Outside Business Activities (OBAs) are a recurring employee compliance challenge in the financial services and fintech sectors.

Employees often pursue side projects, board roles, or entrepreneurial ventures outside their primary firm. Regulators require disclosure of these activities because they can create conflicts of interest, distract from client responsibilities, or blur the line between personal ventures and firm business.

This guide explores the regulatory framework surrounding outside business activities and highlights common pitfalls. It also covers practical steps fintech firms can take to manage OBAs efficiently, balancing regulatory expectations with the realities of running innovative, fast-moving businesses.

What Are Outside Business Activities?

In financial services, “outside business activities” (OBAs) refers to any work, role, or business venture that an employee undertakes outside their primary firm. In the broker-dealer context, this definition is broad and applies whether or not compensation is involved.

FINRA Rule 3270 defines OBAs broadly, covering any employment, business venture, or leadership role that sits beyond the firm’s direct oversight.

For broker-dealer representatives, this encompasses any activity, including activities with compensation or even the expectation of compensation, unless it qualifies as a passive investment. Investment advisors have parallel obligations under SEC rules, requiring disclosure in Form ADV Part 2B supplements whenever an outside role is substantial or creates a conflict of interest.

In practice, outside business activities frameworks are designed to prevent conflicts, protect clients, and keep firms from being blindsided by employees’ undisclosed activities.

Why Regulators Care About Outside Business Activities

Regulators don’t view outside business activities as minor side issues. They see them as potential entry points for conflicts, client harm, and reputational damage.

Conflicts of Interest and Client Protection

Regulators focus on OBAs as they can create conflicts of interest that compromise client trust. If an employee is earning money outside the firm, their judgment can be influenced in ways that are not always obvious.

For example, a broker who also sells insurance products might recommend policies that benefit their outside role rather than the client’s best interest. Even when no harm occurs, the perception of divided loyalty can erode confidence in both the firm and its compliance program.

Risks of “Selling Away” and Undisclosed Ventures

Undisclosed outside ventures carry a different risk: the potential for “selling away.” This happens when a registered person solicits or sells securities outside the firm’s supervision.

History shows that many fraud cases, from Ponzi schemes to unapproved private placements, have surfaced through undisclosed OBAs.

Regulators expect firms to identify and stop these activities before clients are harmed. This is why reporting and reviewing OBAs is not a box-checking exercise but a central part of supervisory duties.

Reputational and Operational Impact on Fintech Firms

For fintech firms, the consequences of mishandled OBAs go beyond regulatory fines. Unchecked outside activities can disrupt operations, damage investor confidence, and undermine partnerships.

A founder’s undisclosed side venture or an employee’s crypto project can quickly become a major issue, even if unintended. The reputational fallout often outweighs the initial regulatory penalty, especially for newer companies that are still establishing their credibility.

Firms that manage outside business activities effectively reduce both regulatory and reputational exposure. For fintechs looking to build scalable oversight, tools like Regly’s employee compliance platform provide a structured way to track and review OBAs →

FINRA Requirements for Outside Business Activities

FINRA requires registered persons to disclose any outside business activity before engaging in it. Businesses then have a duty to review the request, assess conflicts, and decide whether to approve or restrict the activity.

FINRA Rule 3270

Rule 3270 is the foundation of FINRA’s OBA framework. It prohibits a registered person from engaging in any activity, including activities where compensation is received, or holding a reasonable expectation of compensation, from any outside activity unless they provide prior written notice to their firm.

The rule is broad by design, encompassing roles such as employment, partnerships, officer or director positions, and independent contractor work. Once notified, the company must determine whether the activity could interfere with the individual’s responsibilities or create the impression that the activity is conducted on behalf of the firm.

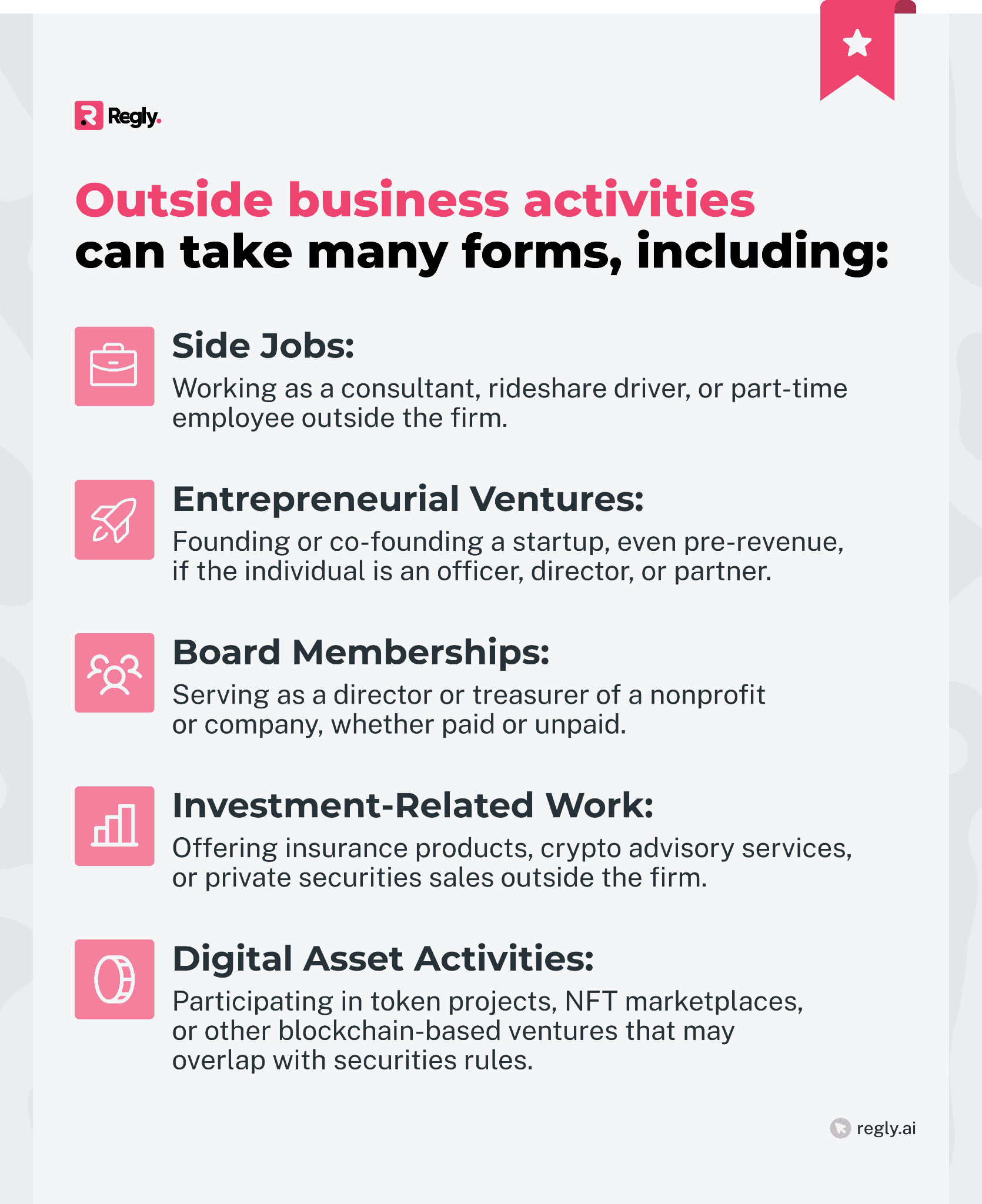

The rule does allow for passive investments, such as owning publicly traded securities or holding a limited partnership interest, without requiring disclosure. But if the individual plays an active role in the management or operations of that investment, the activity typically crosses into OBA territory.

FINRA Rule 3280

Rule 3280 addresses a specific but high-risk category of outside business activities: private securities transactions. This rule applies when a registered person is involved in soliciting or selling securities away from their firm.

Examples include raising money for a friend’s startup or promoting a private placement. Under Rule 3280, the individual must disclose the planned activity in writing before engaging in it.

If the activity involves any form of compensation, the individual must get the firm’s approval before participation, and the firm is required to then supervise the transaction as though it were conducted within the firm. This includes recording the activity on the company’s books and applying the same supervisory oversight as in-house transactions. Disclosure is still required even if the individual doesn’t expect compensation, but the firm has discretion to approve or prohibit participation.

The rule is rooted in the idea that “selling away” creates significant risks for investors and businesses. Undisclosed activity in this area is one of the most common grounds for FINRA enforcement actions.

Form U4 Requirements for Registered Individuals

Registered representatives must disclose outside business activities in writing to the firm (pursuant to Rule 3270) and on Form U4. The Form U4 requires details such as the business name, role, compensation, and hours per month devoted to the activity. Updates must be filed within 30 days of any change. Inconsistencies between U4 filings and firm records are a common examination finding.

SEC Requirements for Outside Business Activities

Unlike FINRA, which imposes prescriptive rules, the SEC follows a disclosure-driven model for outside business activities.

Investment advisors are required to adopt a Code of Ethics under Rule 204A-1 of the Advisers Act, which must include procedures for reporting and addressing conflicts of interest. OBAs fall directly into this framework because they can influence an advisor’s judgment, divert time from client work, or create undisclosed compensation streams.

The primary mechanism for disclosure to customers of an RIA is Form ADV:

Form ADV Part 2A requires firms to disclose other financial industry activities or affiliations.

Form ADV Part 2B requires individual supervised persons to disclose outside business activities if they consume more than 10% of their time or income, or create a conflict of interest.

Learn more about Form ADV Part 2 →

The disclosure obligation frames how the firm demonstrates its fiduciary duty to act in the client’s best interest. If an outside business gives rise to financial incentives that might bias recommendations, the company must clearly explain this to clients and, where possible, adopt policies to mitigate the conflict.

Other Regulators Overseeing Outside Business Activities

Banking regulators, like the OCC and the Federal Reserve, impose restrictions on directors and officers serving on outside boards. For fintechs engaged with crypto, digital asset activities may fall under FINRA or SEC rules if they resemble securities transactions. States also play a role, particularly for state-registered advisors.

Common Compliance Challenges with Outside Business Activities

Managing outside business activities may look simple on paper, but fintech firms often run into recurring problems in practice. The most common issues involve underreporting, unclear definitions, and the practical burden of reviewing and supervising disclosures.

Employees Failing to Disclose Side Projects

The single biggest challenge is non-disclosure. Employees may assume a side gig is too minor to mention or worry that compliance will deny it. This creates risk not only for the employee but for the firm, which is responsible for monitoring OBAs even if it never received notice.

Regulators often uncover undisclosed side businesses during routine exams or through client complaints, and the penalties fall on both the firm and the individual.

Non-disclosure is one of the most frequent breakdowns in employee compliance programs, making it critical to address OBAs alongside other areas such as personal trading and gifts.

Passive vs. Active Involvement

Distinguishing between passive investments and active business roles is another gray area.

Simply owning a rental property or holding public securities typically does not qualify as an OBA. But once an employee forms an LLC, manages tenants, or actively solicits investors, the activity usually crosses into OBA territory.

Compliance teams must train employees to recognize when a “personal investment” becomes an outside business.

Crypto, NFTs, and Digital Asset Activities as OBAs

Activities such as token launches, NFT projects, or staking operations may not always be classified as securities, but regulators expect firms to review them as potential OBAs. A registered person’s involvement in a crypto startup or blockchain venture can quickly move into regulated territory. Ignoring these activities exposes firms to unnecessary scrutiny.

Supervising and Documenting Approvals

Even when registered representatives disclose OBAs, the challenge shifts to supervision. Businesses must then decide whether to approve, deny, or conditionally allow the activity. If approved, regulators expect to see documentation showing that the company considered potential conflicts, client impact, and supervisory responsibilities. Without a consistent process, firms risk having their approvals questioned in exams or enforcement action.

Learn how Regly’s employee compliance module enables fintechs to centralize the approval process →

Keeping U4 and ADV Forms Up to Date

Maintaining current regulatory filings is a constant challenge. Every approved OBA for a registered representative must appear on Form U4, and changes must be reported within 30 days.

Learn more about Form U4 →

Investment advisors face a similar requirement through Form ADV Part 2. Regulators frequently cite outdated forms as exam deficiencies, often because businesses lacked a clear process to connect internal OBA approvals with required filings.

Although different, outside brokerage accounts raise similar risks when firms don’t have a process to capture employee trading activity.

Learn more in our outside brokerage accounts article →

Misconceptions That Lead to Compliance Gaps

Employees and even founders often misunderstand what qualifies as an outside business activity. As these misconceptions create blind spots, addressing them directly is essential to building a stronger compliance program.

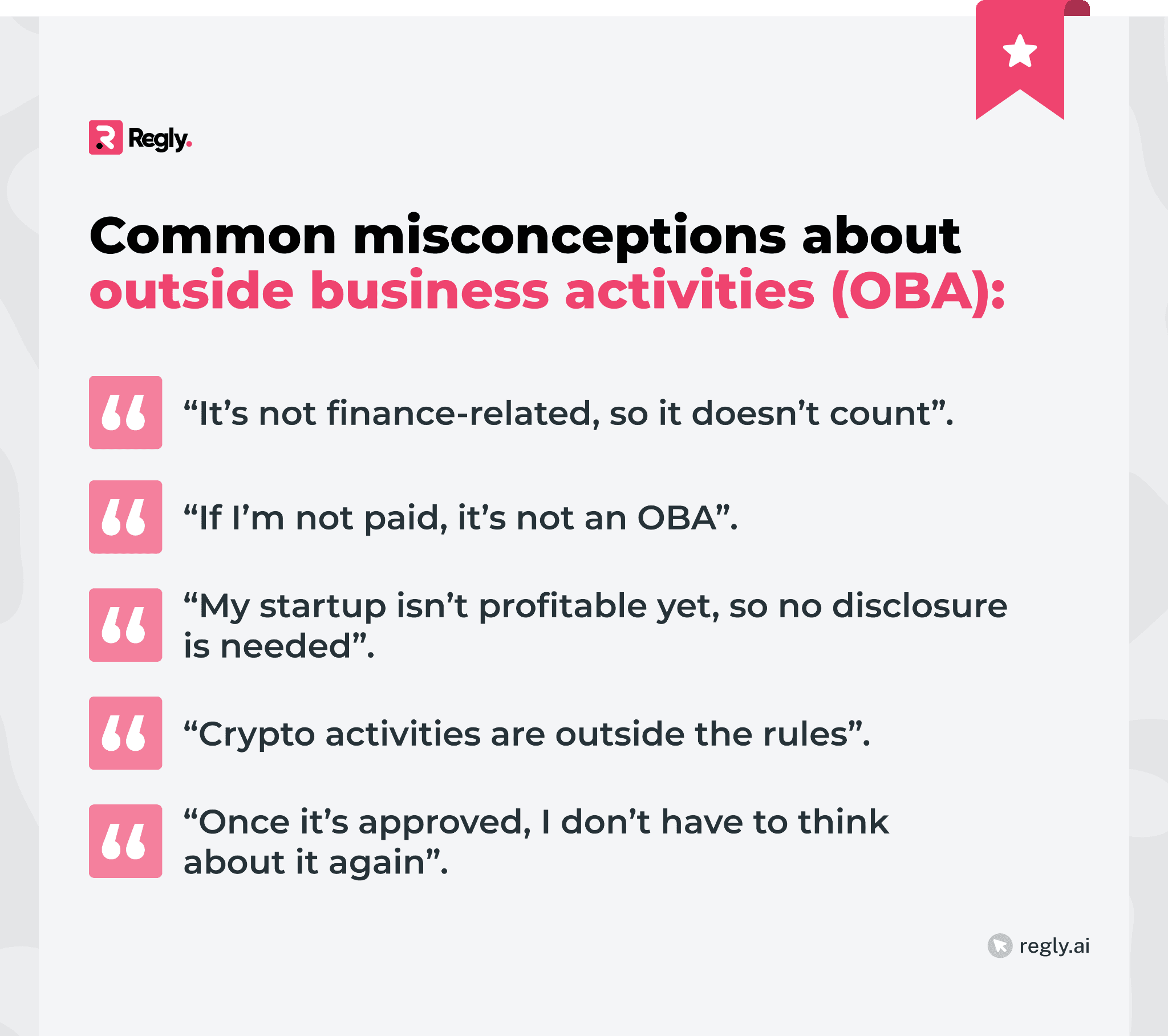

“It’s not finance-related, so it doesn’t count”

FINRA Rule 3270 requires disclosure of all outside business activities, not just those tied to finance. Side jobs like bartending or ride-share driving may seem irrelevant, but they are still technically reportable.

While proposed rule changes may narrow the scope, firms should treat unrelated income-generating activities as disclosable until the rules are finalized.

“If I’m not paid, it’s not an OBA”

Compensation is not the only factor. Unpaid board memberships, treasurer roles, or leadership positions can still present conflicts of interest. Regulators view significant unpaid commitments as relevant because they consume time and may influence business decisions.

“My startup isn’t profitable yet, so no disclosure needed”

Other than passive activities, any outside business activity triggers the rule, not necessarily compensation. If an employee founds a startup, even pre-revenue, they must disclose the activity. Regulators look at the role (officer, director, partner), not just the paycheck.

“Crypto activities are outside the rules”

Digital assets often fall in a gray zone, but regulators expect disclosure. Token projects, NFT launches, or staking ventures can easily overlap with securities laws. Treating them as “unregulated” side projects is risky.

Learn more about tokenized securities →

“Once it’s approved, I don’t have to think about it again”

Approval is not the end of the process. Firms must supervise PSTs, and employees must report changes if the activity evolves. A role that starts as unpaid or minor can become significant over time, requiring new review or disclosure updates.

How Fintech Firms Can Manage Outside Business Activities

Managing outside business activities effectively requires more than collecting forms. Fintech businesses need a structured approach that balances regulatory expectations with the fast-moving nature of startups and innovative financial products.

The main components of effectively managing OBAs include:

Building Clear Policies and Training Employees

Policies should define what counts as an outside business activity and outline how employees should disclose them.

Training is equally important. New hires and existing staff must understand that both compensated and uncompensated roles qualify. Real-world examples help clarify where regulators draw the line between personal and professional activity.

Using Disclosure Forms and Approval Workflows

A standardized disclosure form is the backbone of any OBA process. Employees should provide details about the activity’s nature, time commitment, compensation, and potential overlap with the company's business. An approval workflow, whether manual or software-driven, ensures submissions reach the right decision-makers and responses are documented.

Learn how Regly’s employee compliance can help you with approval workflow →

Risk-Based Review (High-Risk vs. Low-Risk OBAs)

Not all OBAs present the same level of concern.

Investment-related activities, like private securities transactions or crypto advisory work, require in-depth review.

Lower-risk activities, like coaching a sports team or occasional freelance work, may only need basic documentation. A risk-based approach helps compliance teams allocate resources efficiently.

Monitoring Approved OBAs With Conditions

Approval does not end the process. When needed (prohibiting the use of client contacts, restricting work hours, or requiring periodic updates), firms should set conditions and monitor for compliance. Supervisory oversight must be documented so that regulators can see how the firm evaluated and managed the risks over time.

Leveraging Compliance Technology and Automation

Manual processes often break down as a firm scales. Automating OBA intake, review, and recordkeeping reduces the likelihood of missed disclosures or incomplete documentation.

Platforms like Regly give fintechs a way to centralize OBA management, streamline approvals, and maintain an auditable trail for regulators.

Best Practices for Compliance Teams

Even with clear policies, compliance teams need practical routines to manage outside business activities consistently. The following practices help fintech firms mitigate regulatory risks while keeping oversight manageable.

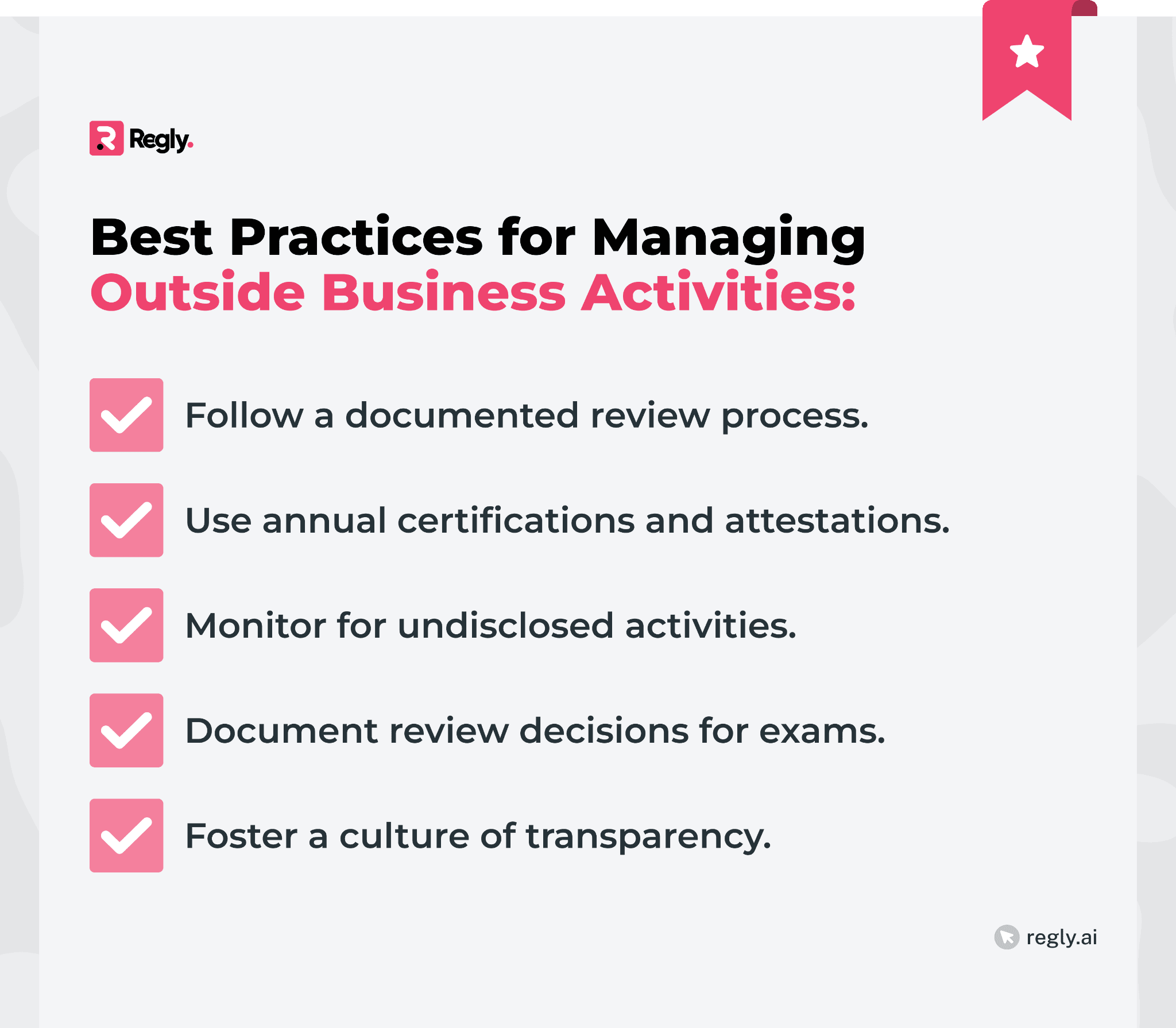

Step-by-Step OBA Review Process

A documented review process is essential. Each OBA disclosure should follow a clear path: employee submission → compliance review → conflict assessment → decision (approve, approve with conditions, or deny). Recording each step creates a defensible audit trail for exams and protects the firm if questions arise later.

Annual Certifications and Attestations

Outside activities change over time, and firms can’t rely on one-time disclosures. Annual certifications give employees an opportunity to confirm their OBA status or update compliance on new commitments. Some firms also require quarterly attestations for higher-risk roles.

Regly’s employee compliance tools help in automating this cycle, making it easier to distribute questionnaires and track responses →

Monitoring for Undisclosed Activities (Public Records, Social Media)

Firms should anticipate that not every OBA will be voluntarily disclosed. Monitoring tools and processes, like scanning public records, LinkedIn profiles, or business registrations, can help identify red flags. A sudden lifestyle change, frequent travel, or unexplained absences may also warrant a closer look.

Firms often apply similar monitoring when supervising outside brokerage accounts, where undisclosed trading can expose the firm to conflicts or compliance gaps.

Documenting Decisions for Exam Readiness

Regulators expect evidence of careful review. Compliance teams should record the rationale behind every approval or denial, noting why the activity was considered low or high risk.

Well-documented files reduce vulnerability during exams and protect the firm in the event of disputes with clients or regulators.

Creating a Culture of Transparency

Employees are more likely to disclose OBAs if they believe the firm will give fair consideration rather than blanket denials. Training sessions, leadership messaging, and case studies all help foster a culture where disclosure is seen as routine and protective, not punitive. This cultural element often determines whether compliance hears about OBAs early or only after a regulator does.

—

Outside business activities are a core compliance concern in financial services and fintech. Regulators like FINRA and the SEC view them as potential sources of conflict, client harm, and reputational risk.

A strong OBA compliance program combines clear policies, employee training, structured review workflows, and ongoing monitoring. It also requires careful recordkeeping and timely updates to regulatory filings like Form U4 and Form ADV.

When done well, OBA oversight can protect both the company and its employees while reinforcing a culture of transparency.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.