Outside brokerage accounts can create visibility gaps for compliance teams. If left unchecked, they may become channels for conflicts of interest, misuse of material nonpublic information, or violations of firm policies.

Handling outside brokerage accounts is a part of employee compliance responsibilities. Regulators expect employers to know where their employees trade securities, monitor that activity, and evaluate whether it raises regulatory or reputational risks.

This article explores what outside brokerage accounts are, why they matter for compliance, and how regulators expect firms to monitor them, covering the rules set by FINRA and the SEC, common challenges firms face in monitoring these accounts, and frequent misconceptions that trip up startups and growth-stage fintechs.

What Are Outside Brokerage Accounts?

An outside brokerage account is any personal investment account that an employee of a regulated business maintains at a financial institution outside of their employer.

What makes it “outside” is that it falls beyond the firm’s direct custody and supervision. Regulators treat these accounts as part of an employee’s beneficial interest if the employee controls the account or gains economic benefit from it.

This means the definition extends beyond accounts in the employee’s own name. It also covers accounts held by spouses, dependent children, or others where the employee has influence or financial ties. The key factor is whether the employee can trade securities or benefit from those trades.

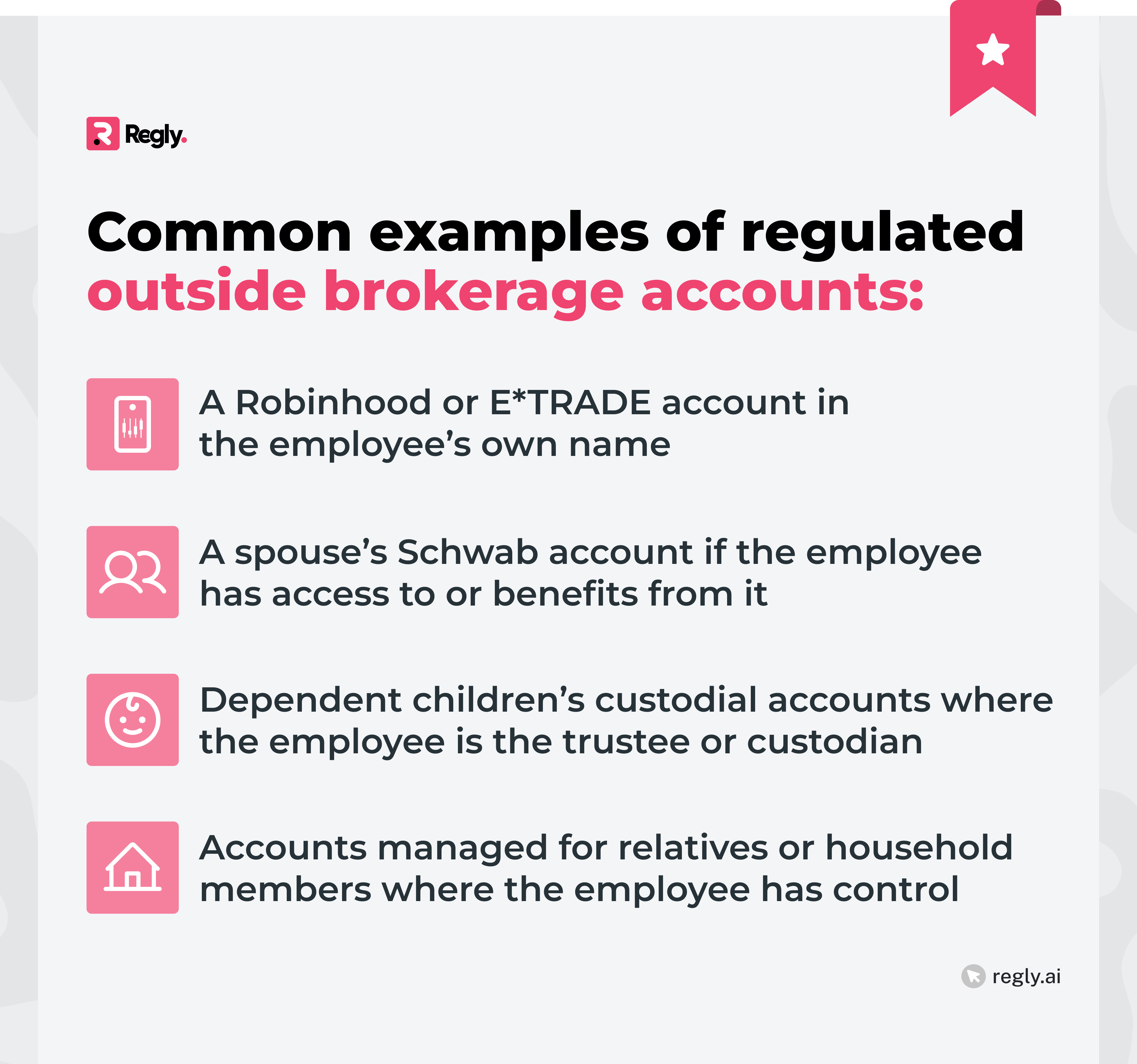

Examples of Accounts That Qualify

For compliance purposes, these are all treated as outside brokerage accounts, even if the employee believes they are “personal” or “separate.”

Why Regulators Care About Outside Brokerage Accounts

Outside brokerage accounts can create blind spots for compliance teams. If an employee executes trades in an undisclosed account, the firm may not detect potential conflicts. That includes front-running client orders, trading securities on the restricted list, or using material nonpublic information.

Regulators view these risks as systemic: a single undisclosed account can be enough for improper trading to occur without supervision. This is why FINRA and the SEC treat outside accounts that can trade securities as part of a firm’s supervisory obligations rather than a private matter.

The common thread is that businesses are expected to:

Know where employees maintain trading accounts

Monitor those accounts for activity that could conflict with firm or client interests

Document their supervisory efforts so regulators can evaluate them during exams

In practice, regulators see effective oversight of outside brokerage accounts as a test of whether a firm takes compliance seriously. Weak controls can lead to findings, fines, or personal sanctions for compliance officers.

See how Regly helps fintechs simplify employee compliance oversight, from disclosures to trade monitoring →

FINRA’s Regulatory Framework

For broker-dealers, FINRA sets the rules that govern how businesses must supervise outside brokerage accounts. These rules are binding obligations that regulators check during exams.

FINRA Rule 3210: Accounts at Other Broker-Dealers

The most relevant is FINRA Rule 3210, which outlines how employees and firms should handle accounts that can trade securities at other broker-dealers or financial institutions.

Rule 3210 requires employees to obtain written consent from their employer before opening or maintaining an outside brokerage account. It also obligates the employee to notify the outside institution of their association with a FINRA member firm. Once the account is opened, the firm has the right to request duplicate trade confirmations and account statements for supervisory review.

This framework provides companies with visibility into employee trading activity that would otherwise take place outside their direct supervision. The expectation is that compliance staff use this data to detect risks such as insider trading, restricted list violations, or front-running.

Treatment of Spouse and Household Accounts

FINRA Rule 3210 also extends beyond the employee’s own accounts. Accounts held by a spouse, dependent children, or anyone financially supported by the employee are presumed to be beneficially owned by the employee.

Unless the employee can demonstrate they have no control or economic interest in the account, which is rare, these accounts must be disclosed and supervised like the employee’s own.

Accounts That May Be Exempt

Not all accounts fall under the same reporting requirements. Certain limited-purpose accounts are excluded under FINRA rules because they carry less risk of conflicts or insider trading and can only trade specific securities as noted below.

Examples include:

Mutual fund-only accounts

529 college savings plans

Unit investment trusts

Variable annuities

These exemptions are narrow. Any account capable of trading equities, bonds, or options is generally subject to disclosure and monitoring. The safest approach for firms is to instruct employees: when in doubt, disclose the account.

SEC Rule 204A-1: Investment Adviser Code of Ethics

For investment advisors, the SEC takes a parallel but distinct approach to outside brokerage accounts. Under Rule 204A-1 of the Investment Advisers Act, businesses must adopt a Code of Ethics that sets standards for personal trading by “access persons.”

An “access person” is any employee who has access to client trading information or investment recommendations. For these employees, the rule requires:

Initial and annual holdings reports that include all personal and outside brokerage accounts

Quarterly securities transaction reports that capture every security trade made, including those in outside accounts

Pre-approval (pre-clearance) for certain trades, such as IPOs or limited offerings

These requirements create a continuous record of employee trading activity, designed to disclose all securities trading activity and identify potential conflicts with client interests.

How It Applies to Outside Brokerage Accounts

Even though Rule 204A-1 does not use the phrase “outside brokerage accounts,” the reporting obligations make it clear that advisors must track employee security transactions. The principle is the same as under FINRA: firms need visibility into accounts where employees can trade securities.

Practical Implications for Firms

Advisors must build systems to collect and review these reports and to follow up on unusual trades. Many firms rely on quarterly certifications from employees that their outside accounts have been disclosed and monitored.

Learn how Regly helps fintechs monitor employee compliance →

During SEC exams, regulators typically request these certifications and the supporting review documentation.

Outside Brokerage Accounts Requirements for Firms

Both FINRA and the SEC expect firms to take an active role in supervising employees outside brokerage accounts. These requirements involve ongoing oversight, structured processes, and thorough documentation.

Written Supervisory Procedures (WSPs) Requirements

Companies must set out in their WSPs how they handle outside brokerage accounts. A regulator reviewing your program will expect to see:

A clear definition of what counts as an outside brokerage account

Steps for obtaining prior consent before accounts are opened

How duplicate statements or electronic feeds are collected

The review process, including who is responsible and how exceptions are escalated

A generic policy is rarely enough. WSPs should reflect the firm’s actual practices, including how they handle hard-to-monitor accounts.

Prior Consent and Disclosure Obligations

Employees are required to get written approval from their employer before opening an outside brokerage account. This consent allows the firm to establish monitoring procedures from the start.

Regulators expect new hires to also disclose any existing accounts promptly. Businesses typically require a disclosure form at onboarding and periodic attestations confirming the employee has opened no new accounts without approval.

Duplicate Statements and Electronic Data Feeds

Regulators expect fintech businesses to receive account activity directly from the outside institution or through secure data feeds. This gives compliance teams visibility into trades without relying solely on employees.

Where feeds are unavailable, firms should establish a documented manual process, for example, requiring employees to upload monthly statements. Gaps in collection are a frequent focus during exams and enforcement cases.

Quarterly and Annual Reporting Under SEC Rules

For investment advisors, Rule 204A-1 requires quarterly transaction reports and annual holdings reports from access persons. These reports must cover all brokerage accounts that can trade securities and allow the firm to compare personal trading against client activity.

Regulators typically test this during exams by asking for employee certifications and reviewing how the firm followed up on flagged trades. Firms that cannot produce a complete audit trail face scrutiny.

Common Compliance Challenges

Supervising outside brokerage accounts is rarely straightforward. Even companies with well-written policies encounter obstacles when trying to capture disclosures, collect account data, and review trades consistently.

The most common challenges include:

Employees Failing to Disclose Outside Accounts: Employees may assume personal accounts don’t need to be reported, or they may overlook spouse and household accounts. Regulators treat nondisclosure as a serious issue, especially when it prevents the firm from spotting conflicts of interest.

Monitoring Accounts at Institutions Without Data Feeds: Not every brokerage or trading platform provides electronic data feeds. This creates blind spots that firms must address manually, often by requiring employees to upload statements or requiring duplicate statements to be provided by the firm executing the securities transactions.

Reviewing High Volumes of Trading Data: For growing fintechs, the volume of outside account activity can quickly exceed what a small compliance team can review line by line. Without structured workflows or automated compliance tools, firms risk missing red flags such as trading restricted securities or patterns suggesting insider use of information.

Remote Work and Delayed Reviews: The shift to remote and hybrid work has highlighted weaknesses in supervision. Some companies fell behind on reviewing outside account activity during periods of disruption. Regulators have since emphasized that reviews must be timely and documented, regardless of where compliance staff work.

Misconceptions About Outside Brokerage Accounts

Even experienced professionals sometimes misunderstand the rules around outside brokerage accounts. These misconceptions can lead to disclosure gaps, weak supervision, and compliance findings during exams:

“These Accounts are Prohibited”

Industry rules do not ban outside brokerage accounts, but firms can prohibit them. Employees can be allowed to maintain them, but only with prior consent and proper supervision. The goal is visibility and securities monitoring. Problems arise when accounts are opened without disclosure or monitored outside the firm’s procedures.

Confusing Outside Brokerage Accounts With Outside Business Activities

It’s common to confuse personal trading accounts with outside business activities (OBAs). They are separate issues.

OBAs cover paid employment or business ventures outside the firm, while outside brokerage accounts involve personal investing. Both require disclosure, but different rules govern them.

Believing Only Registered Reps Must Disclose Accounts

The rules apply broadly. Under FINRA, all “associated persons,” not just registered representatives, must disclose outside brokerage accounts.

For investment advisors, the SEC requires access persons to report their accounts. Assuming the rules only apply to licensed staff can be a costly mistake.

Underestimating Regulators’ Expectations for Startups

Some founders assume regulators will overlook gaps in outside account supervision at smaller or early-stage firms. In practice, regulators hold startups to the same standards as established broker-dealers or advisors. Weak controls in this area are often treated as evidence of broader compliance shortcomings.

Best Practices for Managing Outside Brokerage Accounts

Policies and regulations set the framework, but businesses need practical methods to make outside brokerage account supervision workable day to day. The following best practices reflect what regulators expect to see during exams and what compliance teams can implement to keep oversight efficient and consistent.

See how Regly turns employee compliance best practices into daily workflows →

Clear Policies and Employee Training

Effective supervision starts with policies that employees can understand and follow. A written policy should define what qualifies as an outside brokerage account, outline the approval process, and explain reporting timelines.

But the policy alone isn’t enough. Employees need training that explains the “why.” Connecting the rules to real-world risks, like insider trading cases or regulatory fines, makes compliance less abstract. Businesses that integrate this training into onboarding and reinforce it annually find that employees are less likely to overlook disclosures or assume accounts are exempt.

Centralized Disclosure and Attestations

Scattered processes often create gaps. A centralized system for account disclosure, whether it’s a portal, compliance software, or a structured internal form, gives compliance teams a single source of truth.

Periodic attestations add an extra layer of accountability. For example, a quarterly certification requiring employees to confirm that all outside brokerage accounts are disclosed can surface new accounts that may have been opened without approval. These certifications also serve as evidence during exams, showing that the firm takes proactive steps to maintain oversight.

Learn how Regly’s employee compliance tool can help you centralize disclosures and attestations →

Automating Trade Data Collection and Review

Collecting duplicate statements manually is one of the biggest operational burdens in compliance. Employees and broker-dealers may forget to forward statements, or data may arrive late and incomplete.

Automated feeds mitigate these risks by sending trade data directly from outside institutions to the compliance team. Once collected, automation can help prioritize reviews by flagging exceptions. This allows compliance officers to spend their time investigating higher-risk situations instead of combing through every routine transaction.

Handling Hard-to-Monitor Accounts

Not all accounts provide clean data feeds. For accounts at foreign brokers or crypto exchanges that can trade securities, firms may need employees to upload statements or securities transaction histories on a fixed schedule. Some firms also limit the types of trades allowed in such accounts to reduce risk.

Documentation and Audit Readiness

Supervision is only as strong as the records that support it. Regulators expect to see logs showing when statements or feeds were received, who reviewed them, and what issues were flagged. If an investigation took place, for example, when an employee traded a restricted security, the firm should also document the resolution.

These records form the backbone of audit readiness. Without them, even a strong process may appear weak during an exam. Building a discipline of consistent documentation not only protects the firm but also supports compliance officers if decisions are ever challenged.

—

Outside brokerage accounts may look like personal matters, but regulators view them as a core part of a firm’s supervisory responsibilities. Both FINRA and the SEC expect firms to know where employees hold securities trading accounts, monitor the securities trading activity, and keep records that prove oversight.

The challenges are real: undisclosed accounts, platforms without data feeds, heavy review workloads, and the added complexity of remote or hybrid teams. But businesses that build clear policies, centralize disclosures, automate data collection, and maintain strong documentation put themselves in a stronger position during exams and mitigate the risk of missing red flags.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.