What do you do if your influence campaign falls under FINRA and SEC scrutiny? Broker-dealer marketing is no longer limited to print ads and static website pages. It includes social media posts, mobile app notifications, product comparison charts, and even chatbot conversations.

For regulated firms, each of these communications can be scrutinized by FINRA and the SEC.

Marketing is where growth strategy and regulation tend to meet head-on. A bold headline about higher returns, a gamified trading feature, or a referral bonus campaign can all introduce risks that aren’t obvious at first glance. This article takes a closer look at the compliance rules that shape how broker-dealers market their products.

You will see how communications are classified, what content standards apply, when filings are required, how Reg BI affects promotional activity, and where fintech models face heightened risk.

What Is Broker-Dealer Marketing?

Broker-dealer marketing covers any communication distributed by a registered broker-dealer that could influence an investor’s decision. Under FINRA Rule 2210, this generally falls under the broader category of “communications with the public.”

This includes traditional advertisements, but it also extends to:

Website landing pages

Email campaigns

Social media posts

Sponsored content

Webinars and slide decks

Mobile app messages and push notifications

Influencer promotions

Chatbot responses that discuss products or services

If a communication promotes the firm, its services, or specific securities, regulators will likely treat it as marketing. The format does not matter. The substance does.

Broker-dealer marketing is regulated because it can shape investor behavior. A comparison chart between two funds, a statement about trading costs, or a description of a margin feature may all fall within FINRA’s communications rules. Even content labeled as “educational” can become marketing if it implicitly encourages account openings or product usage.

Learn how FINRA evaluates advertising content and enforcement trends →

Retail vs. Institutional Communications

Not all broker-dealer marketing is treated the same. FINRA distinguishes communications based on the audience receiving them. That classification determines approval, filing, and supervisory obligations.

Under Rule 2210, communications generally fall into three categories:

Category | Audience | Key Compliance Impact |

|---|---|---|

Retail Communications | More than 25 retail investors within 30 calendar days | Principal pre-approval typically required |

Correspondence | 25 or fewer retail investors within 30 calendar days | Supervision required, no pre-use approval in most cases |

Institutional Communications | Institutional investors only | No principal pre-approval required, but supervision still required |

Retail investors include individuals and certain non-institutional entities. Institutional investors include banks, insurance companies, registered investment companies, and certain large entities meeting asset thresholds.

Here are a few key points to keep in mind:

Retail communications usually require prior principal approval before first use.

Institutional communications are not subject to pre-use approval, but firms must still supervise them under written supervisory procedures.

If an institutional communication is forwarded to retail investors, it may be reclassified as retail.

In practice, most digital broker-dealer marketing is retail. Public websites, social media posts, app notifications, and online ads typically target or reach retail investors. Firms should classify communications at the design stage, not after publication.

Correspondence vs. Public Communications

In broker-dealer marketing, the line between correspondence and public communications affects approval, supervision, and compliance exposure. The distinction turns primarily on audience size and distribution method:

Feature | Correspondence | Public Communications |

|---|---|---|

Audience Size | 25 or fewer retail investors within 30 days | More than 25 retail investors within 30 days |

Typical Format | Direct emails, one-to-one messages, limited outreach | Websites, ads, social media posts, webinars, mass emails |

Principal Pre-Approval | Generally not required | Retail communications typically require prior principal approval |

FINRA Filing Risk | Rare | Possible, depending on content and firm status |

Supervisory Review | Required under Rule 3110 | Required under Rule 3110 |

Correspondence is narrower and more targeted. It covers limited communications to a small number of retail investors.

Public communications are much broader and more heavily regulated. Many types of digital marketing activity, including social media campaigns and app-based promotions, fall within this category.

In practice, many compliance breakdowns occur when firms misclassify broadly distributed digital content as correspondence. Distribution volume and accessibility matter more than intent.

Static vs. Interactive Content

FINRA also distinguishes between static content and interactive content in broker-dealer marketing. The format affects approval requirements, but not content standards.

Static content remains posted and does not change in response to user input. Examples include:

Website landing pages

Online banner ads

Pre-recorded videos

PDF brochures

Sponsored posts

Static retail communications generally require principal approval before first use.

Interactive content, by contrast, involves real-time or conversational exchanges. Examples include:

Social media comment threads

Live chat responses

Real-time Q&A sessions

Interactive forum posts

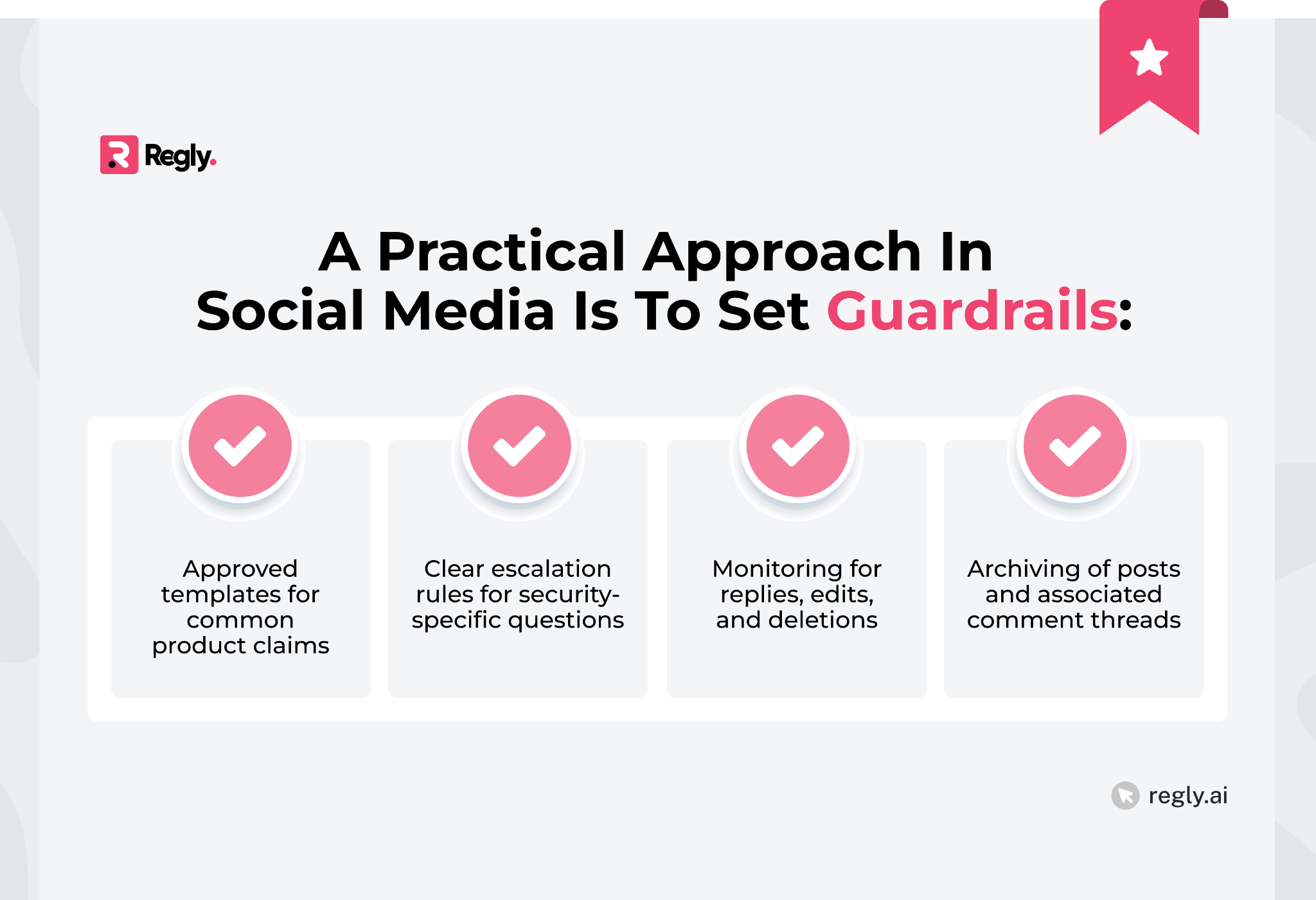

FINRA has stated that most interactive postings will be treated as retail communications; however, FINRA has also generally granted exemptions from pre-use approval and filing requirements. But that doesn’t alleviate supervision. All interactive content posted on behalf of a firm must be monitored, retained for a reasonable period of time, and reviewed by the firm in accordance with FINRA Rule 3110.

Compliance risk escalates significantly when interactive content (e.g., comments) blurs the line to recommendations. When a representative responds to a comment about a specific stock, the response may raise issues under suitability or Reg BI.

For fintech platforms, the regulatory consideration extends beyond just the respondent/representative. For example, chatbots, automated responses, and AI-generated prompts are not "exempt" simply because they are automated. As long as the firm distributes the content, it is considered broker-dealer marketing, whether created by a human or a system.

Marketing vs. Educational Content

Many firms assume that labeling content as “educational” removes it from broker-dealer marketing rules. That’s not how regulators approach it.

If the communication could influence an investor’s decision, it may still be treated as marketing. The label does not control the analysis. The substance does.

Here’s what both types of content typically show:

Educational content does | Marketing content highlights |

|---|---|

Explain general market concepts | Trading features |

Describes how a product category works | Fee comparisons |

Avoids discussing specific securities | Performance data |

Does not encourage account openings or | Account incentives |

Does not encourage transactions | Product advantages or features |

The lines of what constitutes "educational" versus marketing content are further blurred in fintech. A blog that explains how options trading works becomes marketing when it provides a link to open up an account or to the margin feature. If a broker-dealer holds a webinar labeled “educational,” but specifically mentions one of their own product offerings, the webinar can also be classified as retail communication.

Regulators don’t look at labels; they look at the full picture. Where the content lives, what it points to, how it’s framed, and whether there’s a call to action all factor into the analysis.

For growing teams, this is where discipline matters. If a piece of content is designed to move the business forward, it should go through a compliance review, even if it presents itself as purely informational. Having a clear, practical review framework in place helps catch those gray areas before anything goes live.

The Regulatory Framework Governing Broker-Dealer Marketing

Broker-dealer marketing sits within a layered regulatory structure. FINRA sets the primary communications rules, while the SEC enforces federal securities laws and anti-fraud standards. State regulators and other agencies may also have jurisdiction depending on the activity.

Here is the overall regulatory framework around broker-dealer marketing:

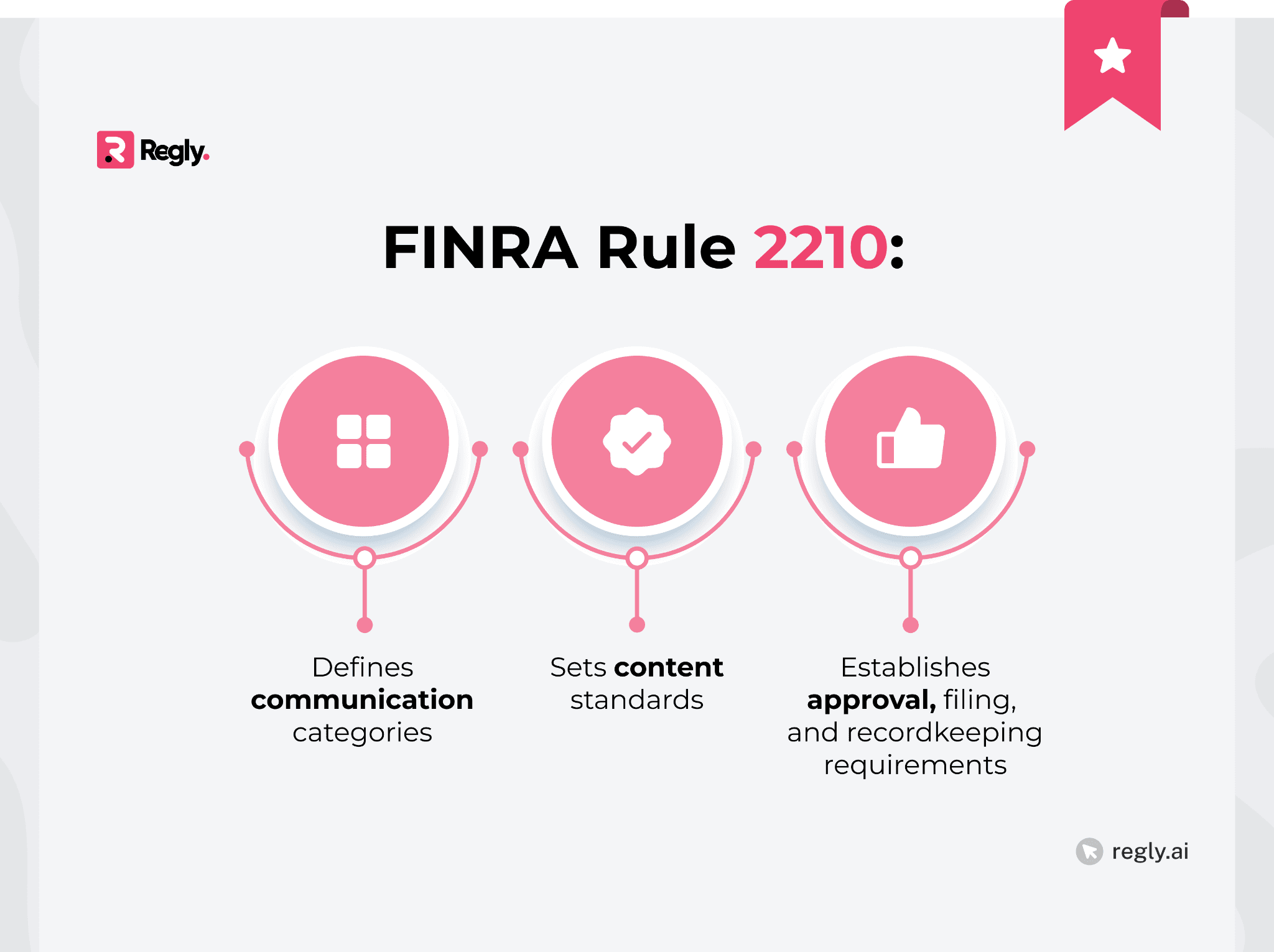

FINRA Rule 2210: Communications With the Public

FINRA Rule 2210 is the core rule governing broker-dealer marketing. It applies to all communications with the public, including retail communications, correspondence, and institutional communications.

The rule does three things:

At its core, Rule 2210 requires that broker-dealer marketing be fair and balanced and not contain false, exaggerated, unwarranted, promissory, or misleading statements. It also prohibits omitting material information if the omission would make the communication misleading.

Key areas regulated under Rule 2210 include:

Performance presentations

Comparisons and rankings

Testimonials

Product descriptions

Risk disclosures

Use of charts and statistics

For retail communications, Rule 2210 generally requires principal approval before first use. Certain categories of communications may also require filing with FINRA’s Advertising Regulation Department.

What matters here is not the format. Whether it’s a static webpage, a paid social ad, or a message inside your app, the rule can still apply. The channel doesn’t change how regulators evaluate it.

For fintech broker-dealers, Rule 2210 often shows up in product design, not just marketing. The language in your app, onboarding flow, or feature descriptions can all count as communications with the public. That means compliance review shouldn’t stop at traditional ads. It needs to cover those in-product moments, too.

SEC Anti-Fraud Provisions and Exchange Act Considerations

FINRA Rule 2210 is not the only authority governing broker-dealer marketing. SEC anti-fraud provisions apply to all communications, regardless of format or audience.

Key statutory provisions include:

Section 17(a) of the Securities Act

Section 10(b) of the Exchange Act

Rule 10b-5 under the Exchange Act

These provisions are meant to stop statements that are false, misleading, or missing key information when securities are being offered or sold. Unlike Rule 2210, they are not limited to communications categories. They apply broadly.

For broker-dealer marketing, this means:

Claims must be accurate and supportable

Material risks cannot be buried or minimized

Fee disclosures must align with actual practices

Marketing statements must match operational reality

The SEC prioritizes what that information says over how it’s presented. An accurate technical description of a product may mislead investors if it creates a distorted view of either the cost to buy, operate, or maintain the product, the risk, or expected results.

Books and records obligations intersect with those of the Exchange Act. Therefore, companies must retain all marketing materials, including social media posts and other forms of digital communications, for at least three years pursuant to Rule 17a-4. Companies that fail to keep these communications may violate the rule.

For fintech firms, this is especially important. Due to their ability to rapidly create new products, changes in product features may happen before a firm has updated its marketing materials. This could lead to increased anti-fraud liability for both the firm and those working on its behalf.

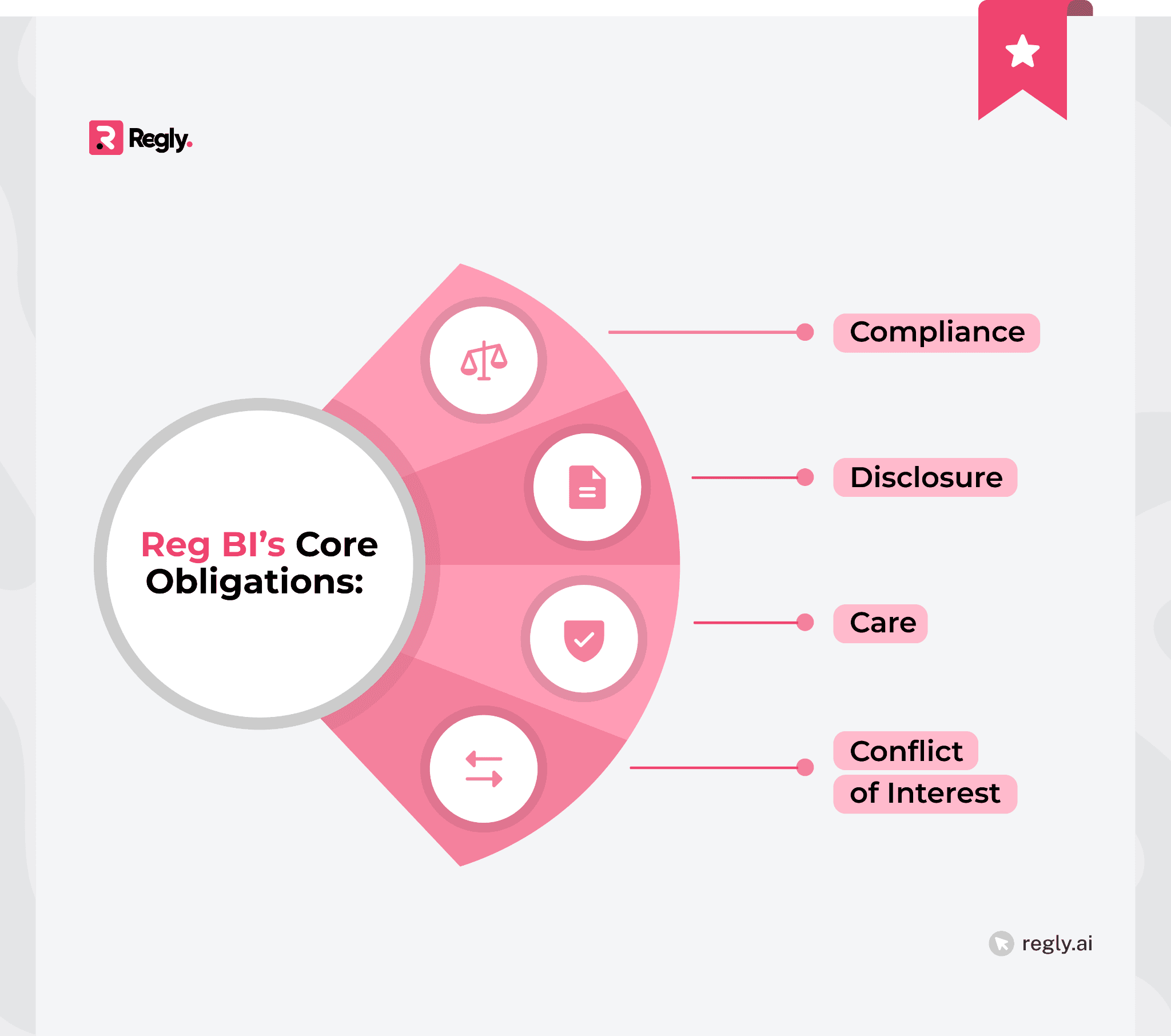

Regulation Best Interest and Marketing Implications

Regulation Best Interest, or Reg BI, applies when a broker-dealer makes a recommendation to a retail customer. Marketing content can trigger Reg BI if it crosses from general promotion into a recommendation.

The key question is whether the communication could reasonably be viewed as suggesting a specific security, account type, or transaction.

Examples that may raise Reg BI concerns include:

Highlighting a specific product as “ideal” for certain investors

Promoting margin or options trading with targeted language

Comparing proprietary products in a way that steers investors

Gamified prompts encouraging frequent trading

When marketing becomes a recommendation, the broker-dealer must comply with Reg BI’s four core obligations:

Reg BI also requires that firms act in the retail customer’s best interest and not place their own interests ahead of the customer’s. Disclosure alone is not enough.

In practice, those self-interests show up in marketing. Compensation structures, sales contests, and referral bonuses all need a closer look for potential conflicts. And when you’re promoting revenue-generating features like payment for order flow, margin, or securities lending, the messaging has to stay tightly aligned with what’s actually disclosed.

Reg BI Risk in Broker-Dealer Marketing

Regulation Best Interest applies when a broker-dealer makes a recommendation to a retail customer. In practice, broker-dealer marketing can cross that line more easily than firms expect.

The regulatory focus is not on how the firm labels the content. It is how a reasonable retail investor would interpret it. If a marketing statement could reasonably be viewed as steering an investor toward a specific security, account type, or strategy, Reg BI may apply.

This section breaks down where marketing activity most often creates Best Interest exposure:

Marketing Statements That Trigger Best Interest Concerns

General brand advertising typically does not trigger Reg BI. However, statements that suggest a specific course of action may.

Examples that raise scrutiny include:

“This ETF is ideal for income-focused investors.”

“Upgrade to margin to maximize returns.”

“Our options platform is built for aggressive traders.”

Prompts encouraging the purchase of a specific trending security

Targeted digital messaging increases risk. Personalized prompts based on account behavior may look less like advertising and more like individualized recommendations.

When broker-dealer marketing moves from general promotion to product steering, firms must evaluate Care, Disclosure, Conflict, and Compliance obligations under Reg BI.

Conflicts of Interest in Promotional Materials

Marketing content often highlights revenue-generating features. That is not prohibited. The issue is how conflicts are disclosed and managed.

Common conflict areas in broker-dealer marketing include:

Payment for order flow

Revenue sharing arrangements

Margin lending

Securities lending programs

Proprietary product promotion

If marketing emphasizes features that generate higher firm revenue, regulators may examine whether disclosures are clear and whether supervisory controls address associated conflicts.

Reg BI requires firms to identify and mitigate or eliminate certain conflicts. Promotional materials should not downplay conflicts that are material to the investor’s decision.

Compensation Disclosures and Incentives

Sales incentives and compensation structures frequently intersect with marketing campaigns. Examples include:

Cash bonuses for account openings

Trading contests

Referral rewards

Volume-based affiliate compensation

These programs can create behavioral pressure that conflicts with a retail investor’s best interest. Marketing materials promoting these incentives must align with internal compensation disclosures and supervisory controls.

Clear eligibility criteria and conditions should be disclosed. Time limits, minimum balances, and trading thresholds must be presented transparently.

From a compliance perspective, marketing language should reflect how the incentive actually operates. Misalignment between promotional copy and operational mechanics increases exam risk.

Product-Specific Campaign Risks

Certain products carry heightened regulatory expectations. Marketing tied to these products deserves additional scrutiny.

High-risk product categories include:

Options and leveraged ETFs

Margin accounts

Structured products

Crypto-related offerings

Complex fixed income instruments

Campaigns promoting these products should include proportionate risk disclosures and avoid minimizing volatility, liquidity, or complexity.

For fintech broker-dealers, digital distribution amplifies reach. A push notification promoting options trading can reach thousands of retail investors instantly. That scale requires disciplined review before launch.

Reg BI risk in broker-dealer marketing is rarely about a single sentence. It is about how messaging, compensation, and product structure interact. Firms that analyze campaigns through that broader lens are better positioned during regulatory examinations.

Form CRS Consistency Requirements

Form CRS is not a marketing document, but it directly affects broker-dealer marketing. Marketing statements must be consistent with the disclosures made in Form CRS.

Broker-dealers are required to:

Deliver Form CRS to retail investors

Post it prominently on their website

Describe services, fees, conflicts, and disciplinary history in plain language

During exams, regulators routinely pull marketing materials alongside Form CRS to see if the story holds together. When it doesn't, that inconsistency becomes its own problem. It raises questions about credibility and usually invites deeper scrutiny.

For firms where the product is still taking shape, this means building in a regular check between what marketing publishes versus what’s stated on Form CRS. Pricing updates, new revenue streams, or product pivots aren't just operational changes; they're triggers to revisit both documents.

In reality, it’s less about drafting and more about governing. The marketing team, legal department, and compliance will have a shared current reference copy of Form CRS for use in developing campaigns.

State Securities (Blue Sky) Considerations

Federal regulations are just one layer that affects how a Broker-Dealer markets its products. State Securities Regulators (often called "Blue Sky" authorities) may also review the marketing materials distributed by a broker-dealer within each state's jurisdiction.

While FINRA oversees communications for member firms, states retain authority to:

Enforce anti-fraud provisions

Review misleading advertising

Investigate sales practices tied to marketing campaigns

Examine state-registered representatives

Some offerings can also bring state-level requirements into play, especially for private placements or non-listed securities. That might mean notice filings or additional disclosures, depending on where investors are located.

For broker-dealers operating nationally through digital channels, marketing rarely stays contained. A single campaign can reach investors across multiple states at once, which naturally expands the number of regulatory touchpoints.

State regulators also tend to coordinate with FINRA and the SEC. So if an issue surfaces at the state level, it can quickly grow into a broader, multi-jurisdiction review.

Content Standards for Broker-Dealer Marketing

Once classification and jurisdiction are clear, the next focus is substance. Broker-dealer marketing must meet specific content standards designed to prevent misleading communications.

Most of these standards flow from FINRA Rule 2210, reinforced by SEC anti-fraud provisions. They apply across channels, including websites, social media, email campaigns, and in-app messaging.

Here is a detailed breakdown of what broker-dealer marketing should do:

Fair and Balanced Communications

At the core of broker-dealer marketing is a simple standard: communications must be fair and balanced. This requirement comes directly from FINRA Rule 2210 and is reinforced by federal anti-fraud principles.

“Fair and balanced” means benefits cannot be presented without adequate discussion of risks. A communication should provide investors with a sound basis to evaluate the information.

In practice, this affects how firms:

Describe product features

Present potential returns

Highlight cost advantages

Compare services to competitors

For example, promoting commission-free trading without clearly addressing other sources of revenue, such as payment for order flow, may create an imbalanced impression. The issue is not the existence of the revenue stream. It’s whether the communication presents a complete picture.

Visual presentation is part of the compliance picture, too. Burying risk disclosures in fine print while benefits run in bold headlines isn't a formatting choice regulators will overlook. They assess the overall impression a piece of marketing creates, not just whether the required language technically appears somewhere on the page.

For fintech broker-dealers, short-form marketing creates added pressure. Push notifications and app banners are brief by design. Even in constrained formats, communications must avoid overstating benefits or minimizing risk.

Ask yourself this: If an investor relied only on this communication, would they have a balanced understanding of the product’s potential benefits and material risks?

Prohibited Statements and Misleading Claims

Broker-dealer marketing cannot contain statements that are false, exaggerated, unwarranted, promissory, or misleading. This prohibition applies regardless of format or distribution channel.

Certain types of claims consistently attract regulatory scrutiny:

Statements suggesting guaranteed returns

Claims that minimize or dismiss risk

Assertions that a product is “safe” or “risk-free”

Implications that regulatory approval equals endorsement

Overstated comparisons to competitors

Technically accurate statements can still mislead when they're stripped of context. Advertising "top-performing strategies" without explaining the time period, how those strategies were selected, or what volatility looks like along the way gives investors an incomplete picture, and regulators treat that incompleteness as a problem.

Context matters. A bold headline promising “maximize income” followed by fine-print risk language may still create a misleading overall impression.

Firms should also avoid vague superiority claims. Terms like “best,” “leading,” or “number one” need to be backed by evidence. If rankings or awards are referenced, the basis must be disclosed clearly.

Required Disclosures and Risk Language

Broker-dealer marketing must include disclosures that provide investors with material information. Risk language should be clear, prominent, and proportionate to the claims being made.

Disclosures commonly address:

Investment risks

Fees and compensation structures

Conflicts of interest

Margin and options risks

Limitations of performance data

The presentation matters as much as the content. Disclosures should not be buried in footnotes if the headline makes a strong claim. Regulators evaluate the communication as a whole.

Here is how disclosure issues typically arise in broker-dealer marketing:

Marketing Claim | Required Consideration |

|---|---|

“Zero commission trading” | Clarify other revenue sources and potential costs |

“Advanced options strategies” | Include options, risk disclosure, and suitability considerations |

“High-yield opportunities” | Explain volatility, liquidity, and principal risk |

“Cash bonus for account opening” | Disclose eligibility conditions and time limits |

Hyperlinks can supplement disclosures in digital environments, but they cannot correct a misleading statement. The core message must stand on its own.

For fintech platforms, risk language should align with product mechanics. If a margin feature increases leverage exposure, the disclosure should reflect how that feature actually works.

Comparisons, Rankings, and Third-Party Data

Comparisons are common in broker-dealer marketing. Firms compare fees, performance, features, or execution quality. These claims are permitted, but they must be accurate and supported.

Any comparison must provide a sound basis for evaluation. Investors should understand what is being compared and how the comparison was constructed. A broker-dealer should not do the following to adhere to marketing compliance:

Omit relevant fees when comparing cost structures

Compare proprietary products against selective competitors

Use outdated performance periods

Highlight favorable metrics without explaining the methodology

Third-party data must also be vetted. Firms are responsible for the content they distribute, even if it originates from another source.

For example, citing a research firm’s “top platform” award without explaining the evaluation criteria may create a misleading impression. Investors may assume broader endorsement than actually exists.

Data-driven broker-dealer marketing efforts should retain an internal record of their marketing activities. The source material used to develop marketing content (i.e., news articles), calculations (e.g., averages) or other metrics, and supporting evidence (e.g., customer satisfaction surveys) should all be maintained by the firm as part of its books and records.

Use of Testimonials and Endorsements

Testimonials are permitted in broker-dealer marketing, but they are regulated. If a communication includes a testimonial about the firm’s services or performance, specific disclosures are required.

Under FINRA Rule 2210, broker-dealers must disclose that:

The testimonial may not be representative of the experience of other customers

The testimonial is not a guarantee of future performance or success

If compensation exceeds $100, the firm must also disclose that the testimonial is paid.

This area creates confusion because broker-dealers and registered investment advisors operate under different testimonial regimes. Broker-dealers follow FINRA Rule 2210. RIAs follow the SEC Marketing Rule under the Investment Advisers Act. The rules are not identical.

Influencer campaigns raise additional risk. If a third party promotes a broker-dealer’s services in exchange for compensation, regulators may treat that communication as the firm’s own marketing.

Approval, Supervision, and Recordkeeping Requirements

Broker-dealer marketing is not just about what you say. It’s also about how communications are reviewed, approved, supervised, and retained.

FINRA rules require firms to implement structured processes around retail communications, correspondence, and institutional communications. Those processes must be documented and reflected in written supervisory procedures.

Here are the core requirements surrounding approval, supervision, and recordkeeping:

Principal Pre-Approval Obligations

Most retail communications used in broker-dealer marketing require approval by a qualified registered principal before first use. This requirement comes directly from FINRA Rule 2210.

Pre-approval typically applies to:

Website content

Online advertisements

Email campaigns sent broadly to retail investors

Static social media posts

Digital brochures and presentations

The approval must be documented. Firms should retain evidence of the approving principal’s name, the date of approval, and the final version of the communication. Interactive content such as real-time posts may not require pre-use approval, but it remains subject to supervision.

Managing approvals, filings, and recordkeeping manually creates gaps that regulators look for. Regly’s marketing compliance module centralizes review workflows, automates approval tracking, and archives every communication without slowing down your campaigns.

FINRA Filing Requirements

In addition to principal approval, certain broker-dealer marketing materials must be filed with FINRA’s Advertising Regulation Department.

Filing requirements depend on the firm’s status and the content being distributed. For example:

New member firms are generally required to file retail communications at least 10 business days before first use during their first year of membership.

Certain product-specific materials, such as those related to registered investment companies or structured products, may require filing.

Failure to file when required is a procedural violation, even if the content itself is compliant. Firms should map filing triggers during campaign planning, not after launch.

Supervisory Procedures Under Rule 3110

FINRA Rule 3110 requires broker-dealers to establish and maintain written supervisory procedures covering communications.

These procedures should address:

Classification of communications

Review and escalation protocols

Supervision of correspondence and interactive content

Oversight of associated persons and third parties

Supervision is continuous and does not end when the initial approval process ends. Brokers-dealers should monitor communications both before and after they have been distributed to ensure that any online interactions between representatives and customers are being supervised.

Regulatory agencies generally review how firms’ supervisory procedures were followed versus what actually occurred during the course of a marketing campaign. Marketing operations that do not follow previously documented controls can lead to examination findings.

Books and Records Under Rule 17a-4

Broker-dealers must preserve marketing communications under Exchange Act Rule 17a-4 and related FINRA requirements.

Retention generally includes:

Final versions of communications

Dates of first and last use

Principal approval documentation

Source materials supporting performance or data claims

Electronic communications should be retained in compliant formats to keep your fintech’s audit trail updated. The SEC has modernized certain electronic recordkeeping requirements, but the obligation to keep complete and accurate records remains unchanged.

In broker-dealer marketing, documentation is often as important as the message itself. If a firm cannot produce records during an examination, that failure can become a separate violation.

Archiving Digital and Off-Channel Communications

Modern broker-dealer marketing extends beyond email and websites. Communications now occur across social platforms, messaging apps, collaboration tools, and mobile interfaces.

Firms must capture and retain:

Social media posts and comments

Direct messages involving business communications

In-app chat interactions

Influencer content created on the firm’s behalf

Unregulated off-channel communications present unique risks. Any discussion of security products and/or services by registered representatives via unauthorized media will likely fall under the regulatory umbrella of record-keeping and supervision rules.

For fintech broker-dealers, scale increases exposure. The objective is straightforward. Every regulated communication should be classifiable, reviewable, and retrievable.

High-Risk Channels in Modern Broker-Dealer Marketing

Not all broker-dealer marketing carries the same level of regulatory risk. Certain channels attract heightened scrutiny because of scale, speed, or historical enforcement patterns. Below, you’ll find the top four high-risk channels in modern marketing broker-dealers use:

Social Media and Interactive Posts

Social media is often treated as informal. Regulators do not view it that way. Broker-dealer marketing rules apply to social media content the same way they apply to websites or email.

Depending upon who has access to your social media posts, they could be categorized as retail communications, correspondence, or institutional communications. Based on what type of interaction you allow in response to a post, comments/threads, and real-time responses could require a different approval process. However, all must be monitored/supervised, and records must be maintained.

Common compliance risk areas include:

Promissory language or exaggerated claims in short posts

Product comparisons without clear assumptions or limitations

Statements about specific securities in public threads

Representatives responding to customer questions in ways that look like recommendations

Firms should also control account access and content ownership. If registered representatives use personal accounts for business communications, supervision and retention become harder.

Influencer and Affiliate Marketing Programs

Influencer campaigns have become common in broker-dealer marketing, especially among fintech firms targeting retail investors. Regulators have responded with focused examinations and enforcement actions.

When a broker-dealer compensates a third party to promote its services, that content is typically treated as the firm’s communication. The firm remains responsible for supervision, disclosures, and record retention.

Key compliance considerations include:

Reviewing and approving static influencer content before publication

Monitoring ongoing posts for accuracy and balance

Disclosing compensation arrangements clearly

Archiving sponsored posts and related communications

Risk increases when influencers discuss performance, trading strategies, or specific securities. Statements that appear casual can still be interpreted as promotional or even as recommendations.

Affiliate programs also raise compensation and conflict issues. If third parties are paid per account opened or per trade generated, firms should evaluate whether disclosures are sufficient and whether the structure creates regulatory concerns.

As marketing channels expand, so does regulatory exposure. Regly’s AI-powered compliance engine analyzes marketing content to flag misleading claims, missing disclosures, and Reg BI risks before they go live.

Mobile Apps, Push Notifications, and Behavioral Design

For many fintech broker-dealers, the primary marketing channel is the mobile app. Messaging is embedded directly into the product experience.

Push notifications, in-app banners, prompts, and feature highlights can all qualify as broker-dealer marketing. The fact that they appear inside a product does not remove them from communications rules.

Common risk areas include:

Notifications encouraging increased trading activity

Prompts highlighting margin or options features without a balanced risk context

Gamified elements tied to account funding or referrals

“Trending” or “popular” labels that may imply suitability

Firms should assess mobile communications through multiple lenses:

Rule 2210 content standards

Reg BI recommendation risk

Disclosure alignment with Form CRS

Books and records retention

Because app content evolves so quickly, version control becomes essential. Compliance teams need clear visibility into product and feature updates that could change how something is being promoted.

At scale, it’s not enough to review things after they go live. The more effective approach is to build compliance into the release cycle itself, with structured review workflows that move alongside product updates. In a mobile-first environment, marketing and product can’t operate on separate tracks from compliance.

Crypto Asset and Digital Asset Marketing

Crypto-related messaging continues to draw close scrutiny in broker-dealer marketing. Regulators have repeatedly flagged issues like unclear product descriptions, misleading claims, and confusion about which entity is actually providing the service.

It’s important for marketing to draw a clear line between broker-dealer offerings and any crypto services provided through affiliates or third parties. Investors should be able to tell who they’re dealing with and what protections, if any, apply to each service.

Common risk areas include:

Implying that SIPC protects crypto assets

Failing to explain custody structures

Comparing crypto accounts to traditional brokerage accounts without clarifying the differences

Highlighting potential returns without a balanced volatility discussion

If a broker-dealer markets access to digital assets through an affiliated platform, the communication should identify the legal entity involved and the scope of regulatory oversight.

Crypto messaging often moves quickly in response to market conditions. That increases the risk of exaggerated language during periods of volatility. Firms should maintain documented review controls for time-sensitive campaigns.

Read more about KYC crypto requirements →

AI-Generated Content and Chatbots

Automation does not change regulatory responsibility. If AI systems generate communications on behalf of a broker-dealer, the firm remains accountable for compliance.

Chatbots, automated email responses, and dynamic content engines can all fall within communications rules if they discuss products or services.

Key considerations include:

Whether AI responses could be interpreted as recommendations

Whether risk disclosures are incorporated into automated messaging

Whether conversations are retained under the books and records requirements

Whether model outputs are monitored for accuracy and drift

AI-driven personalization introduces additional complexity. Tailored prompts based on user behavior may raise Reg BI concerns if they steer investors toward specific products.

For fintech broker-dealers using generative systems at scale, oversight cannot be informal. Structured review parameters, output testing, and ongoing monitoring are necessary to manage risk.

Broker-Dealer Marketing for Fintech and Hybrid Models

Fintech broker-dealers often operate through hybrid structures. They may combine brokerage services with crypto access, lending features, payment tools, or embedded finance partnerships.

These blended models create additional complexity in broker-dealer marketing. These are the areas where risk tends to concentrate and where a closer look matters most:

Brokerage and Crypto Combinations

Many fintech platforms offer both securities brokerage and crypto trading. The distinction matters.

Marketing should clearly disclose:

Which entity executes securities transactions

Whether crypto assets are offered by an affiliate or a separate company

Whether SIPC coverage applies

The custody and risk structure of digital assets

Statements implying that crypto holdings receive the same regulatory protections as brokerage accounts can create misleading impressions.

Brand consistency should not override legal clarity. If services operate under separate registrations or licenses, that separation must be reflected in promotional materials.

App-Based and Gamified Experiences

Gamification is common in fintech environments. Features such as badges, leaderboards, streaks, and celebratory graphics can increase engagement.

However, when gamified elements encourage trading activity, regulators may examine whether they function as recommendations.

Risk areas include:

Prompts encouraging rapid or frequent trading

Notifications highlighting trending securities

Visual rewards tied to transaction volume

Simplified representations of complex products

Design decisions don’t just affect how an app looks; they influence how investors behave. That’s why compliance teams need to look closely at how app-based marketing lines up with Reg BI and suitability obligations.

Marketing and product are often intertwined in mobile-first broker-dealers. Review processes should account for both content and user interface mechanics.

Referral Programs and Cash Incentives

Referral bonuses and cash incentives are widely used to drive growth. They are permitted, but they create disclosure and conflict considerations.

Marketing materials should clearly describe:

Eligibility requirements

Minimum funding thresholds

Time limits

Any required trading activity

If incentives are tied to trading activity or account behavior, it’s important to take a hard look at whether that structure creates conflicts under Reg BI.

How you describe the program matters just as much as how it’s built. If the messaging oversimplifies how it works, it can lead to confusion, investor complaints, and tough questions during exams.

Embedded Finance and Affiliate Marketing

Some broker-dealers distribute services through third-party platforms or participate in embedded finance arrangements.

In these models, marketing may appear on partner websites, co-branded applications, affiliate content, and platform dashboards. Even so, the responsibility doesn’t shift. The broker-dealer is still accountable for communications made on its behalf, which makes oversight of partner-created content especially important.

Firms should define:

Approval rights over co-branded materials

Monitoring procedures for affiliate messaging

Record retention responsibilities

Clear identification of the regulated entity

Fintech models often scale through partnerships. Without documented supervisory control over distributed marketing content, regulatory exposure increases quickly.

Building an Effective Broker-Dealer Marketing Program

Strong broker-dealer marketing compliance is not built around isolated reviews. It’s built around a process.

An effective program connects classification, approval, supervision, and documentation into a repeatable workflow. When these elements operate separately, gaps appear during exams. The steps below outline a practical framework:

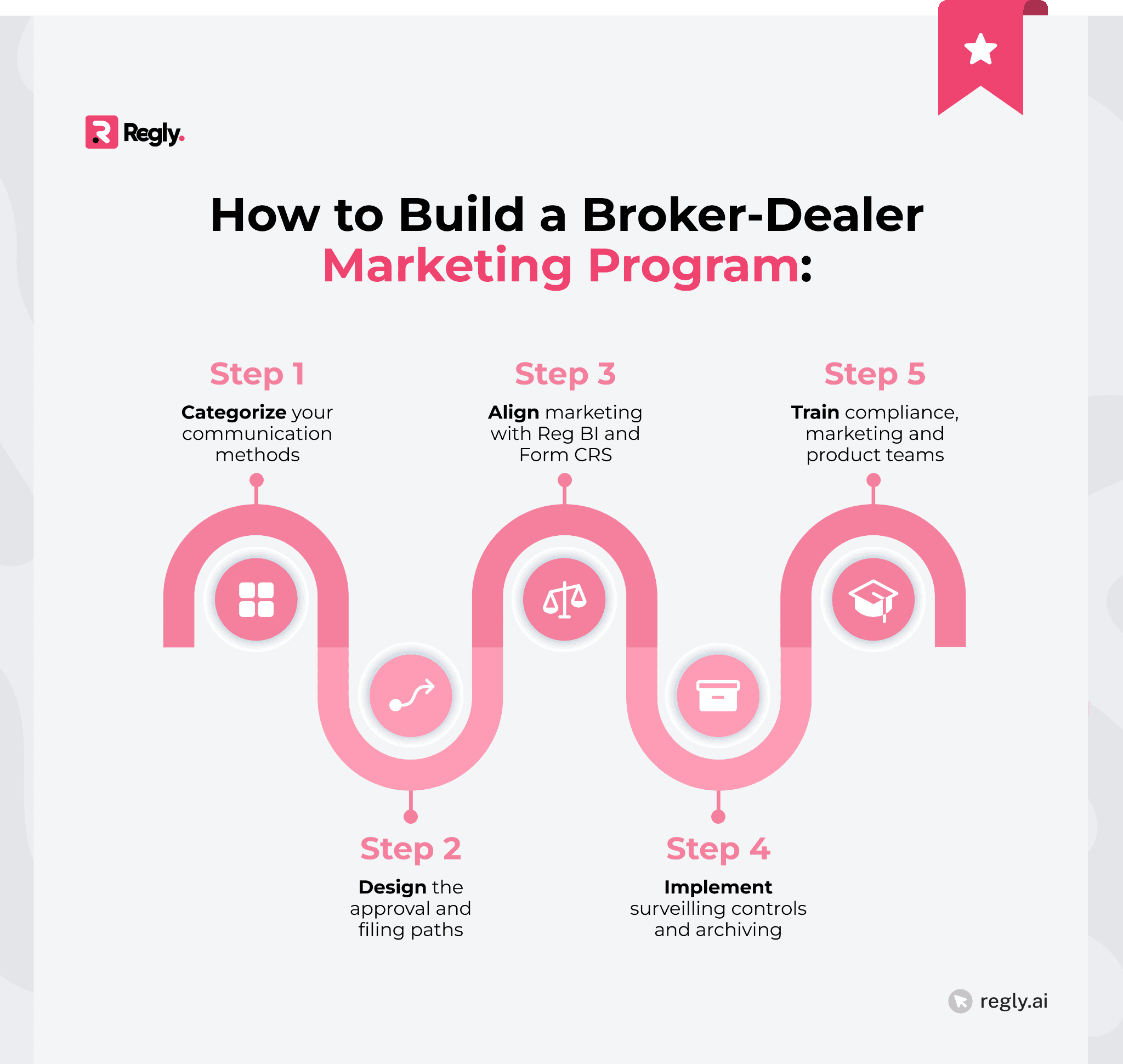

Step 1: Classify Your Communication Types

Start with classification. Every broker-dealer marketing communication should be categorized before release.

At minimum, determine:

Retail communication, correspondence, or institutional communication

Static or interactive content

General promotion or potential recommendation

Product-specific or brand-level messaging

Classification drives approval, filing, and supervisory obligations. Misclassification is a common source of regulatory findings.

For fintech firms operating across web, mobile, and social platforms, classification should be embedded into campaign planning. It should not be an afterthought.

Step 2: Design Approval and Filing Workflows

Once classified, communications should follow a defined approval path. An effective workflow typically includes:

Routing retail communications to a qualified principal

Documenting approval dates and versions

Identifying FINRA filing triggers early

Escalating higher-risk campaigns for additional review

Manual email chains are difficult to track at scale. Structured systems that log versions, approvals, and filing status reduce documentation risk.

For fintech broker-dealers with frequent product updates, aligning approval workflows with release cycles is especially important.

Step 3: Align Marketing With Reg BI and Form CRS

Marketing cannot operate independently from regulatory disclosures. Before launch, review whether the campaign:

Could be interpreted as a recommendation

Involves revenue-generating features with conflicts

Is consistent with Form CRS disclosures

Accurately reflects fee structures and product limitations

If marketing emphasizes certain features, those features should be clearly addressed in formal disclosures. Periodic reconciliation between marketing materials and Form CRS reduces inconsistency risk during examinations.

Step 4: Implement Archiving and Surveillance Controls

All broker-dealer marketing communications must be retained under applicable books and records rules. Controls should address:

Website content and revisions

Social media posts and comments

Influencer communications

In-app messaging

Chatbot interactions

Surveillance should also extend to associated persons and approved third parties.

Fintech firms often operate at a higher communication volume. Automated archiving and centralized monitoring are more reliable than manual collection methods. Platforms like Regly were developed to support this operational reality, helping firms maintain structured records without expanding internal teams.

Step 5: Train Marketing, Product, and Compliance Teams

Policies alone are not sufficient. Teams need a practical understanding of broker-dealer marketing requirements. Training should cover:

Communication classification

Prohibited statements and disclosure standards

Reg BI implications

Escalation protocols

Use of approved templates

Product teams should also understand how interface design can create marketing exposure. Marketing teams should know when content may trigger regulatory review.

An effective broker-dealer marketing program is collaborative. Growth, compliance, and legal functions must operate from the same framework, especially in fintech environments where speed and scale are constant.

Read more about policy management here →

FAQs About Broker-Dealer Marketing

Got some more questions? Keep reading to find answers to common FAQs:

Do All Marketing Materials Require FINRA Filing?

No. Most retail communications require principal pre-approval, but only certain categories require FINRA filing. New member firms must file retail communications during their first year. Other filings depend on product type, content, or specific regulatory triggers under FINRA Rule 2210.

Can Broker-Dealers Use Testimonials?

Yes, but they must comply with FINRA Rule 2210. Testimonials must disclose that they may not be representative and are not guarantees of future performance. If compensation exceeds $100, that compensation must also be clearly disclosed. Broker-dealers follow different testimonial rules than registered investment advisors.

Are Performance Projections Ever Allowed?

Generally, broker-dealers may not project or predict performance in retail communications, subject to limited exceptions such as certain investment analysis tools or research reports. Firms should review current FINRA guidance carefully, as proposals have been discussed, but broad permission for projections is not currently in effect.

How Is Broker-Dealer Marketing Different From RIA Advertising?

Broker-dealer marketing is governed primarily by FINRA Rule 2210 and Exchange Act standards. Registered investment advisors follow the SEC Marketing Rule under the Advisers Act. The two regimes differ in areas such as testimonials, performance advertising, and filing requirements. Firms operating hybrid models must apply the correct ruleset.

What Are the Biggest Red Flags in Regulatory Exams?

Common red flags include misleading performance claims, inadequate risk disclosures, influencer supervision failures, unfiled required communications, and gaps in record retention. Regulators also focus on inconsistencies between marketing statements and Form CRS or internal policies, particularly in digital and mobile distribution models.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.