewer resources. As fintech products evolve and regulatory obligations expand, manual reporting starts to slow teams down and create unnecessary risk.

At the same time, regulators have made it clear that automation doesn’t change accountability. Reports still need to be accurate, complete, and subject to meaningful human oversight. Tools can support the process, but they shouldn’t replace regulatory judgment or governance.

In this guide, we’ll break down what automating compliance reporting involves, how fintechs are using it in practice, and what US regulators expect to see during exams. We’ll also cover common mistakes and practical ways to automate without creating new risks.

What Does Automating Compliance Reporting Involve?

Automating compliance reporting is all about using technology to handle parts of the reporting process that are repetitive, time-sensitive, or data-heavy.

Instead of pulling information manually from multiple systems, teams rely on rules, workflows, and integrations to:

Collect data

Apply regulatory logic

Generate reports on a recurring basis

This often means automating routine tasks such as:

Filling in Suspicious Activity Reports (SARs) and Currency Transaction Reports (CTRs)

Generating trade surveillance reports

Preparing regulatory filings

Creating dashboards or exception reports for internal review

For example, rather than compiling an AML report in a spreadsheet every month, transaction data can be pulled directly from core systems, flagged based on predefined criteria, and routed to a reviewer before submission.

Automation doesn’t replace people, and it isn’t supposed to. The best setups use software to handle the heavy lifting, like collecting data and spotting potential issues, while humans stay in charge of judgment calls, escalations, and final approvals.

This means that if a transaction is flagged, a person should still review the context. When a report is generated, someone should check it before it’s sent.

How Are Fintechs Using Compliance Reporting Automation in Practice?

Most fintechs don’t automate everything at once. They usually start with reports that are frequent, repetitive, and governed by clear rules. The focus is on reducing manual work without changing who makes the final decisions.

Common use cases of compliance reporting automation include:

AML transaction monitoring and reporting: As payments, trades, or wallet transactions move through your systems, automated monitoring rules look for unusual patterns. When something stands out, compliance reviews the alert, adds context, and decides whether to file a SAR or escalate the issue internally.

Alert review and prioritization: Automation helps prioritize alerts and organize supporting data, so reviewers spend less time sorting through noise and more time assessing risk and documenting decisions.

Broker-dealer and advisor reporting: Trade reporting, best execution reviews, and supervisory reports all pull data from different corners of your tech stack. Rather than piecing that together manually, fintechs route it into a single workflow where exceptions get flagged automatically. Reviews move faster, and you get more consistency across the board.

Ongoing supervisory oversight: Automated exception reports help supervisors track patterns like repeated rule breaches, trading outside parameters, or delayed reviews without manually compiling weekly or monthly reports.

Internal management and board reporting: Compliance dashboards and recurring management reports can be generated on a schedule, giving leadership visibility into risk trends without adding extra work for compliance teams.

Across all of these examples, the approach is the same. Automation handles volume and consistency, while people handle judgment and escalation. The strongest setups support existing compliance processes rather than trying to replace them.

What US Regulators Expect From Compliance Reporting Automation

US regulators don’t expect firms to avoid automation. They, however, do expect firms to understand how it works, control how it’s used, and stay accountable for the outcomes. When automation touches compliance reporting, examiners focus less on the tool itself and more on the results it produces and how teams oversee it.

Here’s what US regulators expect from compliance reporting automation.

Accuracy, Completeness, and Timeliness

Automation doesn’t change the basic expectations around compliance reporting. Regulators still expect reports to be accurate, complete, and submitted on time, regardless of how they’re generated.

This means automated reports should:

Pull in the right data

Apply the right regulatory logic

Accurately reflect everything that needs to be reported

For example, an automated SAR process still needs to capture all relevant transactions, not just the ones that fit clean thresholds. If data is missing or logic is too narrow, automation can create gaps just as easily as manual work.

Timeliness matters just as much. If an automated system delays alerts, batches reports incorrectly, or fails without being noticed, the firm is still responsible. Regulators will look at how teams monitor report generation, handle exceptions, and confirm that deadlines are consistently met.

Human Oversight and Decision-Making

Regulators expect people to stay involved, even when reporting is automated. Technology can surface issues and prepare reports, but it shouldn’t be making final compliance decisions on its own.

A common example is alert review. An automated system might flag a transaction or trading pattern, but a compliance professional still needs to review the context, document the reasoning, and decide what happens next. That review trail matters just as much as the alert itself.

Examiners often look for clear evidence of oversight. They’ll want to see:

Who reviews reports

How often reviews happen

What steps are taken when something looks off

If automation removes visibility or makes it hard to explain decisions, it’s usually a red flag.

With Regly’s employee compliance tool, teams can assign report reviews, collect attestations, and document approvals so oversight and accountability are clear during exams.

Technology-Neutral But Outcome-Focused Rules

Most US regulators don’t mandate specific tools or technologies for compliance reporting. They focus on whether the reporting outcomes meet regulatory expectations, not on how the work gets done.

That means two firms can use very different systems and still be held to the same standard. For example, one fintech might use custom-built workflows while another relies on a third-party platform. If both produce accurate, timely, and well-documented reports, regulators generally don’t care which approach was used.

This is where some teams start to struggle. Choosing a modern tool doesn’t automatically make a process compliant. Regulators will still ask how rules are applied, how changes are managed, and how teams know the system is working as intended.

Audit Trails and Supervisory Controls

When compliance reporting is automated, regulators expect clear audit trails. They want to see:

What data was used

How decisions were made

Who reviewed the output at each step

For example, a report that’s automatically generated should have a corresponding record that shows when it was created, what data sources were pulled in, and who reviewed or approved it. Updates should be logged with an explanation. The fact that a record is incomplete or doesn’t exist at all will be questioned more than what’s on the record itself.

Supervisory controls matter just as much. Regulators look for defined review roles, escalation steps, and periodic checks to confirm the system is working as expected. Automation should make supervision easier, not harder to explain during an exam.

Escalation Pathways for High-Risk Cases

Automation can help surface risk faster, but regulators still expect firms to know what happens next. High-risk alerts and reports should follow clear escalation paths that are easy to understand and consistently applied.

For example, if an automated system flags suspicious activity or a serious supervisory issue, there should be defined steps for review, approval, and senior involvement when needed. That might include routing the case to a designated compliance lead, documenting the decision, and tracking follow-up actions.

Examiners often look for gaps here. If alerts sit unresolved, get routed inconsistently, or lack clear ownership, automation can actually increase risk. Clear escalation workflows help show that automation supports judgment instead of replacing it.

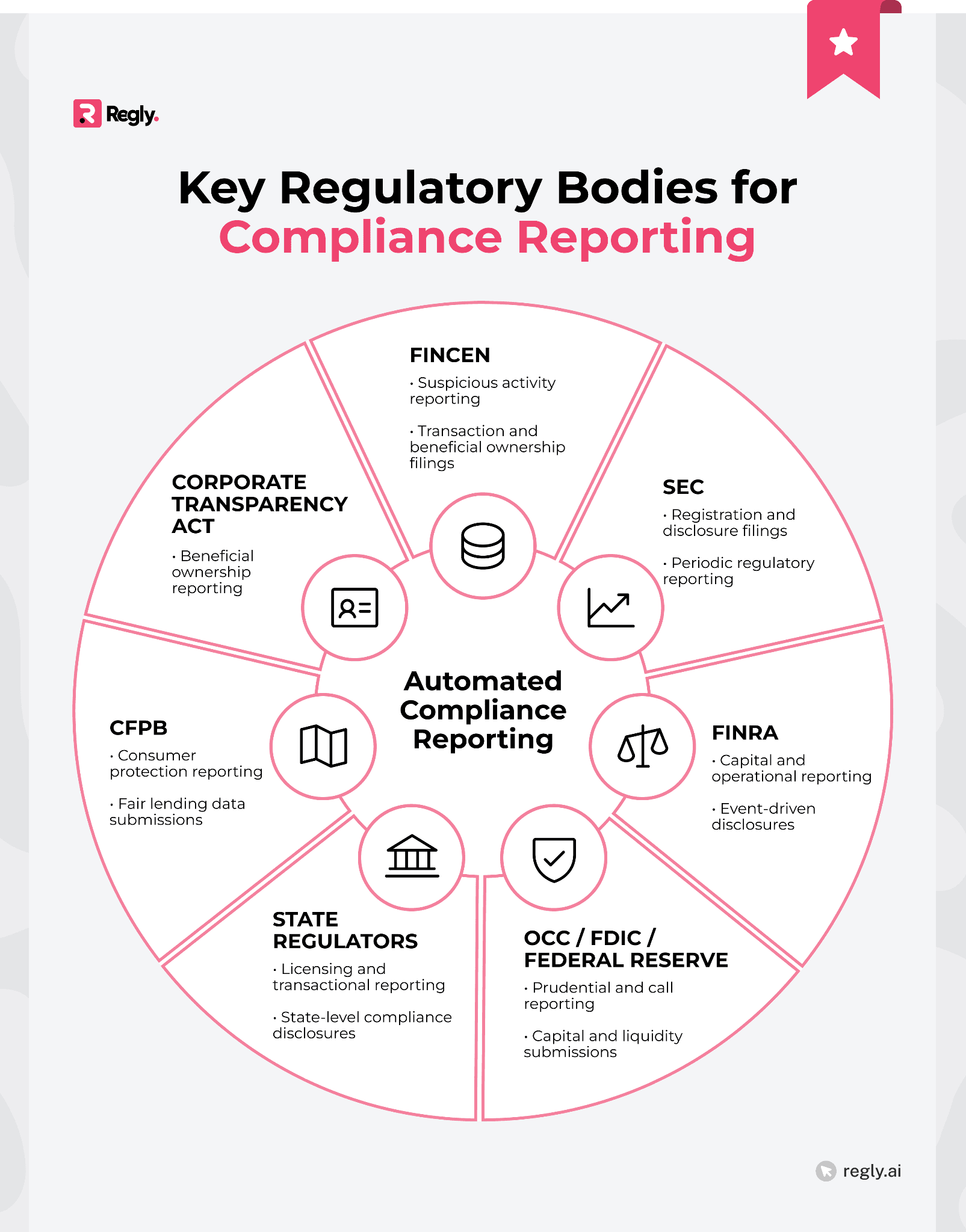

Key Regulatory Bodies and Their Reporting Requirements

Compliance reporting expectations vary by regulator, but the underlying theme is consistent. Each agency focuses on accuracy, oversight, and accountability, even when automation is part of the process.

Here’s how key US regulators think about compliance reporting and where automation fits into their expectations.

1. FinCEN: SARs, CTRs, and AML Monitoring

The Financial Crimes Enforcement Network (FinCEN) focuses heavily on how firms identify, review, and report suspicious activity. Automation is commonly used to monitor transactions, apply thresholds, and generate alerts, but regulators still expect firms to understand and control the process.

For example, an automated AML system might flag transactions that exceed reporting thresholds or show unusual patterns. Compliance teams are expected to review those alerts, document their analysis, and decide whether a SAR or CTR is required.

Automation can speed things up, but it shouldn’t limit the ability to investigate or add context.

If automation filters too aggressively or lacks clear documentation, it can lead to missed filings or weak narratives that draw scrutiny.

2. SEC and FINRA: Broker-Dealer and Advisor Obligations

For broker-dealers and advisors, the Securities and Exchange Commission (SEC) and Financial Industry Regulatory Authority (FINRA) focus on whether firms can demonstrate consistent supervision and accurate reporting across their activities. Automation often supports trade reporting, supervisory reviews, and recurring compliance reports.

For example, firms may use automated workflows to flag trades that fall outside set parameters or to compile supervisory reports on a regular schedule. Compliance teams are still expected to review exceptions, document follow-up, and show how issues were resolved.

During exams, regulators often ask how automated reports are reviewed and who’s responsible for sign-off. They’ll also look at how firms test their systems and handle rule changes. Automation should make supervision easier to track, not harder to explain.

3. CFPB: Consumer Reporting and AI Transparency

The Consumer Financial Protection Bureau (CFPB) pays close attention to how consumer data is used, reported, and explained. When automation is involved, the focus often shifts to transparency and fairness, especially when models or decision rules affect consumers.

For example, if a fintech uses automated processes to generate consumer reports or support credit-related decisions, teams need to understand how those outputs are produced. Compliance teams should be able to explain the logic behind the reporting, identify potential bias, and show how issues are reviewed and corrected.

Examiners may ask:

How automated systems are tested

How changes are documented

How consumers are protected from errors

If automation creates outcomes that can’t be clearly explained, it tends to attract extra scrutiny.

4. OCC, FDIC, and Fed: CMS, Call Reports, and AI Governance

For banks and bank-affiliated fintechs, regulators like the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and the Federal Reserve (Fed) focus on how automation fits into the broader compliance management system.

Reporting isn’t viewed in isolation. It’s tied to governance, controls, and risk management.

Automated processes are often used to:

Support call reports

Internal risk reporting

Ongoing monitoring

Even when reports are generated automatically, teams are expected to understand data sources, review outputs, and document approvals. If a number changes from one period to the next, someone should be able to explain why.

As automation becomes more common, regulators are also paying closer attention to model governance. That includes how tools are tested, how updates are approved, and how teams monitor performance over time. Clear ownership and documentation tend to matter more than the sophistication of the technology itself.

5. State-Level Requirements and the Corporate Transparency Act

State regulators add another layer of reporting requirements, especially for fintechs operating across multiple states. Because expectations can vary by jurisdiction, consistency and clear documentation become even more important when automation is involved.

The Corporate Transparency Act (CTA) is a good example. Firms may use automated tools to collect and track beneficial ownership information, but they remain responsible for confirming accuracy and filing updates when ownership changes. If information isn’t regularly reviewed or refreshed, automation can quickly fall out of sync with reporting obligations.

Because of this, regulators often look closely at:

How firms track state-specific rules

Manage ongoing updates

Confirm that required filings are completed on time

Automation can help manage this complexity, but only when it is paired with clear processes and consistent oversight.

Common Challenges in Automating Compliance Reporting

Automation can reduce manual work, but it also introduces new challenges that teams don’t always anticipate. Here are some of the most common issues fintechs run into when automating compliance reporting.

Fragmented or inaccessible data sources: Reporting often pulls from multiple systems that don’t talk to each other. If data is incomplete, delayed, or stored in silos, automated reports can reflect gaps or inconsistencies that are hard to spot.

Misalignment between tech and regulatory requirements: Tools may be configured around operational needs instead of regulatory rules. When reporting logic doesn’t fully map to actual obligations, automation can produce outputs that look right but miss key requirements.

False positives, missed alerts, and edge cases: Automated rules can be too broad or too narrow. That leads to alert fatigue on one end and missed risk on the other, especially in scenarios that don’t fit clean thresholds.

Scaling systems without losing oversight: As reporting volumes grow, review processes don’t always scale at the same pace. If automation increases output without a clear review of ownership, issues can slip through.

Organizational resistance and process inertia: Teams may be hesitant to change established workflows, even when automation could help. Without buy-in from compliance and operations, tools often end up underused.

Underdeveloped change management and training: Automated systems evolve over time, but training and documentation don’t always keep up. That makes it harder for teams to explain processes or adapt when rules change.

Weak or incomplete documentation for examiners: Regulators expect clear records showing how reports are generated, reviewed, and updated. If documentation is scattered or outdated, exams tend to take longer and raise more questions.

What Do Teams Get Wrong About Automating Compliance Reporting?

Many issues with compliance reporting automation come down to assumptions. Teams move quickly to adopt tools but overlook how regulators actually view automation. These are some of the most common misunderstandings.

Thinking automation equals compliance: Automation can support compliance, but it doesn’t make a process compliant on its own. Reports still need to meet regulatory requirements, and firms are still responsible for the outcomes.

Assuming vendors handle the regulatory details: Vendors can provide technology, but they don’t own regulatory interpretation. Compliance teams are expected to understand how reporting logic works and how it aligns with their specific obligations.

Ignoring the role of human review: Automated outputs still need review, context, and judgment. When teams rely too heavily on automation without defined review steps, regulators tend to push back.

Believing regulators are opposed to automation: Most regulators are neutral on technology. What they care about is whether reporting is accurate, explainable, and well supervised.

Overgeneralizing across jurisdictions or business models: Reporting requirements vary by regulator, product, and geography. A setup that works for one line of business or jurisdiction may not hold up elsewhere.

How Fintechs Can Approach Automating Compliance Reporting

A thoughtful approach to automation starts with process, not technology. Teams that plan for oversight, documentation, and change tend to get more value from automation while avoiding unnecessary compliance risk.

Here’s how fintechs can approach automating compliance reporting in a practical, regulator-friendly way.

Focus Area | What Teams Should Do |

|---|---|

Report selection | Start with high-frequency, high-risk reports |

Data dependencies | Map data sources and update schedules |

Oversight | Build review and approval into workflows |

Documentation | Track changes and maintain version history |

Flexibility | Design workflows that adapt to rule changes |

Ownership | Keep compliance in control of rules and reviews |

1. Prioritize Reports That Are High-Frequency and High-Risk

Not every report needs to be automated right away. Most fintechs see the biggest impact when they start with reports that are filed often or carry higher regulatory risk.

For example, recurring AML reports, supervisory exception reports, or transaction monitoring reviews tend to be good candidates. These reports follow clear rules, rely on consistent data, and consume a lot of manual time. Automating them can reduce workload while improving consistency.

Lower-risk or less frequent reports can wait. Starting small makes it easier to test workflows, refine review steps, and build confidence before expanding automation to other areas.

2. Map Out Data Dependencies and Regulatory Logic

Before automating anything, teams need a clear view of where their data comes from and how reporting rules are applied. If inputs or logic aren’t well understood, automation can amplify mistakes.

For example, a report might rely on transaction data from one system and customer data from another. If those systems update on different schedules or use different definitions, the output can quickly become inconsistent. Mapping this upfront helps avoid surprises.

The same applies to regulatory logic. Teams should be able to explain why a transaction is reportable, how thresholds are applied, and where judgment is required. When that logic is documented, automation becomes easier to manage and defend during an exam.

3. Build Oversight Into the Workflow From the Start

Oversight works best when it’s part of the process, not something added later. Automated reports should move through clear review and approval steps before they’re finalized or submitted.

For example, an automated system might generate a report and route it to a compliance reviewer for sign-off. If something looks off, there should be an easy way to pause the workflow, add notes, and escalate the issue.

When oversight is built in from the beginning, teams are better prepared to explain how automation supports compliance rather than replacing it.

4. Maintain Clear Documentation and Version Control

Automation doesn’t remove the need for documentation. Regulators still expect firms to explain how reports are generated and how changes are managed over time.

For example, if reporting logic is updated to reflect a new rule or guidance, that change should be documented along with the reason for the update and who approved it. Older versions should be retained so teams can explain what was in place at any point in time.

Strong version control makes exams smoother. It shows that reporting processes are deliberate, reviewed, and kept up to date as requirements change.

With Regly’s policy management tool, your team can track policy versions, approvals, and regulatory updates tied to compliance reporting without relying on separate spreadsheets or shared drives.

5. Keep the Process Adaptable to Regulatory Change

Regulatory requirements change, and automated workflows need to change with them. A setup that’s too rigid can quickly fall out of date.

For example, new guidance might adjust reporting thresholds or introduce new data fields. If automation can’t be updated without major rework, teams may end up relying on manual fixes that create confusion.

Processes that are easy to adjust make it simpler to respond to regulatory updates and document how changes were handled. That flexibility tends to matter more than how advanced the technology looks.

6. Make Sure Compliance Owns the Controls, Not Just the Tools

Automation works best when compliance teams own the rules, reviews, and decisions, even if technology supports the workflow. When control sits only with engineering or operations, gaps tend to show up during exams.

For example, compliance should be able to adjust thresholds, review logic, or escalation paths without waiting on a product sprint. They should also understand how reports are generated and be able to explain that process clearly to regulators.

Tools can support efficiency, but ownership matters. When compliance owns the controls, automation becomes easier to manage, easier to explain, and easier to adapt as requirements change.

Key Trends Shaping the Future of Compliance Reporting Automation

Automation in compliance reporting is continuing to evolve as regulators, technology, and business models change. These trends are shaping how fintechs think about reporting, oversight, and long-term scalability.

Real-Time Monitoring as the Emerging Standard

More fintechs are moving away from periodic, batch-based reporting toward real-time or near real-time monitoring. This shift helps teams identify issues earlier instead of discovering them weeks later in a scheduled report.

For example, instead of reviewing transaction activity once a month, automated systems can flag unusual behavior as it happens. Compliance teams can review alerts sooner, document decisions, and address issues before they escalate.

Regulators haven’t mandated real-time monitoring across the board, but many view it as a positive step when it’s paired with proper oversight and review.

Regulator Interest in AI and Model Explainability

As automation becomes more advanced, regulators are paying closer attention to how AI-driven systems make decisions. The focus isn’t on whether firms use AI, but on whether teams can explain how outputs are produced.

For example, if an automated model flags certain transactions or behaviors, compliance teams should be able to explain what factors drove that result. They should also be able to show how models are tested, monitored, and updated over time.

When outputs can’t be explained in plain terms, exams tend to become more difficult. That’s why clear logic, strong documentation, and human review are so important. Together, they help demonstrate that AI is supporting compliance rather than obscuring it.

High-Profile Enforcement Actions Driving Investment

Recent enforcement actions have pushed many fintechs to take a closer look at their reporting processes. In many cases, fines and public orders point back to the same root issues, including gaps in monitoring, weak documentation, or missed follow-ups.

As teams work to address those gaps, many are turning to automation to catch issues earlier and create clearer records of how decisions are made. For example, automated reporting can make it easier to show when an alert was reviewed, what action was taken, and who approved it.

This shift also aligns with what regulators expect to see. Rather than using automation only to reduce manual work, firms are increasingly using it to strengthen controls, improve accountability, and demonstrate that lessons from past enforcement actions have been applied.

Growth of API-First and No-Code RegTech Platforms

More fintechs are turning to API-first and no-code platforms to support compliance reporting. These tools make it easier to connect data sources, adjust workflows, and respond to changes without heavy engineering work.

For example, compliance teams can configure reporting logic, update thresholds, or add review steps without waiting for development resources. That flexibility helps teams move faster while staying closer to the underlying regulatory requirements.

Regulators don’t favor one type of platform over another, but they do care about control and visibility. Tools that give compliance teams direct ownership tend to be easier to explain and manage during exams.

Expansion of Automation Into ESG and Privacy Reporting

Automation is beginning to move beyond traditional compliance reporting into areas like Environmental, Social, and Governance (ESG) and privacy.

As disclosure expectations continue to grow, more teams are turning to automation to make it easier to track data and produce reports consistently, without adding extra manual work.

For example, firms may automate the collection of data tied to privacy requests, consent tracking, or internal ESG metrics. That helps reduce manual effort and creates clearer records when disclosures are reviewed.

Even as these areas continue to evolve, regulators still expect the basics to be covered. Teams should understand their data, clearly document how reports are created, and review outputs before anything is shared externally.

Questions Every Compliance Team Should Be Asking About Automating Compliance Reporting

Before expanding automation, teams should pause and pressure-test their approach. Asking the right questions upfront can help surface gaps, clarify ownership, and avoid issues later during exams or audits.

Which Reports Can We Automate Without Creating Risk?

Not every compliance report is a good fit for automation. Teams should start with reports that:

Follow clear rules

Rely on stable data

Don’t depend heavily on judgment

These are typically high-volume, recurring reports where consistency is more important than interpretation. For more complex or narrative-heavy reports, a higher level of manual review still plays an important role.

The key is to automate where it reduces friction and supports oversight, not where it introduces uncertainty or limits visibility.

How Do We Validate Our Automation Outputs?

Automation only works if teams trust what it produces. That trust comes from having a clear process to review outputs and catch issues early.

Validation can take different forms. Some teams compare automated reports to manual ones during early rollout. Others rely on periodic reviews or spot checks once systems are in place. What matters is having a repeatable way to confirm reports reflect the right data and logic.

When something looks off, teams should be able to trace the issue back to its source and document how it was resolved. That ability often makes the difference during exams.

What Does “Sufficient Oversight” Look Like to Examiners?

Examiners aren’t looking for constant manual involvement. They want to see that people stay accountable and that review steps are clearly defined.

That usually means having named reviewers, documented approvals, and clear escalation paths when something looks wrong. Oversight should be easy to follow, not buried in informal processes or tribal knowledge.

If a regulator asks who reviewed a report, when it was reviewed, and what happened next, those answers should be easy to find and easy to explain.

Are We Capturing and Documenting Regulatory Changes?

Regulatory requirements change over time, and automated reporting needs to reflect those changes. Teams should have a clear way to track updates and show how reporting logic was adjusted.

That includes documenting:

When a change was identified

What was updated

Who approved it

Even small updates matter when examiners ask how current a process is.

Good documentation helps teams explain why a report looks the way it does today and how it’s evolved over time.

Do Our Tools Create New Blind Spots or Gaps?

Automation should make compliance easier to understand, not harder. Teams need to step back and ask whether tools are hiding issues or reducing visibility into what’s happening.

If outputs can’t be easily reviewed or explained, that’s usually a signal that something needs attention. Blind spots often show up when systems aggregate too much or skip context that reviewers rely on.

Regular reviews of both outputs and workflows help confirm that automation is supporting compliance instead of creating new gaps.

—

Automating compliance reporting can help fintechs manage growing regulatory demands, but it doesn’t change what regulators expect. Accountability, oversight, and clear documentation still sit with the firm, even when technology plays a larger role.

Teams that approach automation with a process-first mindset tend to get better results. They focus on where automation adds value, build review and escalation into workflows, and stay flexible as requirements change.

When done thoughtfully, automating compliance reporting can reduce manual effort while improving consistency and visibility. The goal isn’t to replace compliance teams, but to give them better tools to do their jobs effectively.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.