Politically exposed persons (PEPs) are a common part of financial services compliance, but they are often misunderstood. For fintechs operating in regulated environments, properly identifying and reviewing PEPs is a basic expectation tied to money laundering risk, corruption concerns, and regulatory oversight.

In this article, we’ll break down what a PEP is, how regulators define different PEP categories, and why PEP status affects customer risk assessments. We’ll also explain how PEPs are treated under US and international rules, when enhanced due diligence comes into play, and where firms most often make mistakes.

What Is a PEP (Politically Exposed Person)?

A politically exposed person is someone who holds, or has recently held, a prominent public position.

Regulators pay closer attention to these individuals because their roles may give them access to public funds, influence over policy, or decision-making authority that could be misused.

Being a PEP doesn't mean someone has done anything wrong.

It simply means their position creates a higher potential risk for bribery, corruption, or money laundering. Because of that risk, financial institutions are expected to apply additional scrutiny when these individuals become customers.

What Is an Example of a PEP?

A politically exposed person can surface at any point during customer onboarding or ongoing monitoring. They don’t even have to be well-known to the public to qualify.

For example, a customer who serves as a deputy minister in a foreign government would be considered a PEP due to their access to public funds and policy decisions. A senior executive at a state-owned oil company could also qualify, even if they’re not an elected official. In both cases, the concern is the influence tied to the position, not the individual’s intent.

PEP status can also appear indirectly.

For instance, if a fintech is onboarding the spouse of a sitting mayor or the business partner of a senior regulator, that relationship may trigger PEP classification.

Why PEP Status Matters in Compliance Programs

PEP status directly affects how a firm assesses customer risk and applies its compliance controls. Because individuals with political influence may present higher risks, regulators expect firms to apply heightened scrutiny when these customers are identified.

Key reasons PEP status matters include:

Higher regulatory scrutiny: Accounts linked to PEPs often receive heightened scrutiny during exams or audits, particularly around identification, documentation, and ongoing monitoring.

Stronger due diligence expectations: PEPs typically trigger enhanced due diligence, which means a deeper review of background information, wealth sources, and account activity.

Ongoing monitoring requirements: PEP risk doesn't stop after onboarding. Firms are expected to monitor transactions and update risk assessments over time, especially if the customer’s role or influence changes.

Exam and enforcement risk: Weak PEP controls are a common finding in regulatory exams. Inconsistent treatment, poor documentation, or missed classifications can lead to follow-up questions or remediation obligations.

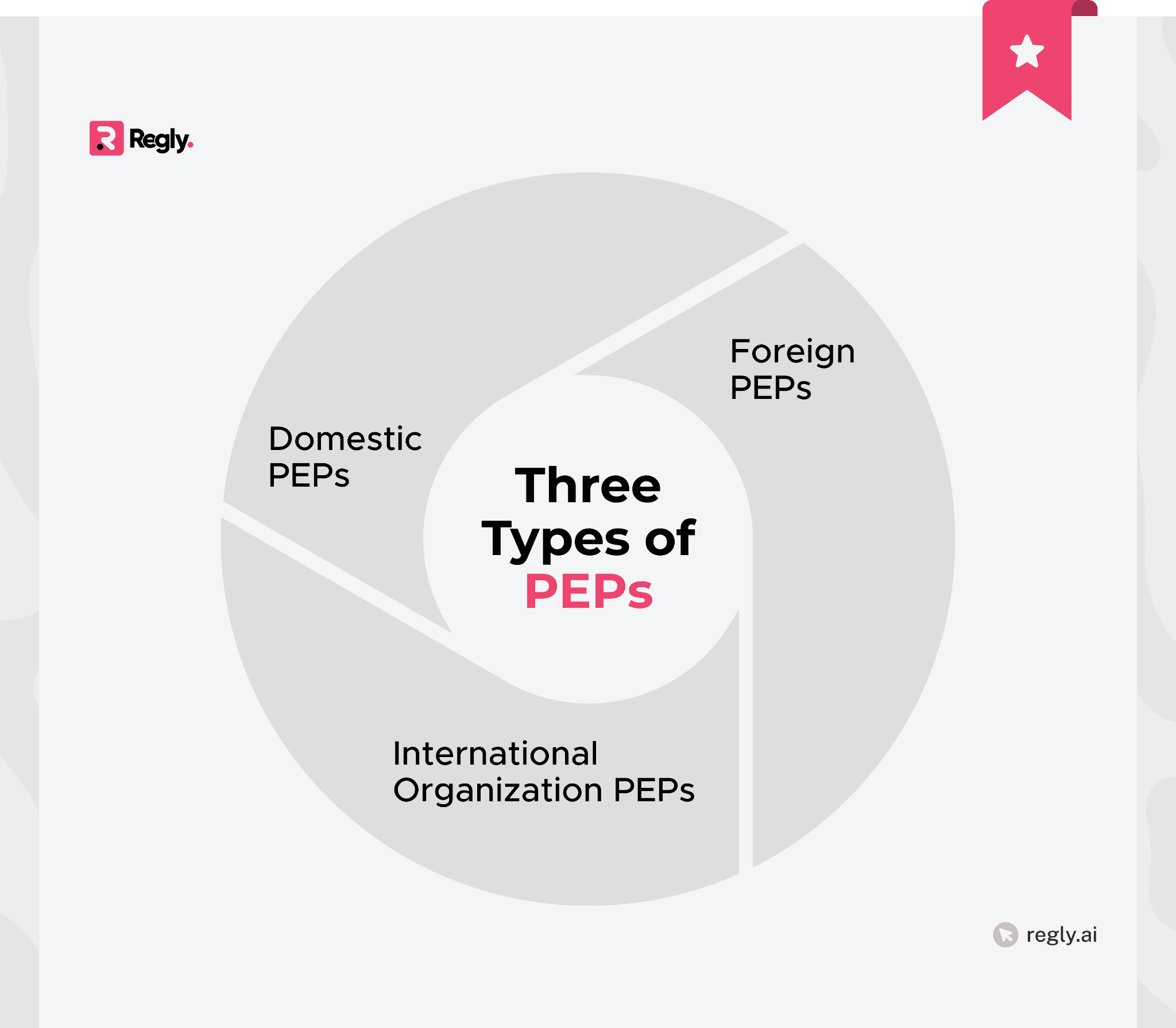

What Are the Three Types of PEPs?

Regulators generally group politically exposed persons into three main categories. These categories help compliance teams assess risk based on the nature of the individual’s role and influence, not their personal behavior.

Here’s how each type of PEP is commonly defined.

Foreign Politically Exposed Persons

Foreign PEPs are individuals who hold, or have held, prominent public positions outside the country where the financial institution operates.

Regulators view these customers as higher risk because cross-border activity can make oversight, transparency, and enforcement more complex.

This category often includes:

Senior government officials

High-ranking military officers

Judges

Executives of foreign state-owned enterprises

The focus is on the level of authority and access tied to the role, not whether the position is elected or appointed.

Because foreign PEPs operate outside the firm’s home jurisdiction, they typically trigger closer review, stronger documentation expectations, and ongoing monitoring as part of a risk-based compliance approach.

Domestic Politically Exposed Persons

Domestic PEPs hold, or have held, prominent public positions within the same country as the financial institution. While these individuals may be easier to evaluate due to local transparency and familiarity, they can still elevate risk.

This category often includes:

Elected officials

Senior regulators

Judges

High-level government executives

Their proximity to public decision-making and resources is what drives the risk consideration.

Firms should assess these types of PEPs using a risk-based approach. Some may require enhanced due diligence, while others can be managed with standard controls and ongoing monitoring, depending on the role and the nature of the relationship.

International Organization Politically Exposed Persons

International organization PEPs are individuals who hold senior roles at global or regional institutions. These organizations often operate across borders, which can introduce similar risk considerations to foreign public offices.

Common roles in this category include senior executives or board members at organizations such as:

International development banks

Intergovernmental bodies

Their risk often stems from their influence over funding, policy decisions, or large-scale programs.

From a compliance perspective, these customers are typically reviewed with added care. Firms should look at the scope of the individual’s authority and the nature of the organization to determine the appropriate level of due diligence and monitoring.

Are Family Members and Close Associates Considered PEPs?

The definition of a PEP can extend beyond the individual to include close family members and known associates, since financial activity may flow through these relationships. The concern is the potential for indirect influence or access, not the relationship itself.

For compliance teams, these connections often require additional context and documentation.

How Regulators Define Close Relationships

When assessing close relationships, regulators focus on ties that involve trust, influence, or shared financial interests. These relationships are relevant because they may be used to move funds or conceal activity associated with a PEP.

Close relationships often include:

Spouses

Partners

Parents

Children

Siblings

They can also include business partners or individuals who regularly act on behalf of the PEP in financial or commercial matters.

The key factor is substance over form. Compliance teams are expected to look at how the relationship functions in practice, not just how it appears on paper.

Where Misclassification Often Happens

PEP misclassification usually results from gaps in context rather than a lack of effort. Job titles can appear senior without real influence, while lower-profile roles may carry substantial authority.

Issues often arise when firms rely too heavily on automated screening results without reviewing the underlying details. Because a name match alone does not reflect actual risk, clear review standards and consistent follow-up are essential.

These processes help teams understand why a customer was flagged and support accurate PEP classification and documentation.

Are PEPs Allowed as Customers in Financial Services?

Politically exposed persons are not prohibited from opening accounts or using financial services. Instead, regulators expect firms to assess PEPs using a risk-based approach and apply controls that reflect the level of risk involved.

Risk-Based Treatment vs. Blanket Exclusions

Most regulators discourage firms from automatically rejecting PEPs. That kind of blanket approach can create unnecessary barriers and isn't how risk should be assessed.

Firms are expected to evaluate each PEP based on their:

Role

Level of influence

Nature of the relationship

This is where a risk-based approach comes into play. It allows compliance teams to apply controls where they matter most. It also helps fintechs balance regulatory expectations with fair access to financial services.

Approach | How It Works |

|---|---|

Blanket exclusion | All PEPs are automatically rejected or offboarded |

Risk-based assessment | Each PEP is reviewed based on role, influence, geography, and account activity |

What Regulators Expect From Firms

When it comes to PEP compliance, regulators generally expect firms to follow a few core practices:

Clear identification processes: Firms should be able to identify PEPs during onboarding and through ongoing monitoring as roles and relationships change. This typically includes screening customers against reliable PEP databases, collecting detailed role and affiliation information, and refreshing screenings periodically to capture new appointments or changes in political exposure.

Documented risk assessments: Firms are expected to document why they classified a customer as a PEP and how they determined their risk level. This usually includes written justification tied to the individual’s role, jurisdiction, level of influence, and source of funds, along with a clear record of the controls applied to mitigate that risk.

Appropriate due diligence: The level of due diligence should match the PEP’s risk profile. For higher-risk PEPs, regulators often expect enhanced due diligence measures such as source-of-wealth and source-of-funds verification, senior management approval, and increased scrutiny of account activity.

Ongoing review and monitoring: Regulators expect firms to reassess PEP relationships on a recurring basis rather than treating them as a one-time classification. This commonly includes periodic risk reviews, ongoing transaction monitoring, and updates triggered by changes in political position, account behavior, or adverse media.

Consistent application of policies: Firms should apply PEP policies consistently across customers with similar risk profiles. Consistency demonstrates that decisions are risk-based and repeatable, which helps firms explain their approach during exams and reduces the likelihood of regulatory findings.

Why Politically Exposed Persons Are a Higher Risk

Politically exposed persons are treated as higher risk because of the positions they hold and the influence that comes with them. These roles can create opportunities for misuse of authority, which is why regulators expect closer attention from financial institutions.

The Link Between PEPs, Corruption, and Money Laundering

PEPs are considered higher risk because their roles can create opportunities for corruption or misuse of public power.

When illicit activity occurs, financial systems are often used to move or hide those funds. That’s why regulators closely scrutinize transactions involving PEPs and expect firms to understand how money flows through these accounts.

The focus isn’t on intent or wrongdoing. It's about recognizing where risk can arise and applying controls that reflect the level of exposure created by the role itself.

Why Fintechs Are Expected to Apply Closer Scrutiny

Fintechs often operate at speed, across borders, and at scale, which can amplify PEP risk if controls are not thoughtfully designed and consistently applied.

Many fintech products make it easier to move funds quickly or access services remotely, which can change the risk profile when a PEP is involved. Regulators, therefore, expect firms to understand these features and adjust their reviews accordingly.

However, closer scrutiny doesn't mean slowing everything down. It means designing checks that fit the product, support growth, and still provide compliance teams with clear visibility.

Key Regulations Governing PEP Compliance

Both international standards and local regulations shape PEP obligations. Although the details differ by jurisdiction, regulators generally align on expectations for risk assessment and due diligence.

Here are the primary regulatory frameworks that set these expectations

FATF Guidance on Politically Exposed Persons

Global expectations around PEPs are largely shaped by guidance from the Financial Action Task Force (FATF), which sets international AML standards.

Under FATF guidance, firms are expected to:

Identify PEPs

Assess the risk tied to their roles

Apply enhanced due diligence where appropriate

The emphasis is on understanding influence, access, and exposure rather than relying on fixed labels.

For fintechs operating across borders, FATF provides a common reference point. Even when local rules differ, FATF principles often shape how regulators evaluate PEP controls in practice.

PEP Requirements in the United States

In the United States, PEP obligations are addressed through existing anti-money laundering frameworks rather than a single standalone rule.

The Financial Crimes Enforcement Network (FinCEN) sets expectations under the Bank Secrecy Act. The Securities and Exchange Commission (SEC) and the Financial Industry Regulatory Authority (FINRA) apply those expectations to regulated financial institutions.

US regulators look at whether firms have practical, reasonable processes for identifying PEPs and assessing the risk they present. Since there’s no official government PEP list, firms typically rely on a mix of screening tools, internal review, and documented judgment.

Regly’s AI-Powered KYC Software supports this process by helping teams identify beneficial owners, flag potential PEP relationships, and centralize supporting information for review.

In practice, what matters most is how decisions are made and supported. During exams, regulators tend to focus on clear risk assessments, appropriate due diligence, and evidence of ongoing monitoring rather than rigid checklists.

Learn more about the difference between CDD and EDD here →

PEP Rules in the EU and UK

In the EU and the UK, PEP obligations are set out more explicitly in regulation. Firms must identify PEPs, apply enhanced due diligence, and continue monitoring for a period even after an individual leaves a public role.

These rules cover domestic PEPs, foreign PEPs, and individuals connected to them, such as family members and close associates. The scope is intentionally broad to account for how influence and access can extend beyond the official position.

For fintechs operating in these regions, the structure can feel more prescriptive than in the US. However, the underlying goal remains the same: assess risk thoughtfully and apply controls that match the exposure.

How PEP Obligations Differ by Jurisdiction

PEP obligations are not applied uniformly across jurisdictions. Requirements vary based on where a firm operates and where its customers are located, with some regulators providing detailed rules and others relying more heavily on risk-based principles.

These differences affect:

How PEPs are identified

How long someone is treated as a PEP

The level of expected due diligence is expected

For fintechs with cross-border activity, this means policies need flexibility. Teams must understand local expectations while applying a consistent approach to risk assessment and documentation.

PEPs and Enhanced Due Diligence (EDD)

Politically exposed persons are usually subject to enhanced due diligence due to the elevated risks associated with their roles and influence. EDD allows firms to take a closer look at these relationships and apply controls that align with the level of exposure.

When Enhanced Due Diligence Is Required

Enhanced due diligence is typically required when a PEP presents a higher level of risk based on their position, authority, or geographic exposure. The trigger is not PEP status alone, but the combination of factors that surround it.

For example, a senior foreign official or someone connected to high-risk jurisdictions may warrant deeper review than a local official with limited influence. The goal is to match the depth of review to the actual risk involved.

How PEP Risk Changes the Due Diligence Process

When a customer is identified as a PEP, due diligence moves beyond basic identity checks. Teams are expected to build a clearer picture of who the customer is and how their role could influence financial activity.

This often means spending more time understanding the customer’s background, connections, and expected account behavior. It also involves documenting why certain controls were applied and how risk will be reviewed over time.

The process doesn't need to be complex to be effective. What matters is that the additional steps are thoughtful, consistent, and aligned with the level of risk the PEP presents.

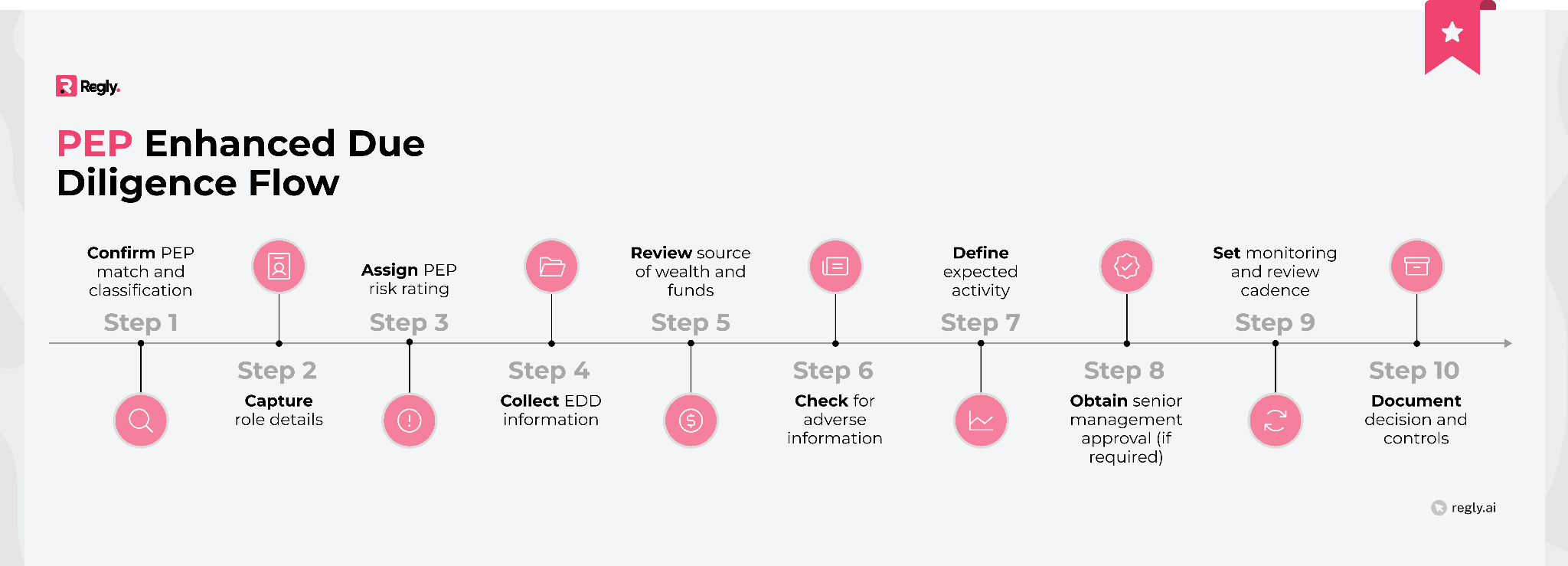

Enhanced Due Diligence Steps for PEPs

Enhanced due diligence for PEPs adds structure and context to higher-risk customer reviews. A clear step-by-step process helps teams apply consistent controls while keeping decisions practical and well documented.

Step 1: Confirm the PEP Match and Classification

Start by confirming that the alert is a true match instead of a false positive. To make that determination, verify core identifiers such as the individual’s full name, date of birth, and jurisdiction, and confirm the public role or relationship that triggered the PEP flag.

Once confirmed, classify the PEP type and highlight whether the individual is the PEP or a related party. This determination directly informs the level of due diligence, approval requirements, and monitoring that follow.

Step 2: Capture the Role Details That Drive Risk

Once the PEP status is confirmed, document the specific role or relationship that creates the political exposure. Record the title, level of seniority, and the country or jurisdiction involved, along with whether the role is current or has ended.

Because recency and authority influence risk, note when the position began and ended, and whether the individual has meaningful decision-making power or access to public funds.

Step 3: Assign a PEP Risk Rating

Using the role details you captured, apply your firm’s PEP risk model to assign a risk rating. Consider defined factors such as role seniority, geographic risk, product type, expected transaction activity, and any elevated risk indicators tied to the position.

The goal is clarity. Document the rationale in plain language to help examiners easily understand the risk rating.

Regly’s risk scoring tool supports this step by generating dynamic risk indicators based on customer attributes, occupation, and jurisdiction to help teams assign consistent and defensible PEP risk ratings.

Step 4: Collect EDD Information

Based on the assigned PEP risk rating, collect the additional information required under your enhanced due diligence procedures. This typically includes:

Background details

Confirmation of current or prior public roles

Employment history

Information that supports the customer’s overall financial profile

Focus on gathering information that explains who the customer is and how their profile aligns with the level of risk you have assigned.

Step 5: Review the Source of Wealth and Funds

Next, assess how the customer accumulated their overall wealth and where the funds used in your product or account will originate. Document whether these sources are reasonable given the individual’s role, jurisdiction, and risk rating, and note any gaps or inconsistencies.

This step helps establish whether the customer’s financial profile aligns with the activity you expect to see over time.

Step 6: Check for Adverse Information

After establishing the customer’s profile and financial background, review credible adverse information related to corruption, bribery, misuse of public funds, sanctions, or other relevant misconduct.

Focus on reliable sources and material issues rather than volume. Document whether the information increases the customer’s risk or requires additional controls or escalation.

Step 7: Compare the Expected Activity to the Product and Use Case

Based on the customer’s role, risk rating, and product use, clearly document what normal activity should look like for this PEP relationship. This includes anticipated transaction types, volumes, and patterns.

Defining expected activity upfront creates a clear baseline for ongoing monitoring and helps teams identify unusual behavior more quickly.

Step 8: Obtain Senior Management Approval When Required

If your policy requires escalation, present the case to senior management for approval before proceeding. Provide a clear, concise summary that explains why the customer is a PEP, the assigned risk rating, key findings from the enhanced due diligence review, and the controls you plan to apply.

This enhances accountability for higher-risk relationships and creates a clear audit trail for regulators.

Step 9: Set Monitoring and Review Cadence

With the relationship approved, define how you will monitor the PEP on an ongoing basis. Document what types of activity you’ll review, how often you’ll rescreen, and when you scheduled the next formal risk review.

Higher-risk PEPs typically require more frequent monitoring and reassessment to reflect changes in role, activity, or external risk factors.

Step 10: Close the Loop With Clean Documentation

Conclude the review by documenting the final decision, supporting evidence, and the controls put in place for the PEP relationship. Store all records, approvals, and monitoring plans in a single, accessible location.

Clear, organized documentation is what makes the entire enhanced due diligence process defensible and easy to explain during a regulatory exam.

How Financial Institutions Screen for PEPs

Financial institutions screen for politically exposed persons to identify customers whose roles may introduce higher risk. Screening typically starts at onboarding and continues throughout the relationship as roles, connections, and risk profiles change.

PEP Checks During Customer Onboarding

PEP screening typically begins during customer onboarding, when firms collect identifying information and run it through AML screening tools. These checks help flag individuals whose public roles may affect their risk profile.

Tools like Regly’s AML screening software support this step by screening customer data against PEP sources alongside sanctions and adverse media.

This helps surface potential matches and prioritize higher-risk cases. When a match appears, teams review the result to confirm accuracy, understand the role involved, and assess whether enhanced due diligence is required.

Clear onboarding workflows make this step more manageable. When teams know what to review and how to document decisions, PEP checks become part of the standard onboarding process rather than a last-minute hurdle.

Ongoing PEP Monitoring and Rescreening

PEP risk doesn't end after onboarding. Roles change, relationships evolve, and a customer who was not a PEP at sign-up may become one later.

Ongoing monitoring helps firms catch those changes. This usually involves periodic rescreening against updated PEP data and reviewing account activity for patterns that no longer match the customer’s risk profile.

Regular reviews keep PEP controls current without adding unnecessary friction. When monitoring is built into routine processes, teams can respond to changes in status or behavior in a timely and consistent way.

The Difference Between PEP and Sanctions Screening

PEP screening and sanctions screening serve different purposes, even though they are often run at the same time.

PEP screening identifies individuals with public roles that may present a higher risk. These customers are not prohibited from using financial services, but they may require additional review and monitoring.

Sanctions screening, on the other hand, focuses on legal restrictions. If a customer appears on a sanctions list, firms are typically required to block or restrict activity.

Common PEP Compliance Challenges for Fintechs

PEP compliance can be difficult to manage in fast-moving fintech environments. Many challenges stem from balancing regulatory expectations with product design, scale, and customer experience.

Common PEP compliance challenges include:

False positives and name-matching issues: Common names, partial matches, and outdated data can trigger frequent alerts. Without clear review standards, teams can spend significant time clearing low-risk matches.

Gaps in PEP data and list coverage: No PEP dataset is complete. Coverage can vary by country, role, and recency, which means firms must rely on judgment alongside screening results.

Scaling PEP reviews as volume grows: Manual reviews that work at low volume can become difficult to manage as onboarding and transaction activity increase. This often leads to backlogs or inconsistent reviews.

Inconsistent risk assessments across teams: When the criteria are unclear, similar PEPs may be treated differently. This can create documentation gaps and raise questions during exams.

Keeping PEP status up to date: Customers may become PEPs after onboarding, or their roles may change over time. Without regular rescreening, these changes can be missed.

Managing friction in the customer experience: Additional questions and documentation can feel intrusive if not handled carefully. Clear communication helps reduce frustration while still supporting compliance needs.

—

Politically exposed persons are a routine part of financial services compliance, particularly for fintechs operating across borders and at scale. PEP status does not indicate wrongdoing, but it does require firms to approach risk with greater care and clearer documentation.

That expectation is best met through strong PEP controls built on clear definitions, consistent reviews, and processes that fit how a product actually works. When screening, due diligence, and monitoring are aligned, teams can manage PEP risk without slowing operations or creating unnecessary friction.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.