A Customer Identification Program (CIP) is one of the first regulatory obligations a fintech encounters when opening accounts for customers. It answers a simple but critical question: who’s this customer, and how do we know?

For many founders and compliance teams, CIP feels straightforward at first. Collect a name, date of birth, address, and identification number. Verify it. Keep records. However, these details carry weight. How you define a customer, how you handle exceptions, and how your systems document decisions can shape your regulatory exposure.

In this guide, we’ll break down what a Customer Identification Program requires, how it fits within an AML framework, and where fintech firms often run into trouble.

What Is a Customer Identification Program (CIP)?

A Customer Identification Program is a written policy that explains how a financial institution collects, verifies, and records information to confirm a customer’s identity before opening an account. In the US, it’s not optional. It’s a required part of an anti-money laundering program.

A CIP answers a few simple but critical questions.

What is the minimum information you should collect from a customer?

How will you verify that information?

How long will you keep those records?

It also requires screening customers against certain government lists.

For fintech teams, a CIP shapes your entire onboarding experience. It affects which vendors you rely on for identity verification, how your product collects and stores customer data, and how information flows across your systems.

The Legal Foundation Under Section 326 of the USA PATRIOT Act

The Customer Identification Program requirement comes from Section 326 of the USA PATRIOT Act. After 9/11, Congress required financial institutions in the US to implement procedures to verify the identity of customers opening accounts.

The objective was clear. Prevent anonymous access to the financial system and reduce the risk that financial institutions could be used to move illicit funds.

Section 326 directed federal regulators to issue implementing rules. Those rules were incorporated into the broader Bank Secrecy Act framework. Today, banks, broker-dealers, mutual funds, futures commission merchants, and introducing brokers in commodities are specifically covered by applicable CIP rules.

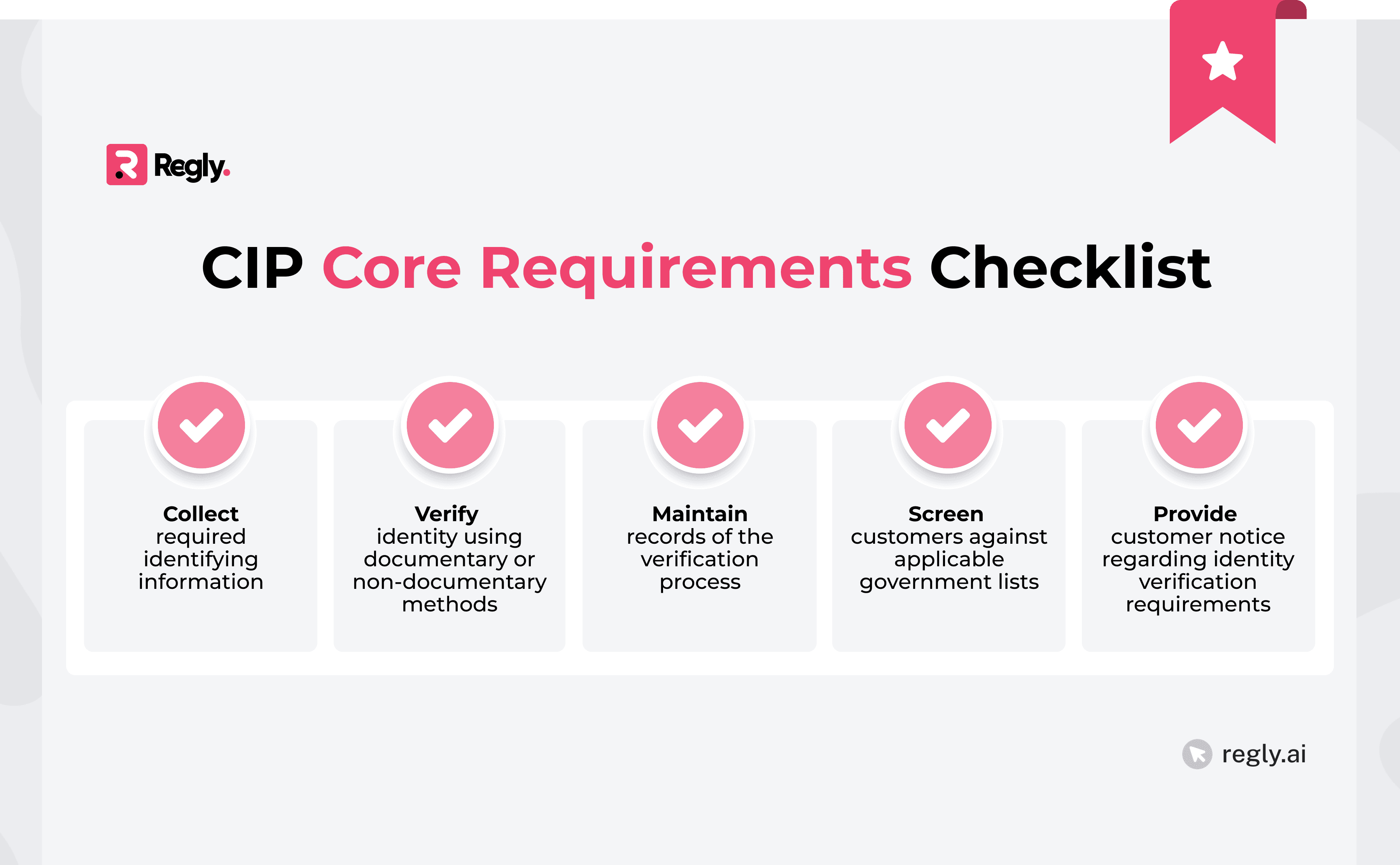

The rule requires institutions to:

Collect specific identifying information before opening an account

Verify the identity of each customer using risk-based procedures

Maintain records of the information collected and the verification steps taken

Screen customers against applicable government lists

How CIP Fits Within an AML Program

A Customer Identification Program isn’t the full AML program. It’s one required component within it, and it lays the groundwork for the rest of your compliance framework.

Under the Bank Secrecy Act, financial institutions should maintain a written AML program that includes internal controls, independent testing, a designated compliance officer, training, and risk-based procedures. CIP is part of those internal controls. It governs how customers are identified before an account is opened.

The identity information collected during onboarding doesn’t stay isolated. It flows into other AML controls and supports how risk is assessed and monitored over time.

CIP data feeds:

Sanctions and watchlist screening

Transaction monitoring rules

Suspicious activity investigations

Because of this connection, weaknesses in CIP rarely stay contained. If identity records are incomplete or poorly documented, risk ratings can become inconsistent, and monitoring alerts may lack context. Investigations may then rely on fragmented information.

This is why regulators examine these controls together rather than in isolation. During exams, they often review onboarding files alongside risk classifications and monitoring activity to see whether identity verification supports the institution’s broader compliance framework.

CIP starts the customer relationship, and the rest of the AML program builds on that foundation. When identity verification, risk assessment, and monitoring controls align, the overall compliance program is far easier to defend.

Customer Identification Program (CIP) vs. Customer Due Diligence (CDD) vs. Know Your Customer (KYC): Key Differences

CIP, CDD, and KYC are often used interchangeably in fintech conversations, but they don’t mean the same thing.

CIP: This is the narrowest concept. It focuses on identity verification at account opening. It requires collecting specific identifying information, verifying it using risk-based procedures, keeping records, and screening against government lists.

CDD: It goes further. Once you know who the customer is, you need to understand their risk profile. That includes evaluating factors such as occupation or business activity, geographic exposure, ownership structure for entities, and expected account activity. CDD answers a different question: how risky is this customer?

KYC: This is the broad umbrella term. It generally refers to the overall process of knowing and understanding your customer. In many organizations, KYC includes CIP, CDD, beneficial ownership information collection, and ongoing monitoring.

Concept | Primary Focus | When It Applies | Core Question |

|---|---|---|---|

CIP | Identity verification | At account opening | Who is this customer? |

CDD | Risk assessment and customer profiling | At onboarding and updated over time | How risky is this customer? |

KYC | Broad compliance framework covering identity and risk | Throughout the customer lifecycle | Do we understand this customer? |

The difference matters operationally.

A fintech might implement a strong identity verification vendor and believe its KYC program is complete. But if there’s no documented risk rating methodology or no process for updating customer risk over time, the firm is only covering the CIP portion of its obligations.

Who Should Comply With Customer Identification Program Requirements?

Customer Identification Program requirements don’t apply to every fintech company in the same way. The obligation depends on the type of regulated financial institution involved and which entity is legally responsible for opening the account.

1. Banks and Federal Banking Agency Rules

Banks should maintain a Customer Identification Program under rules issued by their federal banking regulators. These requirements sit within the broader Bank Secrecy Act framework and apply whenever a bank opens an account for a customer.

The bank’s CIP defines:

What identifying information should be collected

How identity will be verified

How records are stored

How government-list screening is performed

It’s also responsible for documenting situations where identity can’t be verified or where additional review is required.

2. Broker-Dealers Under SEC and FINRA Oversight

Broker-dealers should also maintain a Customer Identification Program as part of their AML obligations under the Bank Secrecy Act and FINRA rules. The requirement applies before a brokerage account can be opened.

The firm should collect identifying information from each customer and verify that information using risk-based procedures. That includes maintaining records of the information collected and documenting how the identity was verified.

For example, if a fintech operates a digital trading platform as a registered broker-dealer, its onboarding process should collect the required CIP information before allowing a user to begin trading. The firm should also keep records showing how the customer’s identity was verified and how any verification issues were handled.

Because broker-dealers often combine identity checks with broader onboarding steps such as suitability questionnaires or account agreements, CIP controls need to be clearly documented within the overall account opening process.

3. Mutual Funds and Other Covered Financial Institutions

Mutual funds and other financial institutions should also maintain a Customer Identification Program under Bank Secrecy Act regulations. The requirement applies when the institution opens an account or establishes a formal customer relationship.

Like banks and broker-dealers, these institutions should:

Collect identifying information

Verify the customer’s identity using risk-based procedures

Keep records, and screen against applicable government lists

The same expectation applies to other covered financial institutions listed in the regulation.

4. Fintech Platforms Partnering With Banks

Many fintech companies don’t hold customer deposits or operate under their own financial licenses. Instead, they partner with regulated institutions such as banks that provide the underlying account infrastructure.

In those arrangements, the partner bank typically carries the legal responsibility for the Customer Identification Program because it’s the institution opening the account. The bank’s CIP policy will define what information should be collected and how identity verification is performed during onboarding.

Even though the regulatory obligation sits with the bank, fintech platforms still play a significant operational role. The product’s onboarding flow, data collection processes, and identity verification tools should align with the bank’s CIP requirements and documentation standards.

Platforms such as Regly can help structure these onboarding workflows by combining identity verification, document analysis, and approval tracking in one environment. This then allows compliance teams to capture verification results and supporting records automatically during account opening.

5. When Reliance on Another Institution Is Permitted

Regulations allow a financial institution to rely on another regulated institution to perform certain elements of the Customer Identification Program. This is known as reliance, and it’s permitted only under specific conditions.

The relying institution should have a formal agreement with the other financial institution confirming that the CIP procedures will be performed on its behalf. The institution performing the verification should also be subject to AML program requirements and regulated by a federal functional regulator.

Even when reliance is permitted, responsibility doesn’t fully disappear. The institution relying on another party should still be comfortable that the procedures are being followed and that documentation is available if regulators request it.

Core Requirements of a Customer Identification Program

Every Customer Identification Program is built around a set of core regulatory requirements. These rules define what information should be collected, how identity is verified, and how records are maintained once an account is opened.

Required Customer Information

A Customer Identification Program should define the minimum information collected from each customer before an account is opened. Regulators expect institutions to gather enough data to form a reasonable belief about the customer’s identity.

For individual customers, institutions generally collect four core data points:

Full legal name

Date of birth

Residential or business address

Identification number, such as a Social Security number or taxpayer identification number

For legal entities, the information typically includes the entity’s legal name, principal place of business, and taxpayer identification number.

The institution should also determine when additional information is required.

For example, if the customer is located in a higher-risk jurisdiction or if the identity data provided can’t be verified through standard checks, the CIP procedures may require collecting supplemental documentation or performing additional verification steps.

Documentary and Non-Documentary Verification

Once identifying information is collected, the institution should verify that the customer is who they claim to be. CIP rules allow two general approaches:

Documentary verification

Non-documentary verification.

Documentary verification relies on identity documents. For individuals, this may include government-issued identification such as a passport or driver’s license. For legal entities, documents may include formation records, partnership agreements, or similar official filings.

Non-documentary verification relies on other data sources. This can include database checks, credit bureau data, public records, or information obtained from trusted third-party verification providers.

Many fintech onboarding systems combine both approaches. A platform may collect a photo of an ID while also checking identity data against external databases. The CIP policy should explain when each method is used and what steps are taken if the verification results raise questions about the customer’s identity.

Recordkeeping Requirements

Regulators expect institutions to maintain clear records showing what information was collected and how identity verification was performed.

These records typically include:

The identifying information obtained from the customer

The method used to verify identity

The results of those verification steps

If documentary verification was used, the institution may record details such as the document type, issuing authority, and identification number.

CIP rules also require institutions to keep these records for specific periods of time. Records describing verification methods and results are generally retained for five years after the record is made, while identifying information is generally retained for five years after the account is closed.

Government List Screening

A Customer Identification Program should also include procedures for checking customers against certain government lists. These lists identify individuals or entities that may be restricted from accessing the financial system.

Institutions should, therefore, determine whether a customer appears on any list that applies to their business. The requirement is triggered when federal regulators designate a specific list for screening under CIP rules.

If a match is identified, the institution should follow its internal escalation procedures. That may involve:

Additional review

Account restrictions

Coordination with regulatory authorities, depending on the circumstances

AML screening platforms, including Regly’s AML screening platform, help automate these checks. They help streamline broader AML/KYC screening during onboarding, such as sanctions, PEP, and adverse-media review, alongside CIP-related identity verification controls.

Customer Notice Requirements

Financial institutions should notify customers that identity information will be collected and verified when they open an account.

This notice is usually presented during the onboarding process. Many firms include it within the account opening flow, such as on a signup page or within the account agreement.

The language typically states that the institution should collect and verify identifying information to comply with federal regulations designed to prevent money laundering and other financial crimes.

Even though the requirement is simple, regulators expect firms to show that customers received this notice during account opening.

Where CIP Breaks Down in Practice

Most Customer Identification Programs look solid on paper. The problems usually appear during onboarding, documentation, or when exceptions start piling up. These gaps are often what regulators focus on during reviews.

1. Misunderstanding Who Qualifies as a “Customer”

The definition of a customer isn’t always as simple as the person using the product.

A customer is generally the individual or entity opening the account. That distinction matters when dealing with business accounts, intermediaries, or platforms where multiple users interact with the same account.

If the policy doesn’t clearly define this, onboarding procedures can become inconsistent. Some accounts may go through full identity verification, while others bypass key steps because the relationship wasn’t classified correctly.

2. Overreliance on Identity Verification Vendors

Many fintech firms rely on third-party identity verification providers during onboarding. These tools can help automate checks and speed up account opening, but they don’t replace the firm’s responsibility under its CIP.

A vendor may verify identity data against databases or perform document checks, but the financial institution still needs to define how those results are interpreted. The CIP should explain:

What counts as a successful verification

When additional review is required

How unresolved results are handled

If those decisions are left entirely to a vendor’s default settings, the program can become difficult to defend during regulatory reviews. Regulators expect the institution to show how verification outcomes connect to its own written procedures.

3. Weak Exception and Escalation Documentation

Identity verification doesn’t always produce a clear result. Some records won’t match perfectly, documents may be unclear, or database checks may return conflicting information. When that happens, the CIP should explain how exceptions are reviewed and documented.

Problems arise when those decisions are handled informally. If analysts resolve verification issues without recording the reasoning or the steps taken, the institution may struggle to explain the decision later.

Regulators often look closely at these cases during exams. They want to see a clear record of what triggered the exception, who reviewed it, and why the account was allowed to move forward.

4. Treating CIP as a One-Time Checkbox

CIP is often treated as a step that happens only at account opening. Once identity verification is completed, the process is sometimes viewed as finished.

That approach can create gaps over time. Customer information may change, accounts may be repurposed, or new risks may emerge that weren’t visible during onboarding.

If identity records aren’t revisited when those changes occur, the information supporting the customer relationship can quickly become outdated. Strong compliance programs connect onboarding data to ongoing monitoring and customer risk reviews.

5. Disconnect Between CIP and Transaction Monitoring

Identity verification is only the starting point. The information collected during CIP should feed into how the institution evaluates and monitors customer activity over time.

Problems appear when onboarding data is siloed from the rest of the AML program. If risk ratings, monitoring rules, or investigations don’t use the identity information collected during account opening, compliance teams may lose important context.

Regulators often review how these pieces connect. They expect to see that customer identity data, risk classifications, and monitoring activity align with each other across the compliance program.

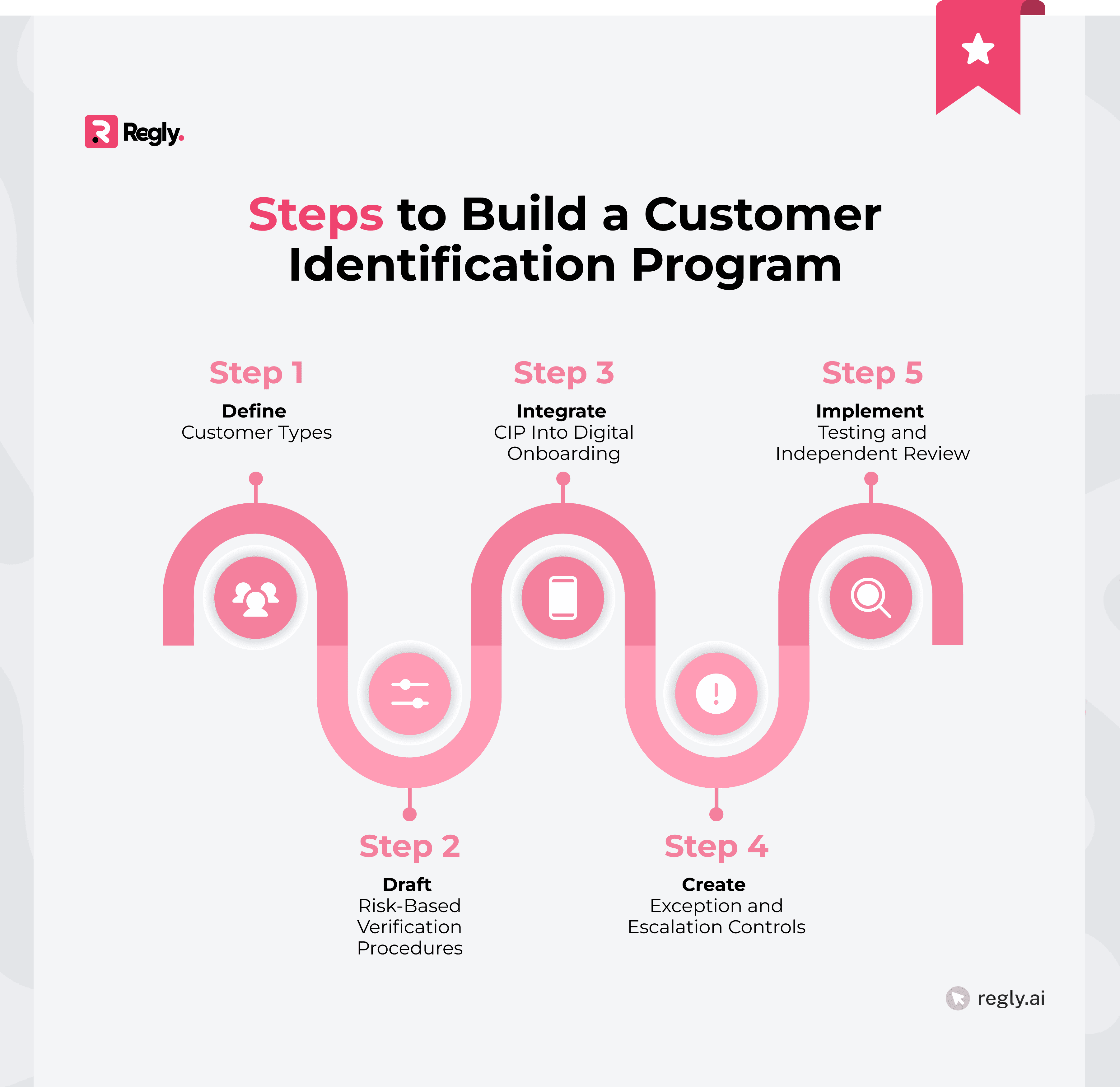

Step-by-Step: Building a Customer Identification Program for a Fintech

Designing a Customer Identification Program involves more than writing a policy. Fintech firms need procedures that work inside digital onboarding systems, vendor integrations, and internal compliance workflows.

Step 1: Define Customer Types and Risk Categories

The first step is defining who your customers are and how different customer types will be treated under the program. Not every account carries the same level of risk, and the CIP should reflect those differences.

Start by identifying the categories of customers the platform supports. This may include

Individuals, businesses

Institutional clients

Other entity types

Each group may require different identity information and verification steps.

The program should also outline how customer risk is categorized. Factors such as geographic location, account purpose, or product features may influence how identity verification is performed and when additional review is required.

Step 2: Draft Risk-Based Verification Procedures

Once customer categories are defined, the next step is documenting how identity verification will occur. CIP rules require verification procedures that reflect:

The institution’s risk profile

The types of accounts being opened

The policy should explain which verification methods are used and when they apply. This includes whether the firm relies on documentary verification, database checks, third-party identity providers, or a combination of methods.

It should also describe how the system handles situations where identity can’t be confirmed through standard checks. That includes additional review steps, escalation paths, and the conditions under which an account may be restricted or closed if verification remains unresolved.

Step 3: Integrate CIP Into Digital Onboarding Flows

Once procedures are defined, they need to be built directly into the onboarding process. Identity information should be collected, verified, and recorded as part of the account opening workflow.

This means aligning the CIP policy with product design. Signup forms, identity checks, and data collection steps should reflect the information required by the program.

The system should also capture verification results and supporting data automatically. When records are tied directly to the onboarding flow, compliance teams have a clearer audit trail showing how each account moved through the verification process.

Step 4: Create Exception Handling and Escalation Controls

Not every verification attempt will produce a clear result. Some identity checks will return partial matches, conflicting data, or incomplete documentation. The CIP should explain how these situations are reviewed and resolved.

The program should define

Who reviews exceptions

What additional information may be requested

How decisions are documented

Clear escalation paths help compliance teams handle unusual cases without slowing down the entire onboarding process.

Strong documentation matters here. When exceptions are recorded with clear reasoning and supporting data, the institution can explain why an account was approved even when the verification process required additional review.

Step 5: Implement Testing and Independent Review

Once the program is in place, it needs to be tested. CIP procedures should be reviewed periodically to confirm that onboarding systems, verification tools, and internal controls operate as described in the written policy.

Testing may include:

Reviewing sampled account files

Checking whether the required identity information was collected

Confirming that verification results were properly documented

These reviews help identify gaps between policy and day-to-day operations.

Independent testing also plays an important role. Many institutions include CIP controls as part of broader AML testing programs to evaluate whether the procedures are working as intended and whether updates are needed as the product or risk profile evolves.

Special Considerations for Digital and Crypto Platforms

Digital platforms often verify identity remotely, without face-to-face interaction. That changes how Customer Identification Programs are implemented and documented.

Fintech and crypto firms need verification methods that work in fully digital environments while still supporting the regulatory requirements behind CIP.

Remote and Non-Documentary Verification

Many digital platforms verify customer identities without collecting physical documents. Instead, they rely on data sources and automated checks to confirm that the information provided by the customer is legitimate.

These methods often include:

Database comparisons

Credit bureau checks

Mobile phone records

Other trusted data sources.

When combined, they can help confirm that the customer’s identity information aligns with existing records.

The CIP policy should explain which non-documentary methods are used and when additional review is required. If the verification results are incomplete or inconsistent, the program should describe how those cases are escalated and documented.

Cross-Border Customers

Fintech platforms often onboard customers located in multiple countries. That adds complexity because identity information, documentation standards, and available verification data can vary across jurisdictions.

The CIP should describe how identity verification is handled when customers are located outside the institution’s primary market. Some regions may have limited public data sources, which can make non-documentary verification more difficult.

The program should also outline when additional documentation or manual review is required for international customers. Clear procedures help compliance teams handle these cases consistently while maintaining reliable identity records.

Use of Biometrics and AI-Based Verification

Many digital onboarding systems now incorporate biometric checks and AI-driven identity verification tools. These technologies can help compare a customer’s selfie to an identity document or analyze patterns that suggest manipulated documents.

While these tools can improve onboarding speed, they still need to align with the institution’s written CIP procedures. The program should describe how biometric checks are used, what thresholds trigger additional review, and how the results are documented.

Compliance teams also need visibility into how these systems make decisions. If a biometric or AI verification tool flags a record as suspicious, the CIP should explain how that alert is reviewed and how the outcome is recorded.

Tools like Regly’s KYC platform can support these workflows by combining biometric verification, document analysis, and identity checks within a structured onboarding process, helping teams document verification results as part of their compliance record.

Embedded Finance and API-Based Onboarding

Embedded finance platforms often open accounts through APIs rather than a traditional signup interface. In these models, customer data may be collected by a partner platform and passed to the financial institution through system integrations.

The CIP should clearly define how identity information flows through these integrations. That includes what data should be collected by the partner, how verification is performed, and how records are stored once the account is created.

Clear data standards matter here. If onboarding information arrives from multiple platforms or partners, the institution needs consistent formats and documentation so identity verification results can be reviewed and audited later.

Stablecoin and Digital Asset Platforms

Digital asset platforms often onboard customers who interact with blockchain-based products rather than traditional bank accounts. Even though the technology is different, the expectation to verify customer identity before establishing a relationship still applies.

The CIP should explain how identity verification occurs before customers are allowed to trade, transfer, or hold digital assets on the platform. It should also describe how identity records are tied to wallet activity and account access.

Clear identity records help connect blockchain transactions to verified users. Without that link, investigations and transaction monitoring can become far more difficult for compliance teams.

What Regulators Review During Exams

Regulators don’t just review the written policy. They also look at how the Customer Identification Program operates inside the institution’s onboarding process and day-to-day compliance controls.

Written CIP Policies and Procedures

Examiners usually start with the written Customer Identification Program. They review the policy to see:

Whether it clearly describes the information collected from customers

The verification methods used

The controls surrounding recordkeeping and list screening

They’ll also check whether the procedures reflect the institution’s products and risk profile. If the firm offers digital onboarding, supports business accounts, or operates across jurisdictions, those realities should appear in the written procedures.

Policies that are vague or disconnected from how the product actually works tend to raise questions. Regulators want to see that the written program matches the firm’s real onboarding processes.

Sampled Account Files and Documentation

Examiners usually review a sample of customer accounts to see how the CIP operates in real situations. They look for the identifying information collected, the verification steps performed, and the records showing how those checks were completed.

The goal is to confirm that the firm followed its own procedures during onboarding. If the policy requires specific data fields or verification methods, those elements should appear clearly in the account records.

Gaps often show up during this stage. Missing identity data, unclear verification results, or incomplete documentation can raise questions about how consistently the program is applied.

Vendor Oversight and Model Validation

When firms rely on third-party identity verification providers, regulators usually review how those vendors are evaluated and monitored. The institution is still responsible for how verification results are used within its CIP.

Examiners often look for documentation showing:

How the vendor was selected

What services it performs

How the institution reviews its performance over time.

They may also ask how verification thresholds, match logic, or automated decision rules are configured.

If automated tools or scoring models are used, regulators may expect evidence that the institution understands how those tools work and how exceptions are handled when results are unclear.

Evidence of Risk-Based Decision Making

Regulators also look for evidence that the Customer Identification Program operates on a risk-based approach. That means verification procedures should reflect the types of customers, products, and jurisdictions the institution works with.

Examiners often review whether different risk levels lead to different verification steps. Higher-risk customers may require additional documentation, manual review, or enhanced verification checks.

They’ll also look at how those decisions are documented. If an account required additional verification or review, the records should show why the step was taken and how the final decision was reached.

Common Deficiencies Cited in Enforcement Actions

When regulators cite CIP violations, the issue often comes down to execution rather than policy design. A program may look complete on paper, but fall short when applied during onboarding.

Several patterns appear repeatedly in enforcement actions and examination findings:

Missing or incomplete identity records

Inconsistent verification procedures across customer accounts

Poor documentation of exception reviews

Heavy reliance on automated verification tools without internal oversight

These gaps usually surface during account file reviews or control testing. If identity verification steps can’t be traced clearly in the records, regulators may conclude that the CIP isn’t being applied consistently.

These types of deficiencies rarely involve a single mistake. They usually reflect a gap between the written CIP policy and how onboarding systems, verification tools, and internal workflows actually operate.

How to Make Your Customer Identification Program Operational

Writing a CIP policy is only the starting point. The real challenge is translating regulatory requirements into systems, workflows, and documentation that hold up during audits and exams.

Translate Regulatory Requirements Into Onboarding Workflows

A CIP becomes effective only when its requirements are built directly into the onboarding process. Identity information, verification checks, and recordkeeping steps should be tied to the systems used to open accounts.

That means aligning compliance procedures with product design. Signup forms, identity verification tools, and backend systems should capture the information required by the CIP and store the results in a consistent format.

When onboarding workflows reflect the written procedures, compliance teams can trace how each account moved through identity verification and how decisions were documented.

Connect CIP Data to AML Monitoring Systems

The information collected during identity verification shouldn’t remain isolated in onboarding records. It should feed directly into the systems used for sanctions screening, transaction monitoring, and customer risk scoring.

When identity data flows into these controls, compliance teams gain clearer context about the customer relationship. Risk ratings can reflect the verified identity information collected at onboarding, and monitoring alerts can be evaluated with more accurate customer details.

If these systems remain disconnected, investigators may have to piece together information across multiple platforms. Integrating CIP data with AML monitoring tools helps create a more complete compliance record.

Build Audit-Ready CIP Documentation

Documentation plays a central role in how a Customer Identification Program is evaluated. Regulators often focus on whether the institution can show what information was collected, how identity was verified, and how decisions were made.

That means records should capture more than the final outcome. They should reflect:

The verification method used

The data sources consulted

Additional review steps taken when the results were unclear

When documentation is structured and easy to trace, compliance teams can respond to exam requests without reconstructing onboarding decisions after the fact.

Track Exceptions and Policy Deviations

Not every account will move through onboarding exactly as the policy describes. Identity verification may return partial matches, documents may require manual review, or additional information may be requested from the customer.

The CIP should define how these situations are recorded and reviewed. Compliance teams should track when verification steps deviate from the standard process and document the reasoning behind the final decision.

Clear exception tracking helps firms show that unusual cases were reviewed thoughtfully rather than handled informally. It also gives compliance teams a way to spot patterns that may signal broader issues in the onboarding process.

Platforms like Regly’s policy management tool can also help teams document these procedures, track policy updates, and maintain version histories that show how exception-handling rules evolve over time.

Create a Defensible Compliance Record

Regulators often focus on whether an institution can explain how identity verification decisions were made. That explanation usually comes from the records created during onboarding and review.

A strong compliance record shows the full path of each account. It connects the information collected from the customer, the verification steps performed, and any additional review that occurred before the account was approved.

When these elements are clearly documented, compliance teams can show that the program operates consistently and that identity verification decisions follow the written procedures.

Frequently Asked Questions About Customer Identification Program (CIP)

What Are the Four Required Elements of CIP?

The four required elements of a Customer Identification Program are: collecting identifying information from the customer, verifying the customer’s identity using risk-based procedures, maintaining records of the information collected and the verification steps taken, and screening customers against applicable government lists. These elements come from Section 326 of the USA PATRIOT Act and form the foundation of CIP requirements under the Bank Secrecy Act.

Is There a Difference Between CIP and CDD?

Yes. CIP focuses on verifying a customer’s identity when an account is opened, while Customer Due Diligence (CDD) goes further by evaluating the customer’s risk profile. CDD looks at factors such as business activity, expected transaction behavior, and ownership structure for entities, and it continues throughout the customer relationship rather than stopping at onboarding.

Are CIP and KYC the Same?

No. A Customer Identification Program is one component of a broader Know Your Customer (KYC) framework. CIP focuses specifically on verifying a customer’s identity before an account is opened, while KYC generally refers to the wider set of processes used to understand a customer, assess risk, and monitor activity throughout the relationship.

What Are the Elements of a Customer Identification Program?

A Customer Identification Program typically includes procedures for collecting identifying information from customers, verifying that information using documentary or non-documentary methods, maintaining records of the verification process, screening customers against applicable government lists, and providing notice to customers that identity verification is required when opening an account. These procedures are documented in the institution’s written CIP policy and integrated into the account onboarding process.

—

A Customer Identification Program plays a foundational role in how financial institutions control access to the financial system. While the regulatory requirements may appear straightforward, the real challenge lies in translating those rules into onboarding processes, verification systems, and documentation that hold up during regulatory review.

For fintech companies, that often means aligning product design, identity verification tools, and compliance workflows from the start. When CIP procedures are built directly into onboarding systems and supported by clear records, firms can scale customer acquisition while maintaining a defensible compliance framework.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.