Onboarding compliance in a fintech is not just an HR checklist. The moment a new employee receives system access, communicates with customers, or participates in product decisions, regulatory exposure begins.

For regulated firms, employee onboarding is a formal compliance control point.

Fintech companies operate at the intersection of new products and established regulatory frameworks. Broker-dealers, RIAs, money transmitters, and crypto firms each face different obligations tied to supervision, licensing, AML, sanctions, data protection, and recordkeeping. How you onboard employees must reflect that regulatory perimeter.

This article breaks down what onboarding compliance actually requires in a regulated fintech. We will clarify the meaning of onboarding compliance, outline obligations by business model, provide a practical checklist covering the first 90 days, and highlight common mistakes that surface in exams and enforcement actions.

What “Onboarding Compliance” Means in a Regulated Fintech

Onboarding compliance refers to the regulatory tasks tied to bringing a new employee into a regulated business. It covers more than offer letters and tax forms. It includes licensing, policy acknowledgments, training, supervision setup, and documentation that regulators may later request.

There is no single onboarding compliance template that fits every fintech. The obligations for a broker-dealer differ from those of a money services business (MSB). An RIA hiring an access person must address reporting and Code of Ethics requirements immediately. The regulatory perimeter drives the process.

Why Onboarding Compliance Is a Control Point

During the onboarding, the permissions are granted, roles are formalized, and obligations are attached to the individual.

If access exceeds guidance, gaps appear. Deadlines can pass unnoticed. Escalations can be delayed. Small oversights early in employment often create larger issues later.

Regulators evaluate whether compliance programs operate effectively. Onboarding is where that operational framework is put in place.

Employee Onboarding vs. Customer Onboarding

In fintech, the word “onboarding” often means customer onboarding, including KYC, identity verification, and AML screening. That is a separate regulatory workflow.

This article focuses on employee onboarding compliance. The risks are different. Instead of verifying customers, you are controlling employee conduct, access to systems, communications, and potential conflicts of interest.

Onboarding Compliance by Fintech Business Model

Onboarding compliance depends on how your fintech is regulated and how the role is classified: a broker-dealer, RIA, and MSB face different obligations.

Broker-Dealers

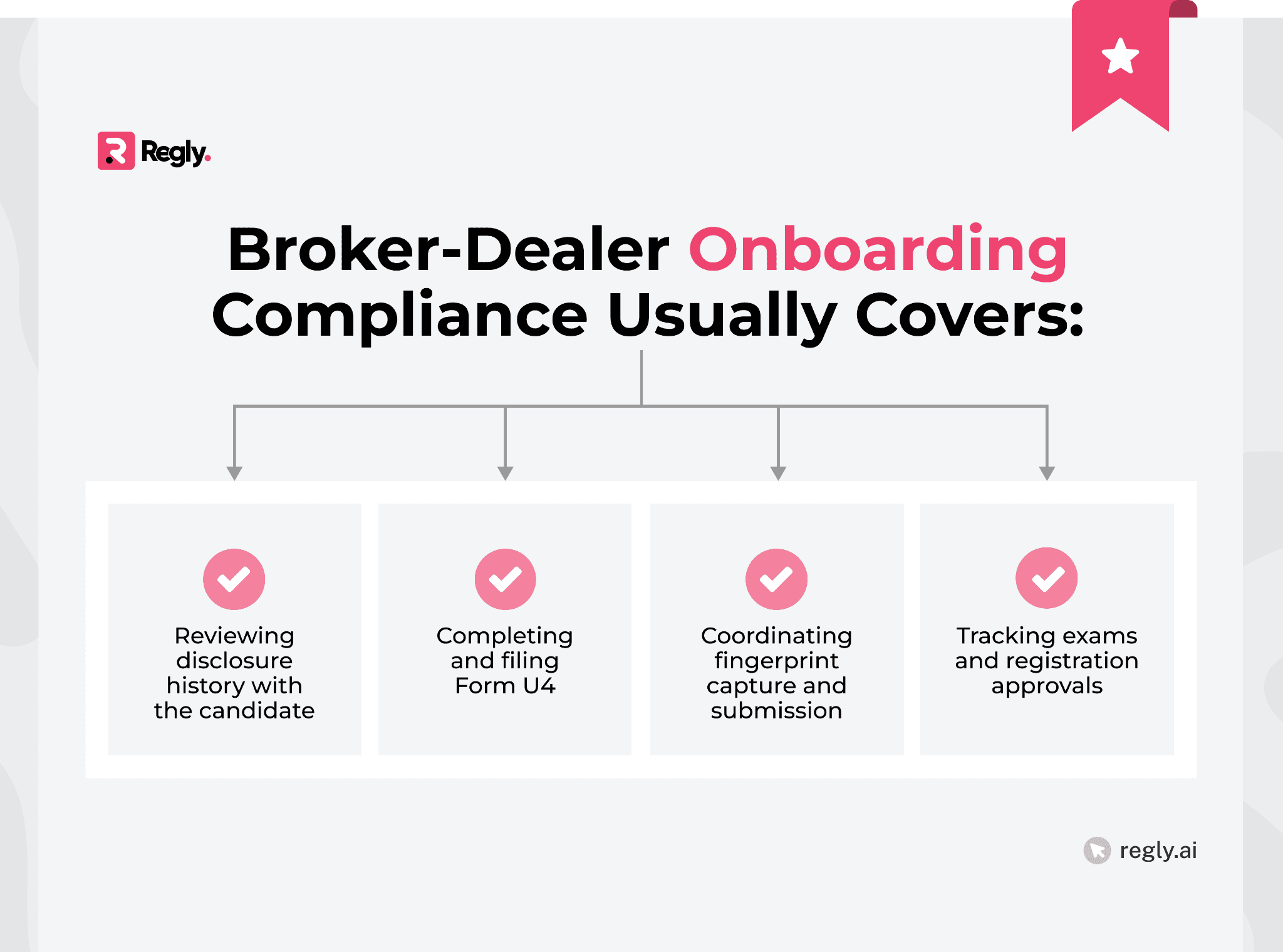

Broker-dealers operate under SEC oversight and FINRA rules. Onboarding compliance in this environment is heavily tied to registration status, supervision, books and records, and continuing education.

The key issue is whether the new hire is an “associated person” and whether they require registration.

See how Regly helps broker-dealers manage advertising reviews, policies, and supervision →

Associated Person status

An associated person includes individuals engaged in the securities business of the firm, including registered representatives and certain supervisors.

As part of onboarding compliance, the firm should assess whether the individual needs to be registered, whether they will participate in securities activity or supervise it, and which qualification exams are required.

If that assessment is incorrect, registration and supervisory gaps often appear later during regulatory reviews.

Form U4 Filing and Fingerprinting

Registration triggers formal filing obligations. The firm must file Form U4 and submit fingerprints within FINRA’s required window.

Incomplete or rushed filings can lead to amendments and regulatory scrutiny.

FINRA Supervision and WSP Alignment

FINRA Rule 3110 requires firms to establish and maintain written supervisory procedures. Onboarding is the point where those procedures are applied to a specific individual.

That means confirming who is responsible for oversight, documenting escalation paths, integrating the employee into monitoring systems, and limiting permissions to what the role requires. Supervision should be set before the first regulated task is performed.

Continuing Education Requirements

FINRA requires registered persons to complete continuing education (CE), including both the Regulatory Element and the Firm Element.

Onboarding compliance should account for when the individual must be enrolled, how deadlines will be tracked, and what role-specific Firm Element content applies. If CE obligations are not built into the onboarding process, lapses can occur later.

See how Regly’s employee compliance helps broker-dealers manage forms, attestations, and outside accounts →

Registered Investment Advisors (RIAs)

RIAs are regulated under the Investment Advisers Act and subject to SEC or state oversight. Onboarding compliance in this model centers on fiduciary duty, conflicts of interest, and personal trading controls.

The central question is not just a job title. It is whether the employee is a supervised person or an access person under Rule 204A-1.

See how Regly helps RIAs centralize compliance oversight and produce evidence →

Supervised Persons vs. Access Persons

A “supervised person” includes employees and others who provide advice on behalf of the firm and are subject to its supervision.

An “access person” is typically someone who:

Has access to nonpublic information about client transactions

Is involved in making securities recommendations

Has access to holdings information of client accounts

During onboarding compliance, you must classify the individual correctly. Access person status triggers additional reporting obligations that begin immediately.

Incorrect classification often leads to missed holdings reports or incomplete transaction monitoring.

Learn more about access persons →

Code of Ethics Distribution and Acknowledgment

RIAs are required to adopt and enforce a written Code of Ethics. Supervised persons must receive a copy and acknowledge it in writing.

Onboarding compliance should include:

Delivering the current Code of Ethics

Collecting a written acknowledgment of receipt

Documenting the acknowledgment in a retrievable system

A firm’s Code of Ethics is frequently one of the first documents requested in an SEC exam.

See how Regly helps RIAs manage policy distribution and attestations →

Initial Holdings and Transaction Reporting Timelines

Once an individual qualifies as an access person, initial holdings information must be submitted within the required window, and after that, transaction reporting typically continues on a quarterly cycle.

As part of onboarding compliance, firms should determine which accounts and securities are reportable, explain the applicable deadlines, monitor submissions, and follow up on missing or incomplete reports. When this process is delayed, gaps tend to surface quickly.

Personal Trading Pre-Clearance Requirements

Pre-clearance obligations are standard in many RIA compliance programs. IPOs and private placements usually require prior notice and approval, and some firms broaden the rule.

During onboarding, the employee should be shown how trade approval requests are made and how their personal accounts are incorporated into ongoing monitoring.

Personal trading rules apply as soon as the individual is designated as an access person. Clear records at onboarding reduce future disputes.

Compliance Area | What Onboarding Should Address |

|---|---|

Supervised Persons vs. Access Persons | Determine whether the employee is a supervised person or qualifies as an access person based on their role and access to client information or trading activity. Access person status triggers additional reporting obligations, so misclassification can lead to missed holdings reports or monitoring gaps. |

Code of Ethics Distribution and Acknowledgment | Provide the firm’s Code of Ethics, collect written acknowledgment of receipt, and retain the record in a retrievable system. This documentation is commonly requested during SEC examinations. |

Initial Holdings and Transaction Reporting | Identify reportable accounts and securities, explain reporting deadlines, monitor submissions, and follow up on missing reports. Access persons must submit an initial holdings report and ongoing transaction reports. |

Personal Trading Pre-Clearance | Explain when pre-clearance is required (such as IPOs or private placements), demonstrate how approval requests are submitted, and link personal accounts to the firm’s monitoring process. Personal trading rules apply immediately once the access person's status begins. |

Money Transmitters, MSBs, and Crypto Firms

Money services businesses, including many crypto firms and payment platforms, are governed by the Bank Secrecy Act and related AML rules.

As such, onboarding compliance should include:

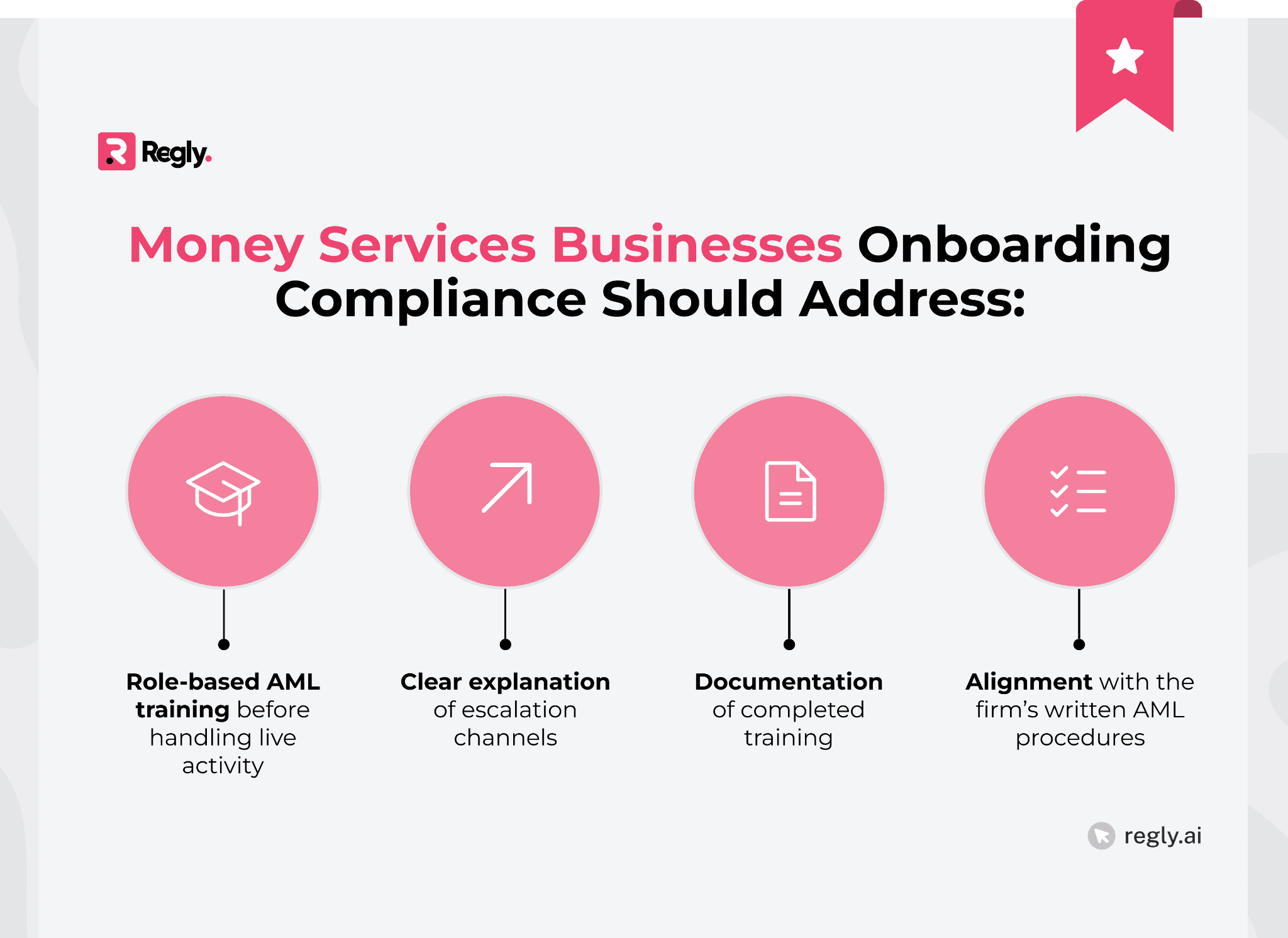

AML Program Pillars and Employee Training

MSBs are required to maintain an AML program that includes internal controls, a designated compliance officer, independent testing, and training for appropriate personnel.

Training should reflect how risk appears in your specific product, whether that involves prepaid cards, cross-border transfers, or digital assets.

See how Regly helps fintechs manage AML oversight and screening workflows →

Suspicious Activity Monitoring Responsibilities

In many fintech organizations, suspicious activity is first identified outside the compliance function. Operations analysts reviewing transactions, support teams handling customer issues, or product staff monitoring user behavior may see irregular patterns before anyone else.

If those employees are not trained to recognize red flags, monitoring systems lose effectiveness. Technology can generate alerts, but human judgment still determines whether activity is escalated appropriately.

Onboarding should make the escalation framework clear. Employees need to know which types of activity must be reported, how internal reviews are recorded, and who ultimately decides whether a Suspicious Activity Report (SAR) is filed. They should also understand that SAR-related information is highly restricted and cannot be discussed freely.

Addressing these expectations early changes how monitoring works in practice. Suspicious activity detection becomes part of normal operations rather than something handled only by compliance. During exams, regulators often focus on whether this kind of operational awareness actually exists.

Sanctions Awareness Under the OFAC Framework

Sanctions rules under US law apply broadly across payment and transaction activity. Anyone involved in customer onboarding, payment handling, or transaction processing needs a working understanding of those restrictions.

Onboarding compliance should introduce the basic structure of sanctions programs, explain how screening tools are used, and outline the steps employees must follow when a name or transaction generates a potential match.

Employees should also understand that screening systems have limitations and that escalation procedures exist for a reason. Decisions about possible matches should move through defined compliance channels.

Many sanctions issues arise when operational staff try to resolve alerts informally or bypass established processes. Early training helps prevent those situations.

See how Regly supports fintech AML and sanctions workflows →

—

Compliance Area | What Onboarding Should Address | Why It Matters |

|---|---|---|

AML Program and Employee Training | Introduce the AML program structure, covering internal controls, compliance oversight, and role-based training before employees access live systems. Escalation paths and training completion should be recorded. | Training should reflect how financial crime risk appears in the firm’s products, such as payments, cross-border transfers, or digital assets. |

Suspicious Activity Monitoring | Explain escalation triggers, internal investigation documentation, SAR decision authority, and confidentiality rules on SAR information. | Frontline teams often identify unusual activity before compliance. Clear guidance helps maintain effective monitoring. |

Sanctions Awareness | Introduce sanctions restrictions, screening system use and limitations, and define escalation procedures for potential matches. | Sanctions failures often result from operational shortcuts or unclear procedures. Early training helps prevent bypassing screening controls. |

The Core Employee Onboarding Checklist for Compliance

Dividing the onboarding process into stages reduces oversight gaps and produces a more reliable audit trail:

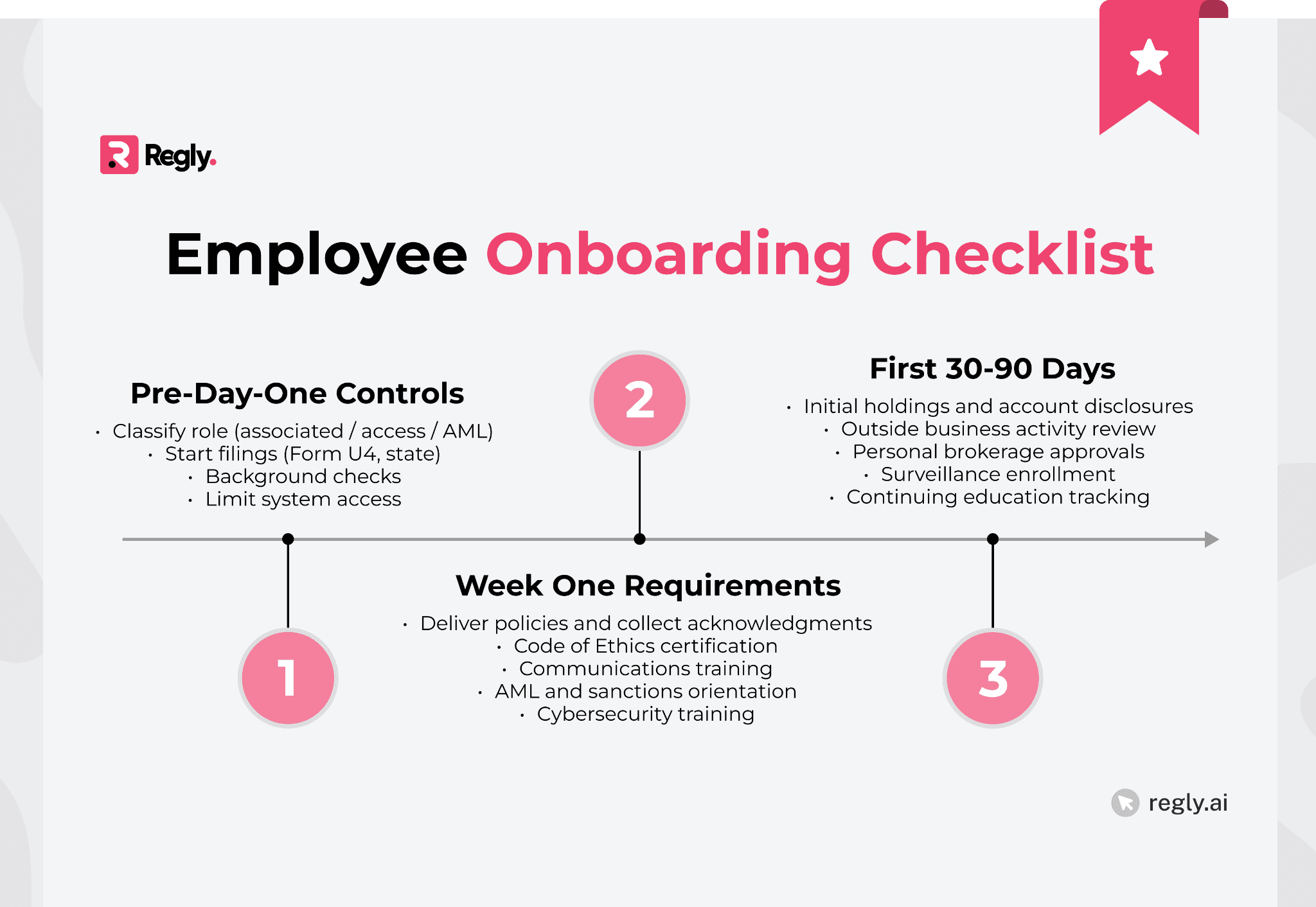

1. Pre-Day-One Controls

Before granting access to live systems, confirm the regulatory classification of the role and map the associated obligations.

Core pre-start onboarding compliance tasks often include:

Role classification and regulatory mapping: Determine whether the employee is an associated person, supervised person, access person, or AML-relevant personnel.

Licensing and registration filings: Submit required filings, such as Form U4 and state registration forms.

Background checks and eligibility screening: Check for disciplinary records, statutory disqualifications, and other reportable matters.

Access scoping and system permissions: Limit system access to job-relevant functions. Avoid broad administrative rights without documented justification.

Each of these actions needs to be supported by clear documentation. During regulatory reviews, firms are often asked to produce records showing when access was approved and how the employee’s role was mapped to regulatory requirements.

See how Regly helps companies centralize documentation and prepare for regulatory examination →

2. Week One Requirements

The first week establishes the baseline for compliance expectations. Policies should move beyond written documents and become acknowledged responsibilities.

Typical onboarding compliance items include:

Policy distribution and documented acknowledgments: Deliver core policies such as Code of Ethics, communications policies, AML procedures, and cybersecurity standards.

Code of Ethics certifications: New hires should confirm in writing that they have received and reviewed the firm’s Code of Ethics. The certification process should also clarify their reporting responsibilities under the policy.

Communications policy training: Clarify approved channels, record retention expectations, and off-channel restrictions.

AML and sanctions orientation: Provide training that reflects the employee’s role within the firm to enable them to understand how your AML programs work in practice and relate to their specific role.

Cybersecurity and incident reporting training: Explain data handling standards, phishing reporting, and escalation protocols.

Week one is about clarity. Employees should understand what is required, how to comply, and where to escalate issues.

3. First 30-90 Days

Some onboarding compliance obligations extend beyond the first week. These are often the items that get missed.

Key items during this window may include:

Access person reporting deadlines: Initial holdings reports and brokerage account disclosures.

Outside business activity disclosures: Collection and review of outside roles, advisory positions, or side ventures.

Personal brokerage account approvals: Linking accounts for duplicate confirmations or monitoring.

Surveillance enrollment and supervision review: Confirm inclusion in trade surveillance, communications review, or AML monitoring workflows.

Continuing education enrollment: Register for required CE programs and track deadlines.

A structured 90-day onboarding compliance timeline reduces reliance on memory and informal follow-ups. It also creates defensible documentation if questions arise later.

For growing fintech teams, centralizing these tasks in a single workflow platform can simplify tracking and reporting without adding headcount. That’s why we have developed our platform based on InnReg’s experience of working with 100+ fintechs.

See how Regly helps fintechs →

Communications, Recordkeeping, and Off-Channel Risk

Communication risk starts immediately. New hires join messaging platforms, email threads, and collaboration tools before they fully understand recordkeeping rules. Onboarding compliance must address approved tools, retention obligations, and restrictions on personal devices.

Approved Communication Tools

Employees need clarity on which communication tools are permitted for business activity and which are prohibited.

Onboarding compliance should spell out approved email domains and collaboration platforms, set boundaries around texting and messaging apps such as WhatsApp or Signal, and define how social media may be used in a professional capacity.

It should also explain what process applies if a team wants to introduce a new tool. When expectations are vague, employees tend to use whatever is most convenient.

Books and Records Requirements

Most regulated fintechs are subject to formal record retention rules. Communications relating to business activity may need to be retained for specific periods.

During onboarding compliance, employees should understand:

What qualifies as a business communication

How messages are archived

Why deleting messages can create regulatory exposure

The role of supervisors in reviewing communications

Examiners frequently request message samples tied to specific employees or time periods.

Personal Device and Messaging App Restrictions

Recent enforcement actions across the financial industry have focused on off-channel communications. Regulators have imposed significant penalties on firms that failed to capture business discussions conducted on personal devices.

Onboarding compliance should address:

Whether personal devices may be used for business

Conditions for approved use, if permitted

Prohibitions on unmonitored messaging apps

Attestation requirements regarding off-channel communications

Clear boundaries at the start of employment reduce the likelihood of later remediation efforts.

Communication oversight is not just a broker-dealer issue. RIAs and fintech payment firms face similar scrutiny when records are incomplete or supervision is weak.

Conflicts of Interest and Outside Activities

Conflicts of interest rarely begin with bad intent. They begin with incomplete disclosure. Onboarding compliance is the point where firms collect the information needed to identify outside roles, financial interests, and relationships that could influence business decisions.

Outside Business Activity Disclosures

Many firms require employees to disclose outside business activities at hire. This can include board positions, consulting arrangements, advisory roles, or side ventures.

Onboarding compliance should require:

A written disclosure of all outside roles

Review by compliance or supervisory personnel

Documentation of approval, denial, or conditions

Ongoing update requirements if circumstances change

Failure to collect this information at onboarding often leads to retroactive reviews after issues surface.

Learn more about outside business activities →

Private Securities Transaction Rules

Under FINRA rules, broker-dealers are required to oversee employee involvement in private securities transactions. In many cases, employees must notify the firm in advance and receive approval before participating in certain offerings.

Onboarding compliance should explain how these transactions are identified and what disclosure steps employees must follow. The firm’s review process and related documentation expectations should also be addressed early. Employees often underestimate how broadly these requirements apply, particularly in environments where startup investments are common.

Personal Trading and Brokerage Account Monitoring

Personal trading creates conflict risk across broker-dealers and RIAs. Monitoring depends on the timely disclosure of brokerage accounts and reportable transactions.

During onboarding compliance, firms should:

Collect brokerage account information

Determine whether duplicate confirmations are required

Link accounts to monitoring workflows

Communicate reporting deadlines clearly

If accounts are disclosed late, monitoring gaps follow.

Learn more about outside brokerage accounts monitoring →

Conflict Inventory Updates During Onboarding

Onboarding compliance is also an opportunity to update the firm’s broader conflict inventory. A new employee may introduce new relationships, affiliations, or revenue streams that were not previously considered.

Compliance teams should assess whether:

The employee’s prior affiliations create disclosure obligations

New compensation structures create incentives that require review

Client disclosures or Form ADV updates are implicated

Conflict management is not static. Each new hire can change the firm’s risk profile.

Common Onboarding Compliance Mistakes in Fintech

Most onboarding compliance failures are not dramatic. They are procedural gaps that accumulate over time. Examiners tend to find patterns, not isolated oversights.

Below are recurring issues we see across broker-dealers, RIAs, and fintech payment firms:

Treating Onboarding as HR-Only: Compliance is sometimes informed after access has already been granted. By that point, system permissions, client communications, and workflow participation may already be active. Onboarding compliance should be coordinated between HR, legal, IT, and compliance. If these functions operate in silos, documentation gaps follow.

Confusing Employee Onboarding with Customer Onboarding: Fintech teams are often strong on customer KYC and AML. Employee onboarding compliance receives less attention. The two processes serve different regulatory objectives. Customer onboarding manages financial crime risk. Employee onboarding manages supervision, conduct, conflicts, and recordkeeping risk. Treating them as interchangeable creates blind spots.

Failing to Align Policies with Actual Systems: Some firms maintain written communications policies that do not reflect how employees actually work. New hires may be placed on collaboration platforms that are not captured by the firm’s monitoring processes. Onboarding compliance should reconcile policy language with the systems used in practice, particularly when tools such as Slack, WhatsApp, or internal workflow platforms are involved.

Ignoring Contractors and Part-Time Staff: Advisors and contractors are common in fintech teams. Depending on their responsibilities, they may still fall under regulatory roles such as associated persons or supervised persons. What matters in onboarding compliance is the activity they perform, not their contract status.

Missing Regulatory Classification at Hire: Many compliance gaps start with role classification. A developer with access to trading systems may create supervisory implications. An operations employee may qualify as an access person. Without clear regulatory mapping at onboarding, filings, and disclosures can be missed.

—

Each new hire introduces new authority, new system access, and potentially new conflicts. Treating onboarding as a coordinated compliance process rather than an HR task creates stronger supervision and clearer accountability.

For firms building at scale, documenting onboarding compliance in a structured, repeatable way provides clarity for management and credibility during regulatory exams.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.