Pay-to-Play Rule for RIAs: Policies, Associates, and Attestations

Published on

Apr 23, 2026

15

min read

The SEC’s pay-to-play rule was adopted to prevent investment advisors from using campaign donations to win or retain government business. For RIAs that advise government entities, this rule can directly affect revenue, hiring decisions, and internal controls.

Rule 206(4)-5 under the Investment Advisers Act imposes a two-year compensation ban if the firm or its covered associates make certain political contributions.

It also restricts the use of third-party solicitors and addresses indirect fundraising activity. Even a small personal contribution by the wrong employee can create firm-wide consequences.

This article breaks down how the pay-to-play rule works in practice. We will cover which advisors it applies to, who qualifies as a covered associate, what contributions trigger restrictions, how the two-year time-out operates, and what policies and attestations regulators expect to see.

What Is the Pay-to-Play Rule?

The pay-to-play rule refers to SEC Rule 206(4)-5 under the Investment Advisers Act of 1940. It prohibits certain political contributions by investment advisors and their covered associates when those contributions are tied to government entities that award advisory business.

The rule was adopted in 2010 after concerns that advisors were making campaign donations to influence the selection of asset managers for public pension plans and other government funds. The Securities and Exchange Commission (SEC) viewed these practices as a form of pay-to-play that undermined fiduciary obligations and public trust.

Unlike general anti-corruption statutes, the pay-to-play rule is a strict regulatory framework. Intent does not matter. A contribution can trigger consequences even if there was no improper motive.

For RIAs advising public pension plans, state retirement systems, or other government entities, this rule is part of the baseline compliance architecture. It interacts with hiring practices, marketing strategy, vendor relationships, and ongoing employee monitoring.

Which Advisors Fall Under the Pay-to-Play Rule

The pay-to-play rule applies to SEC-registered investment advisors, as well as certain exempt reporting advisors. It focuses on advisors that provide advisory services to government entities, whether directly or through pooled investment vehicles.

A “government entity” under Rule 206(4)-5 is defined broadly. It includes:

States and political subdivisions

Agencies, authorities, and instrumentalities of a state or municipality

Public pension plans and retirement systems

529 college savings plans

Pools of assets sponsored or established by a government entity

This means the rule does not apply only to advisors managing traditional public pension mandates. It can also apply to advisors managing private funds where a public pension invests as a limited partner.

Direct and Indirect Advisory Relationships

The pay-to-play rule covers both advisors hired directly by a government entity and advisors to private funds that have government investors.

If a state pension plan invests in your private fund, and you receive compensation from that fund, the rule can apply. The compensation ban operates at the advisor level, not just at the mandate level.

SEC-Registered vs. State-Registered Advisors

SEC-registered RIAs are directly subject to Rule 206(4)-5.

State-registered advisors may be subject to similar state-level pay-to-play laws, which can differ in scope and thresholds.

For fintech RIAs, this distinction matters. A firm may begin as a state-registered advisor and later transition to SEC registration. Political contribution monitoring should account for both regimes, especially during growth or restructuring.

Exempt Reporting Advisors

Certain exempt reporting advisors, such as private fund advisors relying on specific exemptions, are also subject to the pay-to-play rule. Many early-stage venture or crypto fund managers overlook this point.

If you advise a fund with public pension investors, the rule is likely relevant regardless of your registration category.

Understanding whether the pay-to-play rule applies to your firm is the threshold question. The next step is identifying who inside the organization creates exposure.

Who Regulates the Pay-to-Play Rule?

The pay-to-play rule sits within a broader regulatory framework. While SEC Rule 206(4)-5 is the primary federal rule for RIAs, it operates alongside state laws and other regulatory regimes that address political contributions in public finance.

SEC Authority Under the Investment Advisers Act of 1940

The SEC adopted Rule 206(4)-5 under its antifraud authority in the Investment Advisers Act. The rule treats certain political contribution practices as fraudulent, deceptive, or manipulative acts.

Enforcement actions often stem from failures in internal controls rather than intentional misconduct.

State-Level Pay-To-Play Laws and How They Differ

Many states have their own pay-to-play statutes or procurement rules. These can apply to both SEC-registered and state-registered advisors.

Key differences may include:

Area | SEC Rule 206(4)-5 | State Regimes (Varies) |

|---|---|---|

Contribution thresholds | $150 / $350 de minimis | May differ or not apply |

Look-back periods | 2 years (with limited look-back for new hires) | Often different |

Scope of covered persons | Defined “covered associates” | Sometimes broader |

Reporting requirements | No routine filing | Some states require disclosure filings |

In some states, disclosure is required even when the two-year compensation ban does not apply. Others define political influence more broadly than the SEC.

Advisors active in multiple jurisdictions need to understand how these rules intersect, particularly when pursuing public mandates.

MSRB Rule G-37

MSRB Rule G-37 regulates political contributions connected to municipal securities business for broker-dealers. RIAs are not directly governed by G-37, but the rule becomes relevant when firms operate dual BD and advisory structures.

If your firm has both entities, the pay-to-play rule and G-37 can apply at the same time. Each rule defines covered persons and triggering contributions differently.

Monitoring should account for both frameworks so exposure is not missed on either side.

Regly’s policy management module helps fintechs track policies and manage updates →

Interaction With Placement Agents and Third Parties

The pay-to-play rule restricts the use of third parties to solicit government clients unless those third parties are:

Registered broker-dealers subject to MSRB pay-to-play rules, or

SEC-registered investment advisors subject to Rule 206(4)-5

Unregistered placement agents create significant regulatory risk. The rule was amended to limit the “pay-to-play through intermediaries” model that regulators viewed as a workaround.

Vendor oversight is, therefore, part of pay-to-play rule compliance. Advisors should document:

Registration status of placement agents

Representations regarding political contributions

Ongoing monitoring controls

Learn more about the vendor compliance management best practices →

For fintech RIAs that rely on external marketers or capital introduction partners, this area often requires closer review than expected.

Regly’s vendor management module helps RIAs track, organize, and assess vendor relationships →

—

Regulator | Rule / Law | Who It Covers | Why It Matters |

|---|---|---|---|

SEC | Rule 206(4)-5 | SEC-registered RIAs and certain ERAs | Federal pay-to-play framework |

States | State pay-to-play laws | State-registered advisors and firms doing business with state entities | Additional restrictions and disclosures |

MSRB | Rule G-37 | Broker-dealers in municipal securities business | Applies in hybrid BD/RIA models |

When Does the Pay-to-Play Rule Apply?

The pay-to-play rule applies when an investment advisor provides advisory services for compensation to a government entity. That sounds straightforward. In practice, it often is not.

The trigger is not limited to signing a direct advisory agreement with a state pension plan. The rule also applies when government money flows into private funds you manage.

Common scenarios where Rule 206(4)-5 becomes relevant include:

Advising Government Entities: If your RIA is directly retained by a state, municipality, public agency, or government-sponsored authority, the pay-to-play rule applies. This includes public pension mandates and separately managed accounts for government bodies.

Public Pension Plans: Advising a public pension plan triggers the rule. Contributions to officials who can influence manager selection, even indirectly, can result in the two-year compensation ban.

State and Municipal Retirement Systems: Both large statewide systems and smaller municipal plans are covered. If a state or political subdivision creates the entity and manages retirement assets, it typically qualifies as a government entity.

529 Plans and Local Investment Pools: State-sponsored 529 college savings plans and certain local government investment pools fall within the rule’s scope. Exposure here is often missed, particularly when intermediaries handle distribution.

Indirect Advisory Arrangements: The rule also applies when government capital is invested in a private fund you manage. If a public pension invests in your fund, compensation from that fund can be restricted if a covered associate makes a triggering contribution.

Government Client Types: Covered vs. Not Covered

Client Type | Covered Under Rule 206(4)-5? |

|---|---|

State public pension plan | Yes |

Municipal retirement system | Yes |

State-sponsored 529 plan | Yes |

Federal government agency | Generally No |

Private corporate pension plan | No |

ERISA plan sponsored by a private employer | No |

Key Prohibitions Under the Pay-to-Play Rule

The pay-to-play rule is not just a disclosure regime. It imposes direct restrictions that can affect revenue and business development.

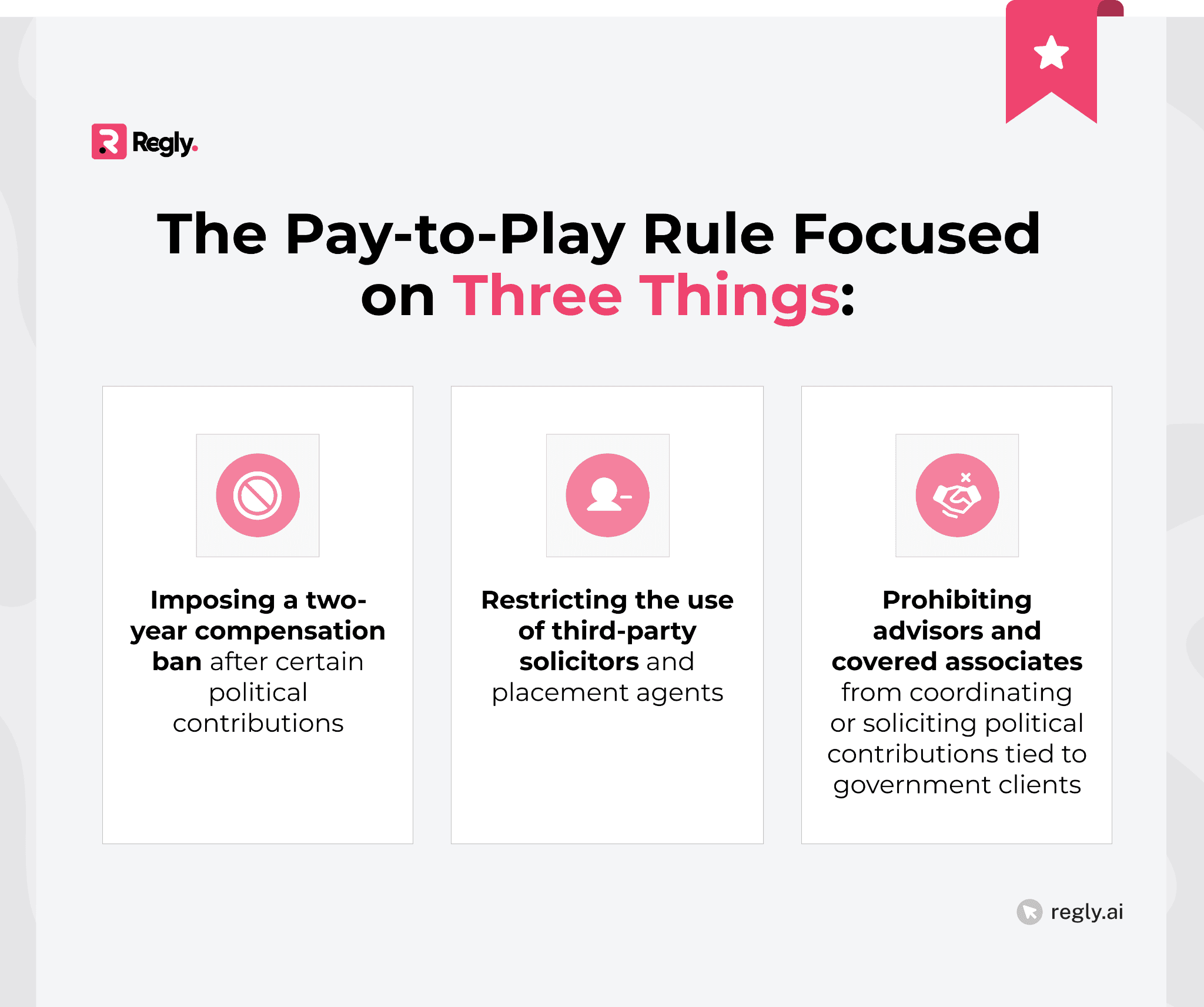

The Two-Year Compensation Ban

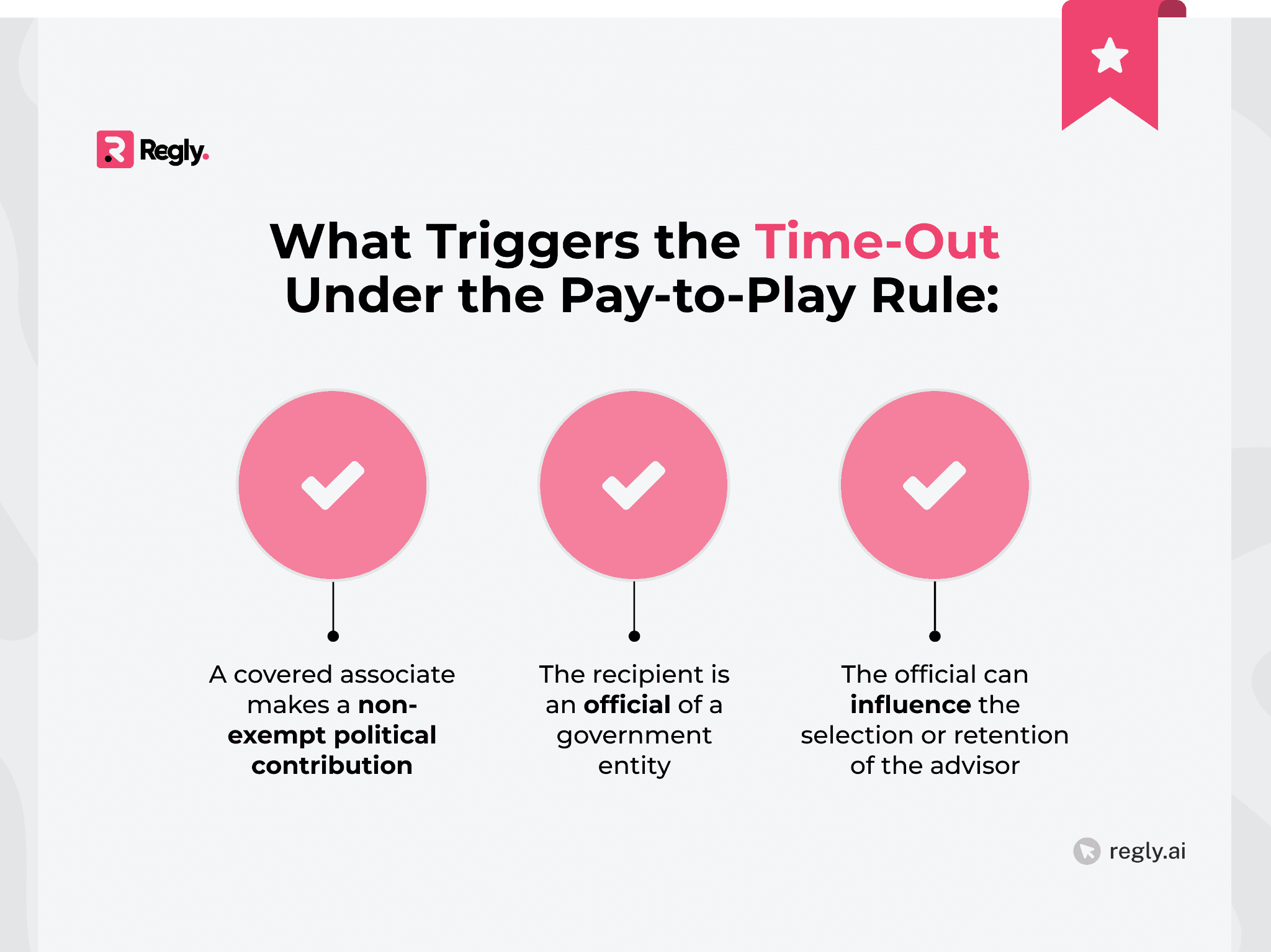

The most significant consequence under the pay-to-play rule is the two-year “time-out.” If a covered associate makes a triggering political contribution to an official of a government entity, the advisor is prohibited from receiving compensation from that entity for two years.

Triggering Political Contributions

A triggering contribution generally involves:

A political contribution to an official of a government entity

An official who can influence the selection of the advisor

A contribution made by the firm or a covered associate

The official does not need final authority. Influence over hiring decisions can be enough.

Direct vs. Indirect Contributions

The rule applies to both direct contributions and indirect activity. That includes contributions made through:

Political action committees controlled by the advisor or covered associate

Coordinated fundraising efforts

Intermediaries used to route contributions

Substance matters more than structure.

What “Compensation” Includes

The ban applies to advisory fees and other forms of compensation tied to advisory services. It does not cancel the contract itself. Instead, it prohibits receiving payment during the time-out period.

In pooled investment vehicles, the restriction can apply at the fund level if government assets are part of the pool.

Third-Party Solicitation Restrictions

The pay-to-play rule also restricts how advisors use placement agents and solicitors to obtain government business.

An advisor may not pay a third party to solicit a government entity unless that third party is: a registered broker-dealer subject to MSRB pay-to-play rules, or an SEC-registered investment advisor subject to Rule 206(4)-5.

The pay-to-play rule places clear boundaries around which intermediaries may solicit government business on your behalf:

Use of Placement Agents: If a third party is marketing your services to a public pension plan or similar entity, you must confirm its regulatory status. Informal marketing arrangements can create risk. This is particularly relevant for emerging fintech advisors that rely on capital introduction partners.

Registered Broker-Dealer Exception: Registered broker-dealers are permitted solicitors because they are subject to MSRB Rule G-37. However, that does not eliminate risk. Political contribution controls still need to be evaluated. Dual-entity firms must align oversight between the RIA and BD sides.

SEC-Registered Advisor Solicitor Requirements: An SEC-registered advisor acting as a solicitor must itself comply with Rule 206(4)-5. If it makes a triggering contribution, the restriction can flow through to the advisory relationship. Due diligence and ongoing monitoring are part of the analysis.

Coordinating or Soliciting Contributions

The rule also prohibits advisors and covered associates from coordinating or soliciting political contributions for: officials of a government entity the advisor is seeking to do business with, and political parties in the relevant state or locality.

This includes fundraising activity, bundling, and organizing events.

A covered associate does not need to write a check personally. Coordinating contributions for others can be enough to trigger restrictions.

—

Prohibition | What It Restricts | Practical Impact |

|---|---|---|

Two-Year Compensation Ban | Receiving advisory fees after a triggering contribution | Direct revenue restriction |

Third-Party Solicitation Limits | Paying unregistered solicitors for government business | Vendor and marketing controls required |

Coordination / Solicitation Ban | Fundraising or bundling for relevant officials | Expanded monitoring beyond personal donations |

Who Is a “Covered Associate” Under the Pay-to-Play Rule?

The pay-to-play rule does not apply to every employee. It applies to specific individuals defined as “covered associates.” Identifying them correctly is one of the most common breakdowns in compliance programs.

Under Rule 206(4)-5, a covered associate generally includes the following categories:

Partners, Managing Members, and Executive Officers: Senior leadership with executive or policymaking authority, including general partners, managing members, presidents, and business unit heads. Function matters more than title. If an individual has executive responsibility or influence over firm direction, they are typically considered a covered associate under the pay-to-play rule.

Employees Who Solicit Government Clients: Any employee who directly or indirectly solicits a government entity on behalf of the advisor is a covered associate. This includes business development professionals, capital raisers, and relationship managers involved in public mandates. The definition focuses on activity, not seniority.

Supervisors of Solicitors: Supervisors of employees who solicit government entities are also covered associates. Even if a manager does not personally market to a public pension, oversight responsibility can bring them within the rule.

PACs Controlled by the Advisor: Political action committees (PACs) controlled by the advisor or by covered associates are also treated as covered associates. Contributions made through these PACs are attributed to the firm for purposes of the pay-to-play rule.

If an individual qualifies as a covered associate, their political contributions can trigger the two-year compensation ban. The risk often surfaces during the hiring of senior personnel, internal promotions into supervisory roles, or expansion into government-facing business lines.

A common issue in enforcement matters is failing to update the covered associate list as responsibilities change. For fintech RIAs that are growing quickly or operating with distributed teams, tracking covered associate status should be an ongoing review, not a one-time designation.

Political Contributions: What Counts and What Doesn’t

Not every political contribution triggers the pay-to-play rule. The analysis depends on who made the contribution, to whom it was made, and whether the recipient has influence over a government entity that awards advisory business.

Direct Contributions

A direct contribution is a payment made by the advisor or a covered associate to an official of a government entity.

If the official can influence the hiring or retention of the advisor, the contribution may trigger the two-year compensation ban. The rule applies regardless of intent.

The timing of the contribution is also relevant, particularly when onboarding new covered associates.

Contributions to Candidates vs. Parties

The pay-to-play rule primarily focuses on contributions to candidates and officials of government entities.

However, it also restricts coordinating or soliciting contributions to political parties in a state or locality where the advisor is seeking government business.

Firms sometimes overlook party-level fundraising activity when assessing exposure.

Federal vs. State vs. Local Offices

Contributions to federal candidates are generally not covered unless the candidate can influence a covered government entity.

By contrast, contributions to state and local officials are more likely to fall within scope if those officials have direct or indirect authority over public pension assets or advisory selection.

The key question is influence over the government entity, not simply the level of office.

De Minimis Exception ($150 / $350 Rule)

The rule includes a limited de minimis exception:

Up to $350 per election to an official for whom the covered associate is entitled to vote

Up to $150 per election to an official for whom the covered associate is not entitled to vote

These limits apply per election, not per calendar year. Exceeding these thresholds can trigger the compensation ban.

Returned Contributions and Cure Provisions

In limited circumstances, advisors may rely on a cure provision if a contribution was inadvertent and returned within a specified time frame.

This relief is narrow and subject to conditions, including limits on the number of times it can be used.

Relying on cure provisions as a primary control is risky. Most firms instead focus on pre-clearance, contribution tracking, and periodic attestations to manage exposure under the pay-to-play rule.

The Two-Year Time-Out: How It Works in Practice

The two-year time-out is the central enforcement mechanism of the pay-to-play rule. When triggered, it prohibits the advisor from receiving compensation from the affected government entity for two years.

The rule also contains a limited look-back provision for newly hired covered associates. Contributions made before joining the firm can still create exposure, depending on timing and role. This is where hiring diligence becomes critical.

See how Regly’s employee compliance module helps fintechs centralize documentation and assign forms and attestations →

The two-year ban restricts compensation, not the advisory contract itself. In practice, that means the advisor may continue providing services, but advisory fees tied to the government entity cannot be received during the time-out period.

For private funds with government investors, the restriction can affect compensation from the entire fund, not just the government’s allocated capital.

Policies Required Under the Pay-to-Play Rule

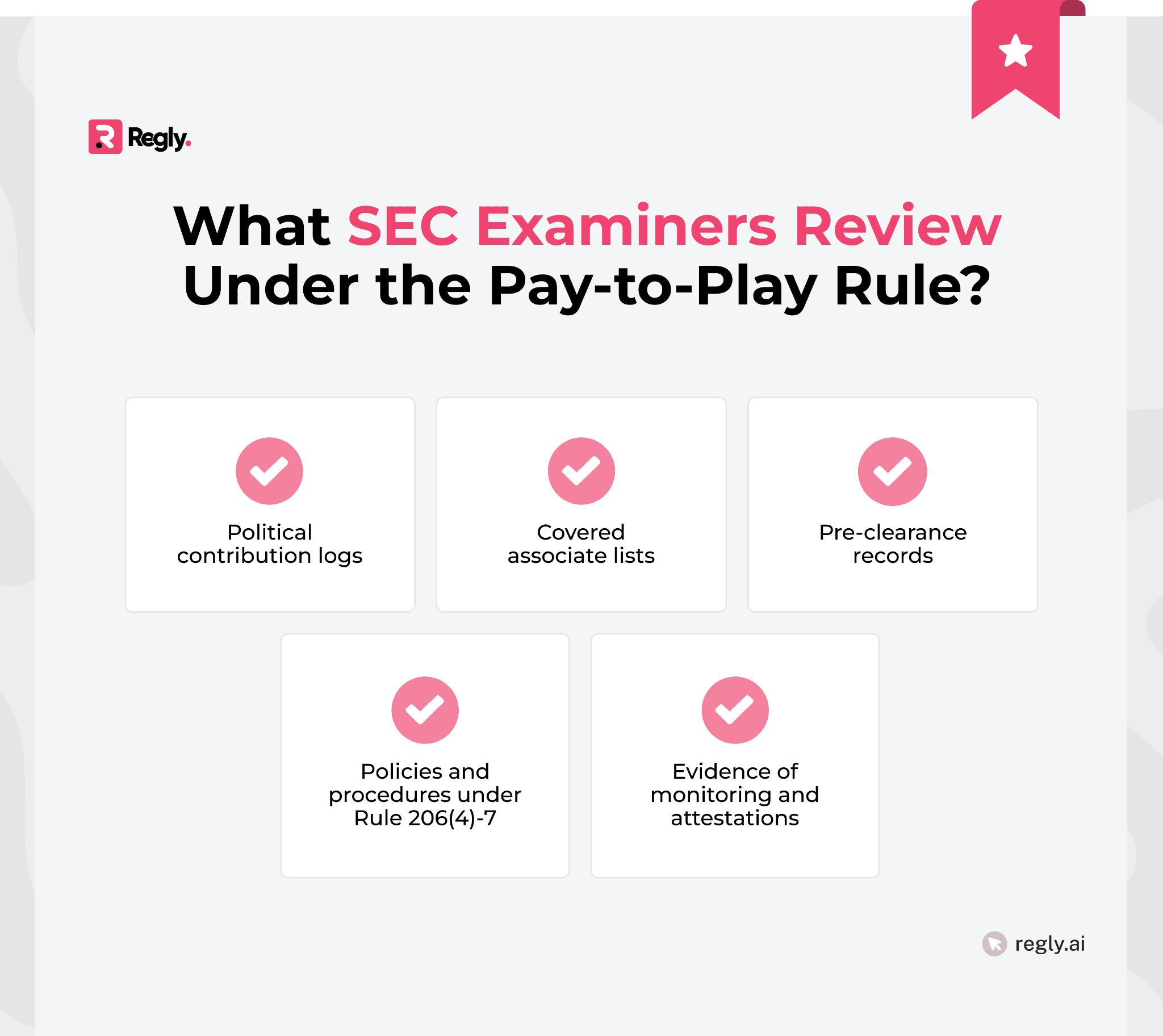

The pay-to-play rule does not prescribe a single template policy. Instead, it operates through the broader compliance framework required under Rule 206(4)-7 of the Investment Advisers Act.

Advisors must adopt and implement written policies and procedures reasonably designed to prevent violations of Rule 206(4)-5. In practice, regulators expect structured controls, documented oversight, and evidence of ongoing monitoring.

A baseline pay-to-play compliance framework typically includes the following components:

Written policies and procedures requirement under Rule 206(4)-7: At a minimum, the policy needs to define covered associates, describe contribution limits, establish pre-clearance procedures, and lay out internal review steps. Contributions made through PACs or other indirect channels should not be left out.

Pre-clearance systems: Before contributing, covered associates should submit the request for review. That review helps determine whether the donation exceeds permitted limits or intersects with existing or targeted public mandates.

Political contribution tracking: Firms should maintain a centralized log of all reported political contributions by covered associates. This log should capture contributor name, recipient, amount, date, office sought, and voting eligibility status.

Escalation workflows: When a contribution exceeds thresholds or raises questions, there should be a defined internal review process. Legal and compliance teams should be involved early, particularly if government business is active or anticipated.

Training requirements: Periodic training helps covered associates understand how the pay-to-play rule applies to them. This is especially important for new hires and employees transitioning into government-facing roles.

For fintech RIAs, policies often fail at the operational level rather than the drafting stage. Rapid hiring, remote teams, and evolving business lines increase the risk that controls exist on paper but are not consistently applied.

Technology can support documentation, task assignment, and periodic reviews.

That is why we have developed Regly Compliance. Based on InnReg’s experience of working with 100+ fintechs, our platform helps businesses centralize compliance tasks using AI-powered tools.

Attestations and Ongoing Monitoring

Policies alone are not enough under the pay-to-play rule. Regulators expect firms to show that controls are operating in real time, not just documented in a manual. Periodic attestations require covered associates to confirm whether they have made political contributions during a defined period.

Pre-Hire Political Contribution Questionnaires

The pay-to-play rule includes a look-back provision for newly hired covered associates. Contributions made before joining the firm can still trigger a two-year compensation ban.

As a result, many advisors require candidates for covered roles to complete a political contribution questionnaire covering a defined historical period.

The review should occur before the individual begins soliciting government business.

Employee Certification Frameworks

A structured certification process typically includes:

Initial designation as a covered associate

Ongoing political contribution reporting

Annual reaffirmation of compliance with the pay-to-play rule

Tracking these certifications across distributed teams can become complex, particularly for fintech RIAs with remote employees and frequent role changes.

This is where centralized compliance systems can support documentation and assignment of attestations without relying on manual spreadsheets.

Supervisory Documentation

Beyond collecting forms, firms should document:

Who is classified as a covered associate

Dates of certifications

Follow-up on disclosed contributions

Escalation decisions and rationale

During an SEC exam, the ability to produce organized records often carries as much weight as the underlying policy language.

Attestations and monitoring turn the pay-to-play rule from a theoretical restriction into an operational discipline.

See how Regly’s employee compliance module helps RIAs manage attestations →

Pay-to-Play Rule Compliance for Fintech RIAs

Fintech RIAs often face a different risk profile under the pay-to-play rule than traditional asset managers. Growth is faster. Teams are distributed. Roles evolve quickly. Each of those factors increases the chance that political contribution controls fall out of sync with the business.

Remote Workforce Contribution Risks

Remote teams make supervision more challenging. Covered associates may sit in different states, each with its own political landscape and potential state-level pay-to-play laws.

When employees relocate, their voting eligibility changes. That directly affects the $150 / $350 de minimis thresholds and how contributions are analyzed.

Firms should periodically review employee location data alongside covered associate status.

See how Regly’s employee compliance module helps RIAs track covered associates, manage attestations, and monitor political contribution exposure across distributed teams →

Digital Political Fundraising Exposure

Campaign activity has largely moved online. Fundraising invitations are shared by email, group chats, and social platforms.

A covered associate might join a virtual fundraiser or forward a donation link without realizing it could raise pay-to-play concerns. The rule covers coordination and solicitation, not just personal contributions. Training should reflect how political activity actually occurs today.

Hybrid Broker-Dealer / RIA Structures

Some fintech businesses run dual registrations as an RIA and a broker-dealer. That setup can trigger obligations under both the pay-to-play rule and MSRB Rule G-37.

If contribution monitoring and covered person lists are managed separately, inconsistencies can develop.

Firms with integrated operations benefit from viewing these requirements together rather than in isolation.

Growth-Stage Hiring Risks

As firms expand, they often hire senior executives, capital markets professionals, or individuals with public sector backgrounds. Those hires may have existing political contribution histories.

Because the pay-to-play rule includes look-back periods, contribution reviews should be part of the hiring process for covered roles.

—

Key Takeaways:

The pay-to-play rule applies to SEC-registered RIAs and certain exempt reporting advisors advising government entities.

A triggering political contribution by a covered associate can result in a two-year compensation ban.

Covered associates include senior leadership, solicitors, supervisors of solicitors, and controlled PACs.

The rule restricts third-party solicitation and coordination of political contributions.

Look-back provisions make hiring diligence critical.

Written policies are not enough. Pre-clearance, tracking, attestations, and supervisory documentation matter.

Fintech RIAs with remote teams and hybrid structures face additional monitoring complexity.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.