When investors, regulators, or potential partners take a close look at a fintech, a due diligence audit is often one of the first things they ask for. It gives them a clear picture of how the business operates.

To help achieve that, a due diligence audit reviews how compliance programs are structured, how licensing is managed, the technology supporting key processes, and the company’s regulatory history.

In this guide, we’ll explain what a due diligence audit is, how it’s used in fintech and financial services, and what the process looks like. We’ll also outline regulator expectations, frequent gaps teams encounter, and practical ways to prepare for one.

What Is a Due Diligence Audit?

A due diligence audit is a structured way to take a closer look at how a company really operates. It reviews the:

Business

Risks behind it

Controls in place

This audit is usually done ahead of a major decision or regulatory milestone to surface issues early, before they impact valuation, compliance, or daily operations.

It looks at how policies work in real life, how obligations are handled day to day, and whether controls can keep pace as the business grows.

Unlike a traditional financial audit, this process is guided by risk and shaped by the company’s situation. What’s reviewed depends on what the business does and where it’s going, which makes due diligence a practical tool.

Learn more about the differences between customer due diligence (CDD) and enhanced due diligence (EDD) →

Types of Due Diligence Audits

The appropriate type of due diligence audit depends on what’s being evaluated. Together, these different types of audits help build a clear and well-rounded view of the business.

Here are the most common types.

Financial Due Diligence Audit

A financial due diligence audit focuses on a company’s financial position and performance. It helps stakeholders understand:

How the business makes money

Where it spends it

How sustainable its financial model is over time

This review goes beyond standard financial statements to examine how revenue is earned, how dependent the business is on certain customers or partners, and how costs change as the company grows.

It also reviews past financial performance, future projections, cash flow, capital structure, and outstanding obligations. The decision-makers can then assess the business's financial risk and long-term stability.

Legal Due Diligence Audit

A legal due diligence audit focuses on a fintech’s legal structure, obligations, and potential exposures.

It examines:

How agreements are drafted and enforced

How responsibilities are allocated between parties

Where legal dependencies exist, such as reliance on key partners, vendors, or banking relationships

This audit typically covers corporate governance records, material contracts, intellectual property, and pending or historical litigation.

Reviewers also assess whether contractual arrangements align with licensing requirements, consumer protection rules, and supervisory expectations.

Taken together, this entire process helps decision-makers identify legal risk early and evaluate whether the company’s legal foundation can support future growth and regulatory scrutiny.

Regulatory Compliance Due Diligence Audit

A regulatory compliance due diligence audit evaluates whether a fintech is meeting the regulatory expectations tied to its business model and growth stage.

The goal isn’t just to confirm what rules apply, but to understand how compliance is owned, executed, and sustained as the company scales.

Rather than relying on written policies alone, the review looks at how compliance works in practice. This includes:

How controls are implemented

How testing is performed

How issues are identified, escalated, and resolved

For fintechs launching new products, offering crypto-related services, or operating across borders, this hands-on approach matters because regulatory scrutiny tends to increase as complexity grows.

As a result, a regulatory compliance due diligence audit provides a clearer picture of where regulatory risk exists today and how prepared the company is for future oversight. Decision-makers use this information to pinpoint what needs attention, plan ahead, and communicate the company’s compliance position to regulators, partners, and investors.

Operational and Technology Due Diligence Audit

An operational and technology due diligence audit looks at whether a fintech’s systems and processes can reliably support its products as the business grows.

It focuses on:

How the day-to-day operations run

How technology supports both core functions and compliance

Whether the platform can scale without introducing undue operational risk

An operational and technology due diligence audit also looks at how workflows operate in practice, where controls are built in, and how key technology dependencies are managed. It covers internal workflows and process controls, as well as IT architecture, cybersecurity, and data management.

This assessment includes close attention to transaction processing, customer onboarding, automated compliance checks, incident response planning, access controls, system redundancy, and reliance on third-party vendors or cloud providers.

The outcome is a clearer view of operational and technology risks that may not surface in financial or legal reviews. This makes it easier for decision-makers to assess execution capability, system stability, and scalability when making decisions in fast-moving fintech environments.

Tax, HR, and Other Specialized Audits

Beyond financial, legal, and operational reviews, some due diligence efforts focus on areas with more targeted risk.

Tax and HR audits are the most common, but depending on the business model, other specialized areas may also be necessary. These audits help fill gaps that broader reviews can miss.

Tax audits examine compliance with federal, state, and local tax obligations, including income, payroll, and sales taxes. For fintechs, this often includes transaction-based taxes, cross-border exposure, and deferred tax positions. Because issues in these areas can lead to penalties or impact valuation, early visibility is especially important.

HR audits focus on employment practices, payroll accuracy, benefits administration, and compliance with labor laws. Reviews typically include hiring policies, contractor arrangements, and controls around employee data. Weaknesses here can create legal risk and operational strain.

Other specialized audits vary by industry and structure. For instance, intellectual property reviews may confirm ownership of software or proprietary algorithms, while ESG reviews assess alignment with environmental, social, and governance expectations that increasingly matter to investors and regulators.

Together, these audits help verify that the firm’s compliance controls are working as intended.

Why Due Diligence Audits Matter in Fintech and Financial Services

Due diligence audits help fintechs and financial services firms make informed decisions by clarifying risk, readiness, and growth ahead of regulatory, partner, or investor scrutiny.

Key benefits include:

Identifying regulatory and operational gaps early: As fintech products scale, small compliance or operational gaps can quickly turn into real risks. Early-stage practices like informal processes or undocumented decisions may work at first, but rarely hold up as the business grows. A due diligence audit identifies these issues while they are still easier and less costly to address, giving leadership time to fix problems before growth amplifies their impact.

Strengthening compliance readiness before regulatory scrutiny: Rather than reacting to exams or inquiries, due diligence audits help firms understand how prepared they are for regulatory oversight. By reviewing licensing, controls, governance, and execution, audits highlight where expectations may not be met and where improvements are needed before regulators come knocking.

Supporting M&A and funding decisions: During mergers, acquisitions, or funding rounds, due diligence audits become essential. They help uncover hidden liabilities, validate assumptions, and assess integration risks. Without this clarity, organizations risk overpaying, inheriting compliance issues, or facing post-transaction surprises that erode value.

Validating scalability as the business grows: Rapid growth can mask inefficiencies, control gaps, or overstretched teams. Due diligence audits provide a reality check by assessing whether systems, processes, and governance structures can scale safely without compromising compliance, reliability, or customer trust.

Reducing exposure to financial crime and operational failures: Fintechs operate at the intersection of technology, money, and data, where risks move fast. Financial crime, cyber threats, regulatory breaches, and third-party failures can escalate quickly if left unchecked. Due diligence audits flag these risks early, before they become costly incidents.

Improving internal decision-making and accountability: By documenting risks, controls, and ownership clearly, due diligence audits give leadership better visibility into how the business actually operates. This supports stronger decision-making, clearer accountability, and more effective prioritization across teams.

Building credibility with investors and partners: A well-executed due diligence audit shows that the business understands its risks and manages them intentionally. This builds confidence with investors, partners, and counterparties who want proof that growth is sustainable and the company is being run with discipline and foresight.

In an industry where trust can disappear overnight, due diligence audits help organizations stay ahead of risk instead of scrambling to respond. They give leaders the clarity needed to grow with confidence, while reassuring regulators, investors, and customers alike.

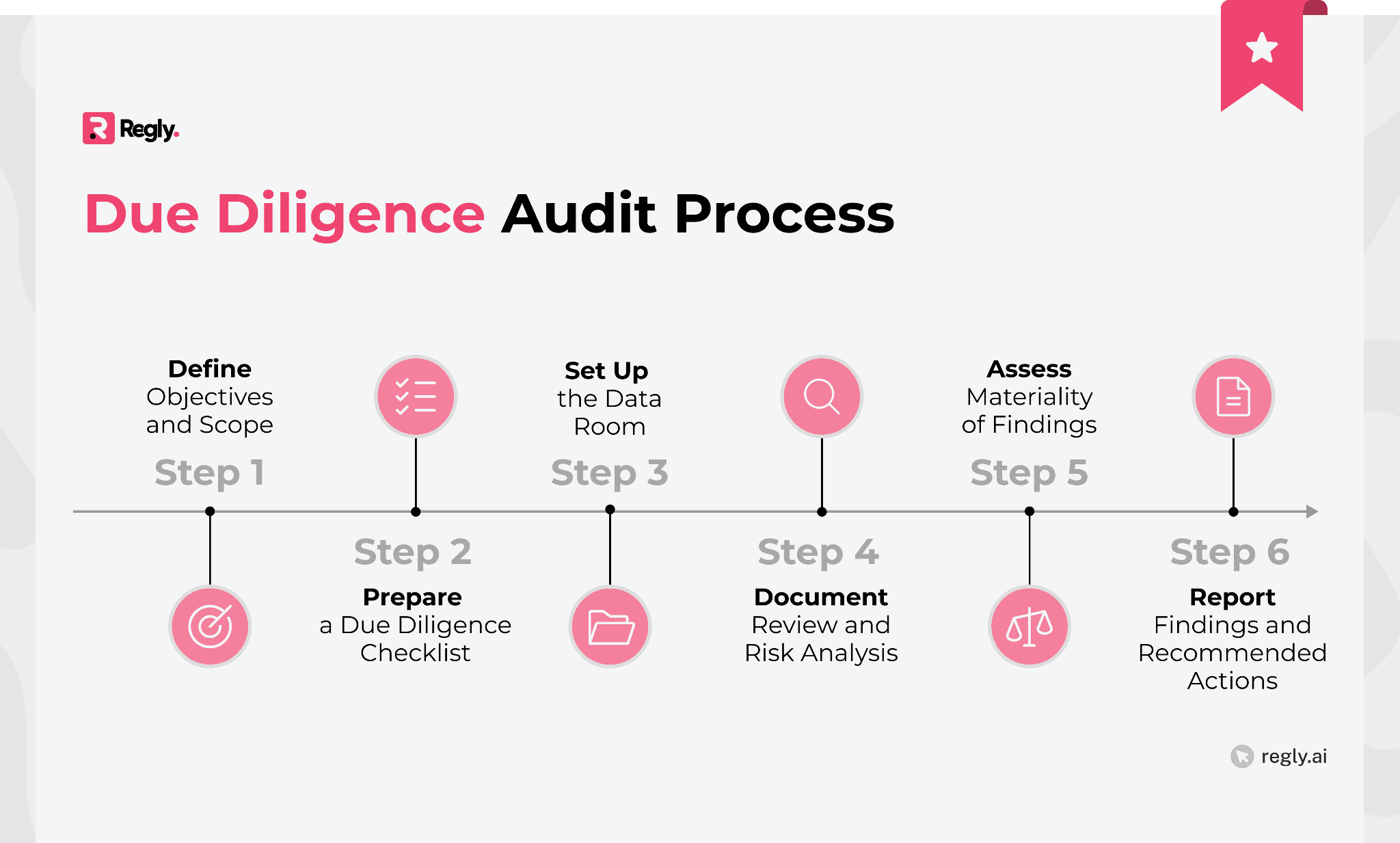

Due Diligence Audit Process Step-by-Step

A due diligence audit breaks reviews into manageable steps so risks can be assessed in a consistent and thorough way. While the details vary by deal or regulator, the overall process helps reduce the risk that important issues are missed.

Here are the key steps involved.

Step 1: Define Objectives and Scope

A due diligence audit begins by first clarifying its purpose. This could include preparing for a merger or acquisition, a capital raise, a licensing review, or an internal risk assessment. Defining the objective upfront helps keep the audit focused on the right business decisions.

That objective then shapes the scope of the review. Teams determine which areas to examine, such as financial, legal, operational, or regulatory matters, and set clear boundaries to focus resources, avoid unnecessary work, and keep the audit efficient and relevant.

Step 2: Prepare a Due Diligence Checklist

With the scope defined, the next step is to build a detailed due diligence checklist that outlines what information needs to be reviewed. This typically includes:

Financial records

Legal agreements

Compliance programs

Operational processes

Technology systems

Specialized areas such as HR or tax, depending on the nature of the audit

This checklist becomes the backbone of the audit. It standardizes the review, keeps teams aligned on expectations, and reduces the risk of overlooking critical issues. By organizing requests and review areas upfront, it also creates a clear roadmap for gathering information and assessing risk consistently and efficiently.

Step 3: Set Up the Data Room and Begin Collection

With objectives defined and a checklist in place, the next step is to gather the required information. This starts with setting up a secure data room, a centralized environment where documents, records, and reports can be stored, accessed, and reviewed in a controlled way.

Organizing materials upfront makes the review more efficient and reduces the risk of missing critical information. Once the data room is ready, documents should be collected according to the checklist, with an emphasis on complete, accurate, and up-to-date files.

Establishing a clear system for tracking submissions helps keep the process moving and avoids unnecessary back-and-forth.

This is where structured policy and document management become critical. Tools such as Regly’s policy management platform help teams centralize policies, track updates, maintain version history, and demonstrate governance during audits.

Having this structure in place reduces follow-up requests, shortens review cycles, and gives auditors confidence that documentation reflects how the business actually operates.

Step 4: Conduct Document Review and Risk Analysis

This stage is where the content of the due diligence audit comes into focus. Collected materials are examined for gaps, inconsistencies, and areas of concern, with attention to how identified risks could affect:

Regulatory compliance

Operational performance

Financial outcomes

For fintechs, particular focus is placed on licensing status, Anti-Money Laundering (AML) and Know Your Customer (KYC) programs, and technology controls. Reviewers aren’t just looking for the existence of documents. They are assessing whether policies and procedures reflect how the business actually operates. Policies that appear sound on paper but aren’t consistently followed in practice are flagged early.

In compliance-focused reviews, testing often includes sampling transactions, alerts, and customer files, as well as reviewing evidence of third-party oversight. This practical testing helps confirm whether controls are working as intended and where weaknesses may exist.

Step 5: Consolidate Findings and Assess Materiality

Not all findings carry the same weight. At this stage, issues are consolidated and reviewed based on potential impact and regulatory sensitivity, with a focus on whether a gap is isolated or points to a broader breakdown.

For instance, a missing document is very different from a weakness that affects customer onboarding or ongoing monitoring.

Assessing materiality helps turn findings into clear next steps. It shows which issues:

Need immediate attention

Can be addressed over time

May influence licensing decisions, partnerships, or deal terms

By focusing on risk rather than volume, teams can prioritize fixes that truly reduce exposure instead of chasing long lists of low-impact issues.

Step 6: Draft the Due Diligence Report and Recommend Actions

With the review complete, the final step is to draft the due diligence report in a clear, usable format. The goal is to present findings in a way that decision-makers can quickly understand and act on.

The report typically includes:

An executive summary

Detailed findings

Risk ratings

Recommended actions

Clarity matters here. Overly legalistic language often obscures the real issues and slows decision-making. Translating regulatory expectations into concrete, operational steps is what turns due diligence findings into meaningful action.

What Regulators Expect from a Due Diligence Audit

Regulators view due diligence audits as evidence that a fintech understands and manages its risks. While each regulator has specific requirements, there are common themes they look for: completeness, accuracy, and operational alignment.

Below are the key areas that should be covered in a due diligence audit:

AML, KYC, and Enhanced Due Diligence

AML, KYC, and enhanced due diligence (EDD) are central to any due diligence report because regulators focus heavily on how firms manage customer risk. This includes having clear, workable frameworks for customer onboarding, transaction monitoring, and identifying and escalating suspicious activity.

During an audit, reviewers look for evidence that the firm understands who its customers are and how risk is assessed in practice. This includes how they:

Make onboarding decisions

Review alerts

Escalate issues after detection

That scrutiny increases for higher-risk customers or jurisdictions. In those cases, auditors expect clearly defined triggers for enhanced due diligence, along with consistent documentation showing how EDD reviews are performed, documented, and maintained over time.

Because these reviews rely heavily on evidence and traceability, many teams use dedicated financial crime and AML tooling to support this work. Platforms like Regly’s fincrime solution help centralize customer risk assessments, alert reviews, and escalation records, making it easier to demonstrate control effectiveness and consistency during due diligence audits.

Learn more about enhanced due diligence (EDD) and how it applies to higher-risk customers and jurisdictions →

Third-Party Risk and Fintech-Bank Partnerships

As fintech–bank partnerships continue to expand, regulators place increased emphasis on how firms manage third-party risk. Due diligence audits are expected to show clear governance around vendor selection, oversight, and ongoing monitoring.

Regulators also look for evidence that banks and fintechs understand shared responsibilities, assess operational and compliance risks, and maintain transparent controls so partnerships operate safely and in line with regulatory requirements.

Because third-party risk management depends on consistent documentation and ongoing oversight, many teams rely on dedicated vendor management systems to support this work.

Tools like Regly’s vendor management solution help centralize due diligence records, risk assessments, and monitoring activities, making it easier to demonstrate effective oversight during audits and partner reviews.

Data Privacy and Cross-Border Rules

Regulators expect firms to know:

Where data resides

Who can access it

How cross-border transfers are managed

The focus here is critical where privacy obligations intersect with consumer protection rules. For that reason, due diligence audits increasingly combine technical reviews with policy analysis.

Common areas of review include data mapping and storage, access controls, cross-border transfers, and incident response, particularly for firms operating across multiple jurisdictions.

ESG and Emerging Due Diligence Areas

ESG is a growing focus for regulators assessing a firm’s long-term resilience and integrity. As a result, due diligence audits are expected to show how environmental impact, social responsibility, and governance standards are built into risk management and everyday decision-making.

This is reflected through clear ESG data, transparent reporting, and frameworks designed to anticipate emerging risks and evolving regulatory and stakeholder expectations.

Who Regulates Due Diligence Audits in Financial Services

In financial services, due diligence audits are shaped by regulatory oversight as much as by business needs. The specific regulators involved depend on the firm’s business model, jurisdiction, and product offerings.

US Regulators

In the US, due diligence audits in financial services are overseen by multiple federal and state regulators responsible for setting standards on risk management, compliance, and governance. Their oversight promotes transparency, protects consumers, and supports financial system stability.

These regulators include:

Financial Crimes Enforcement Network (FinCEN): FinCEN focuses on anti‑money laundering, terrorist financing, and financial crime reporting. It administers key obligations under the Bank Secrecy Act, including suspicious activity reporting and risk‑based due diligence programs for financial institutions.

Securities and Exchange Commission (SEC): The SEC regulates securities markets, broker‑dealers, and investment advisers. It also examines AML programs and compliance with securities laws for firms under its jurisdiction.

Commodity Futures Trading Commission (CFTC): The CFTC oversees derivatives and certain digital asset markets. Its AML and market conduct expectations often shape due diligence requirements for platforms dealing in futures and commodities trading.

Consumer Financial Protection Bureau (CFPB): The CFPB focuses on consumer‑related compliance, including unfair practices and disclosures that may surface during due diligence.

Federal banking regulators, including the Federal Reserve, FDIC, and Office of the Comptroller of the Currency (OCC), also supervise institutions’ risk management, internal controls, and compliance programs as part of examinations.

Global Regulators

As institutions increasingly operate across borders, global regulators play an important role in shaping due diligence audit expectations. Here are the key types of global regulators and how they influence due diligence audits.

International Standard-Setting Bodies: Organizations such as the Financial Action Task Force (FATF) and the Basel Committee establish global benchmarks for AML, counter-terrorist financing, capital adequacy, and risk management. In due diligence audits, reviewers look at how these standards are translated into real controls, including risk assessments, governance structures, and monitoring programs, rather than treated as high-level guidance.

Multilateral Financial Institutions: Institutions such as the International Monetary Fund (IMF) and the World Bank assess the effectiveness of national regulatory and supervisory frameworks through country evaluations and advisory programs. Their findings often shape the scope of a due diligence audit by highlighting systemic weaknesses, emerging risks, or jurisdictions that require enhanced due diligence and closer regulatory scrutiny.

Supranational Regulators: Regulators such as the European Supervisory Authorities issue binding rules and supervisory guidance that apply across multiple jurisdictions. In response, due diligence audits examine how firms have implemented these requirements by focusing on governance, data protection, and cross-border operations.

Global Securities and Market Regulators: Organizations such as the International Organization of Securities Commissions (IOSCO) promote integrity, transparency, and fair conduct across global financial markets. Due diligence audits use these standards as reference points when evaluating controls around market conduct, disclosure practices, and third-party risk management, particularly for firms operating across multiple markets or relying on external service providers.

Common Compliance Challenges in Due Diligence Audits

Due diligence audits often uncover the same compliance challenges, especially for fintechs operating in fast-moving regulatory environments. Recognizing these issues early can help teams address gaps proactively and avoid delays during regulatory reviews.

Common challenges include:

Incomplete or inconsistent documentation: Policies and procedures may exist on paper, but if they don’t reflect day-to-day practices, auditors and regulators will flag the discrepancy. This is particularly common in areas like AML/KYC programs, transaction monitoring, and internal controls.

Siloed processes across departments: Finance, compliance, operations, and technology teams often maintain separate records, making it difficult to consolidate information or demonstrate holistic oversight. Without centralized visibility, risks can be overlooked, and fixing them becomes more expensive.

Rapid product innovation: Fintechs frequently launch new offerings or enter new markets faster than compliance programs can adapt. This can lead to gaps in licensing, cross-border compliance, or data privacy measures.

Third-party and vendor oversight: Outsourced services or technology providers can introduce regulatory and operational risks if due diligence on these partners is insufficient or documentation is missing.

Limited evidence of control effectiveness: Even when controls are in place, firms often struggle to show that they are working as intended. Missing testing results, weak monitoring metrics, or inconsistent issue tracking can raise concerns during a due diligence audit.

How to Prepare for a Due Diligence Audit

Preparing for a due diligence audit requires careful planning, organization, and coordination across finance, compliance, legal, and operations teams. For fintechs, early preparation can save time, reduce risk, and create a smoother audit experience.

The table below outlines key steps to effectively prepare for a due diligence audit.

Preparation Step | What to Focus On |

|---|---|

Assemble a Due Diligence Team | Include representatives from finance, legal, operations, and compliance. |

Organize Documentation | Collect contracts, financial statements, corporate records, and regulatory filings systematically. |

Review Financial Records | Confirm accounts, tax filings, and financial reports are accurate and up-to-date. |

Assess Legal Compliance | Verify licenses, permits, and regulatory obligations are current. |

Conduct Internal Audits | Identify potential risks or discrepancies before external review. |

Prepare management reports | Summarize financial and operational performance for auditors. |

Implement Data Security Measures | Secure sensitive information with controlled access. |

Conduct Pre-Audit Meetings | Align stakeholders on objectives, timelines, and responsibilities. |

Founders: What to Organize in Advance

Founders have a direct impact on how smoothly a due diligence audit runs. Preparing early can prevent delays, reduce surprises, and build trust with investors and partners. Focusing on the areas below helps set the business up for a more efficient review.

Define the Scope: Know why the audit is happening. Clear objectives help your team focus and avoid unnecessary work.

Organize Corporate Documents: Gather incorporation papers, board minutes, licenses, and key contracts. Verify everything is complete and easy to find.

Prepare Financial Records: Have your statements, forecasts, and reconciliations ready. Accuracy and clarity here save time and questions later.

Document Intellectual Property: List patents, trademarks, copyrights, and any software or tech assets. Clear records protect your company’s innovations.

Review Contracts and Obligations: Check employee agreements, vendor contracts, and leases. Spot any risks or liabilities in advance.

Maintain Compliance: Confirm licenses, permits, and certifications are up to date. Stay ahead on taxes, labor laws, and industry regulations.

Organize HR and Operations: Prepare org charts, policies, and key operational metrics. This gives auditors a clear view of how the business runs day-to-day.

Protect Sensitive Data: Secure financial, customer, and proprietary information. Control access and maintain confidentiality.

Do a Pre-Audit Check: Run a quick internal review to catch gaps or discrepancies before auditors arrive.

Align Your Team: Confirm everyone knows their role and responsibilities. Communication keeps the process smooth and stress-free.

Compliance Teams: What to Scrutinize and Document

Compliance teams play a key role in determining how well a firm holds up under review. Focusing on the areas below helps align documentation with execution and address real risks before an audit begins.

Execution over theory: Policies, procedures, and risk assessments should reflect how the business actually operates, not just what is written. Testing evidence should be current, complete, and easy to access.

Alignment during change: Product updates, new partners, and geographic expansion often outpace compliance updates. Change management controls should help compliance evolve alongside the business.

Risk-based prioritization: Teams with deep fintech and regulatory experience recognize common exam and audit patterns. This helps focus effort on material risk and avoid unnecessary over-engineering.

Process-driven operations: Compliance programs built around consistent, repeatable processes tend to perform better under scrutiny.

—

A due diligence audit shows how innovation and regulation really come together inside a business. When done well, it becomes a practical management tool that brings clarity, highlights risk early, and supports better decisions.

For fintechs and financial services firms, this kind of thoughtful, expert-led approach makes growth, partnerships, and regulatory reviews more predictable and manageable.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.