The EU AI Act Article 14 centers on a simple but important idea: AI systems can’t operate without human oversight. If your company relies on high-risk AI, you need clear ways for people to understand what the system is doing and step in when needed.

This is especially relevant for fintech. AI already plays a role in credit decisions, fraud monitoring, transaction screening, and trading. Article 14 doesn’t restrict these use cases, but it does make it clear that firms remain responsible for the outcomes and can’t rely on automation alone.

This guide walks through what Article 14 actually requires, how human oversight works in practice, and what fintech teams should be doing about it now.

Overview of the EU AI Act and Why Human Oversight Matters

The EU AI Act is a risk-based regulation that classifies AI systems based on how much potential harm they can cause. High-risk systems, which are common in financial services, face the most detailed obligations around governance, documentation, and control.

Human oversight sits at the center of this framework. Regulators aren’t trying to stop companies from using AI. They’re addressing a different concern. AI systems can produce outcomes that are hard to interpret, difficult to challenge, or inconsistent over time.

Without human involvement, those issues can go unnoticed until they create real regulatory or customer impact.

Article 14 is the provision that translates this concern into operational requirements. It requires firms to design systems in a way that allows people to:

Monitor outputs

Question decisions

Step in when something doesn’t look right

For fintech teams, this often means going back and looking at how AI actually fits into the compliance work already in place. Oversight can't sit in a policy document and call it done. It has to be built into the systems, the workflows, and what people are doing every day.

What Does Article 14 of the EU AI Act Require?

Article 14 focuses on one key idea: human oversight. If your firm uses high-risk AI, you need clear ways for people to monitor decisions and step in when needed.

The Purpose of Human Oversight

Human oversight is about keeping control over how AI systems behave, especially when decisions can affect:

Customers

Markets

Regulatory outcomes

While AI can process large amounts of data and spot patterns quickly, it doesn’t understand context the way people do. That gap is where oversight becomes important.

Regulators are focused on reducing risks that come from overreliance on automation. This includes situations where:

Decisions can’t be easily explained

Errors go unnoticed

Systems behave differently over time

Without human involvement, these issues can go unnoticed until they create real risk.

Article 14 addresses this by requiring firms to stay actively involved in how AI is used. That means reviewing outputs when needed, questioning results that don’t make sense, and having the ability to step in before a decision causes harm.

The goal is to create a layer of control that matches the level of risk. For fintech teams, that often means focusing human attention where it matters most instead of trying to review everything.

Which AI Systems Must Comply With Article 14

Article 14 applies to high-risk AI systems under the EU AI Act. These are systems that can have a significant impact on:

People’s rights

Financial outcomes

Access to services

The regulation defines these categories clearly, and many common fintech use cases fall within them.

In financial services, this often includes AI used in:

Credit scoring

Lending decisions

Fraud detection

If a system influences whether someone gets access to a financial product or how they’re treated from a compliance perspective, there’s a strong chance it will be classified as high risk.

It’s important to note that not all AI systems are covered. Lower-risk tools, such as basic automation or internal productivity systems, may not trigger the same requirements. The focus is on systems where decisions carry real consequences.

Where Article 14 Fits in the EU AI Act Framework

Article 14 doesn’t stand alone. It works alongside rules on:

Risk management

Data governance

Transparency

Accuracy

Documentation.

Human oversight ends up tied to a bunch of other obligations, whether you want it to be or not. You can't really monitor a system if you don't have a view into how it was trained or how it's holding up over time. And you can't step in when you need to if there's no clear record of what the system has been doing or what decisions came out of it.

Article 14 focuses on the human role within this larger framework. It defines how people stay involved in systems that are otherwise automated. Other provisions define what needs to be built around that, such as controls, testing, and recordkeeping.

For fintech teams, it helps to think of Article 14 as the operational layer. It’s where regulatory expectations meet real workflows. If the surrounding framework is in place, oversight becomes easier to implement and maintain.

Key Human Oversight Requirements Under the EU AI Act

Article 14 sets out clear requirements for human oversight. These focus on giving people visibility into AI systems, control over outcomes, and the ability to step in when needed.

1. Designing AI Systems for Human Oversight

Human oversight starts with how the system is built. If oversight isn’t considered during design, it becomes much harder to add later. Teams need to think early about:

How decisions will be reviewed

What information will be available

How users will interact with the system

This often comes down to visibility. People should be able to see how the system reached a decision, what data was used, and how confident the output is. If outputs appear as black boxes, oversight becomes limited and reactive.

It also requires clear control points. Systems should allow users to pause, flag, or override decisions when something doesn’t look right. Without these controls, oversight exists in theory but not in day-to-day use.

For fintech companies, this usually means working closely across product, engineering, and compliance teams.

2. Preventing or Minimizing AI Risks

Human oversight is closely tied to risk reduction. The goal is to catch issues early, before they lead to incorrect decisions or regulatory exposure. This starts with understanding where the system can fail and what the impact would be.

Some risks come from data quality, model drift, or unexpected patterns in new inputs. Others come from how outputs are used in decision-making. Without oversight, these risks can build over time without clear signals.

To address this, firms need defined checkpoints where outputs are reviewed or flagged. This doesn’t mean reviewing everything. It means focusing attention on higher-risk scenarios, unusual results, or edge cases.

Oversight also needs feedback loops to work. When something gets caught, there has to be a way to feed that back into the system or change how it's being used. That's what keeps the same errors from happening again and keeps the system behaving the way it's supposed to.

3. The Ability to Intervene or Override AI Decisions

Human oversight only works if people can act on what they see. If a system produces a questionable result, there needs to be a clear way to step in, stop the process, or change the outcome.

This requires defined intervention points. For example, a flagged transaction might be held for review, or a credit decision might be paused before it’s finalized. These controls need to be easy to access and built into normal workflows.

It’s also important to define when intervention is expected. Teams should know what types of outputs require review and what thresholds trigger action. Without this clarity, decisions may still pass through without proper checks.

Overrides need to be logged and traceable. When someone changes a decision or blocks it from going forward, there has to be a record of what they did and the reason behind it. That trail holds up in internal reviews and lines up with what regulators expect when it comes to showing accountability.

4. Monitoring System Performance and Behavior

Oversight doesn’t stop after a system is deployed. AI systems can change over time as data shifts or usage evolves. Without ongoing monitoring, small issues can turn into larger problems.

Teams need visibility into how the system performs on a continuous basis. This includes tracking:

Accuracy

Consistency

Any unusual patterns in outputs

Sudden changes or unexpected results should be easy to detect and review.

Monitoring also helps identify drift. A model that worked well at launch may behave differently months later. Regular checks make it easier to spot these changes early and take corrective action.

For fintech companies, this often ties into existing risk and compliance processes. Monitoring AI systems shouldn’t sit in isolation. It should connect with broader controls that track operational and regulatory risk.

5. Verifying Oversight Personnel Have the Right Competence

Human oversight depends on the people involved. If teams don’t understand how the system works or what to look for, oversight becomes limited.

Staff responsible for reviewing AI outputs should have enough context to interpret results and question them when needed. This doesn’t mean everyone needs to be a data scientist. It means they should understand the system’s purpose, its limitations, and where it can go wrong.

Employee training plays a key role here. Teams need guidance on how to handle flagged cases, when to escalate issues, and how to use override controls. Without this, decisions may still rely too heavily on automated outputs.

Clear roles and responsibilities also matter. Everyone involved should know what they’re accountable for and how their actions fit into the broader control framework.

How Does Human Oversight Work in Practice?

Human oversight can take different forms depending on how the AI system is used and the level of risk involved. The EU AI Act recognizes this and allows for flexibility in how oversight is applied.

Human-in-the-Loop Oversight

Human-in-the-loop oversight means a person is directly involved in the decision-making process. The AI system may generate a recommendation, but a human reviews it before any final action is taken.

This model is common in higher-risk scenarios where decisions have a clear impact on customers. For example, a flagged transaction or a credit decision might require manual approval before it moves forward.

It gives the highest level of control, but it also requires more time and resources. Teams need to balance this approach with operational efficiency, especially when dealing with large volumes of decisions.

Human-on-the-Loop Oversight

Human-on-the-loop oversight means the system runs on its own, but people monitor its behavior and step in when something looks off. The focus is on supervision rather than reviewing every decision.

This approach is often used when decisions happen at scale. For example, fraud monitoring systems may process large volumes of transactions, while analysts focus on alerts, trends, or unusual patterns.

It relies on strong monitoring and clear escalation paths. If something crosses a threshold or raises concern, there should be a clear way for teams to investigate and take action.

Human-in-Command Oversight

Human-in-command oversight focuses on overall control rather than individual decisions. People don’t review each output or monitor every action, but they remain responsible for how the system is set up, used, and governed.

This includes:

setting policies

defining thresholds

deciding when a system should be updated, paused, or taken offline

It also involves reviewing performance over time and making adjustments when needed.

This model is often used for systems that operate continuously, where direct involvement in each decision isn’t practical. Even so, accountability stays with the firm, and teams need to stay engaged with how the system behaves.

When Each Oversight Model Is Used

Each oversight model serves a different purpose. The right choice depends on how the AI system is used and the level of risk tied to its decisions.

Human-in-the-loop is typically used for high-impact decisions where a review step is needed before any action is taken. This is common in areas like credit approvals or account restrictions.

Human-on-the-loop works better for systems that handle large volumes. Teams monitor outputs, review alerts, and step in when something looks unusual. This approach is often used in fraud detection and transaction monitoring.

Human-in-command applies at the governance level. It’s used for setting rules, reviewing performance, and deciding when systems need changes. Most fintech companies use a mix of all three, depending on the use case.

Model | How It Works | Typical Use Case |

|---|---|---|

Human-in-the-Loop | Humans review each decision before taking action | Credit approvals, account restrictions |

Human-on-the-Loop | The system runs independently with human monitoring | Fraud detection, AML monitoring |

Human-in-Command | Human oversees system design and performance | Trading systems, portfolio management |

EU AI Act Human Oversight Requirements for Fintech and Financial Institutions

Human oversight looks different depending on the use case. In financial services, the focus is on how AI affects decisions that carry regulatory and customer impact.

1. AI in Credit Scoring and Lending Decisions

AI gets used heavily in credit scoring and lending to size up risk and move decisions faster. These systems can chew through a lot of data, but the outputs still need to make sense to someone, and they need to be reviewable when the situation calls for it.

Human oversight is especially important when decisions affect someone’s access to financial products. If an application is declined or marked as higher risk, there should be a clear way for a person to review that outcome and challenge it when appropriate.

Teams also need visibility into how decisions are made. If a model relies on certain variables or patterns, reviewers should be able to interpret those signals and spot potential issues, such as bias or inconsistent results.

This is an area where oversight often combines different models. Some decisions may go through automated flows, while others are routed for manual review based on risk level or predefined triggers.

2. AI in AML and Fraud Monitoring

AI shows up all over AML and fraud monitoring, helping teams spot suspicious activity and flag patterns that don't look right. These systems make it possible to handle huge transaction volumes, but they also generate plenty of false positives and can miss risks that are still taking shape.

Human oversight is critical when alerts are triggered. Analysts need to review flagged activity, decide whether it requires escalation, and determine the appropriate next step. The system may surface the signal, but the decision still sits with the team.

Oversight also helps refine how the system performs over time. If certain alerts are consistently low value or if patterns are being missed, teams need a way to adjust thresholds or retrain models.

For fintech companies, this often means combining automated detection with structured review processes. The goal is to manage scale without losing control over how decisions are made.

3. AI in Customer Risk Profiling and Compliance Monitoring

AI is often used to assess customer risk and support ongoing compliance monitoring. These systems can:

Group customers by risk level

Flag changes in behavior

Support decisions around onboarding or account reviews

Human oversight is important when these classifications affect how customers are treated. If a customer is labeled high risk, there should be a way to review that outcome and understand what drove it.

Teams also need to monitor how these profiles change over time. A shift in behavior or data inputs can lead to different risk scores, and those changes should be visible and explainable.

Oversight helps keep these systems aligned with regulatory expectations. It also reduces the chance of relying on outdated or misleading signals when making compliance decisions.

4. AI in Trading, Portfolio Management, and Market Surveillance

AI is used in trading and portfolio management to:

Analyze market data

Execute strategies

Detect unusual activity

These systems can react quickly, but that speed also increases the need for control.

Human oversight focuses on setting boundaries and monitoring outcomes. Teams need to define trading limits, risk thresholds, and conditions where activity should be paused or reviewed.

Market surveillance systems also rely on oversight to investigate alerts. If the system flags potential manipulation or abnormal behavior, someone needs to assess whether it reflects real risk or a false signal.

These environments often combine automation with supervisory controls. The system handles execution or detection, while teams stay responsible for how it operates and how issues are addressed.

Common Compliance Challenges With Article 14

Implementing human oversight sounds straightforward, but teams often run into practical challenges once systems are live. Most issues come from how AI is designed, used, and integrated into existing workflows.

Overreliance on Automated Decisions: When systems perform well, teams may stop questioning outputs. For example, a credit model might consistently approve or decline applications without review, even when edge cases appear. Over time, this can lead to decisions being accepted without scrutiny, especially in high-volume environments.

Defining Meaningful Human Intervention: It’s not enough to say a human is “in the loop.” Teams need to define what actions are expected. Should a reviewer validate inputs, challenge the output, or just approve it? Without clear expectations, reviews can become a formality rather than an actual control.

Lack of AI Transparency and Explainability: If a system produces a risk score or decision without showing the key drivers behind it, reviewers are left guessing. That makes it harder to justify decisions internally or answer regulatory questions, especially when the outcome affects a customer directly.

Skills Gaps in Oversight Personnel: Working with external models or APIs usually means working with thin documentation and not much insight into the outputs. When something breaks, it's not always clear how the model got to its answer or what levers exist to change it. That leaves a gap in control, even though accountability still rests with the firm using it.

Oversight Across Third-Party AI Vendors: Working with external models or APIs usually means working with thin documentation and not much insight into the outputs. When something breaks, it's not always clear how the model got to its answer or what levers exist to change it. That leaves a gap in control, even though accountability still rests with the firm using it.

Common Misconceptions About Human Oversight in the EU AI Act

Human oversight is often misunderstood, especially when teams first read Article 14. Some assumptions can lead to unnecessary complexity or missed requirements.

Human Oversight Does Not Mean Manual Review of Every Decision

Human oversight doesn't mean a person has to sign off on every single decision. That falls apart fast, especially with systems handling huge volumes of data. Instead, oversight is about focusing attention where it matters. Teams can rely on thresholds, alerts, or risk-based triggers to decide when a review is needed. For example, only higher-risk transactions or unusual outcomes may be flagged for human review.

The point is to stay in control without grinding operations to a halt. Systems keep running on their own, but there's always a clear way to bring a result in for a closer look when it lands outside what teams would normally expect to see.

Automation Is Not Prohibited Under the EU AI Act

The EU AI Act doesn’t restrict the use of automation. Firms can continue using AI to support decisions, improve efficiency, and handle large volumes of data.

What changes is how that automation is controlled. Systems can’t run without visibility or accountability. There needs to be a way to understand outputs, question results, and step in when something doesn’t look right.

This means firms don’t need to scale back their use of AI. They need to build the right controls around it so automation works within a defined framework.

Oversight Must Be Built Into System Design

Human oversight can’t be added at the end as a separate control. If it isn’t part of how the system is designed, it often becomes difficult to apply in a meaningful way.

Teams need to think about oversight early. This includes:

How decisions are displayed

What information is available to reviewers

How users can take action when something looks off

If these elements aren’t built in, oversight tends to rely on workarounds. That can lead to gaps, delays, or inconsistent reviews. Designing for oversight from the start makes it easier to keep control as systems scale.

Responsibility Cannot Be Fully Outsourced to Vendors

Using third-party AI providers doesn’t remove responsibility. Even if a system is developed or hosted by a vendor, the firm using it is still accountable for how it performs and how decisions are made.

That creates a real problem when visibility is thin. Vendors often hand over outputs without showing much of what's happening behind the model or how a decision came together. When you can't see in, reviewing results or stepping in to fix something gets a lot harder.

Firms need to put controls in place when working with vendors. This can include clear documentation, defined escalation paths, and the ability to monitor outputs over time. Vendor relationships should support oversight, not limit it.

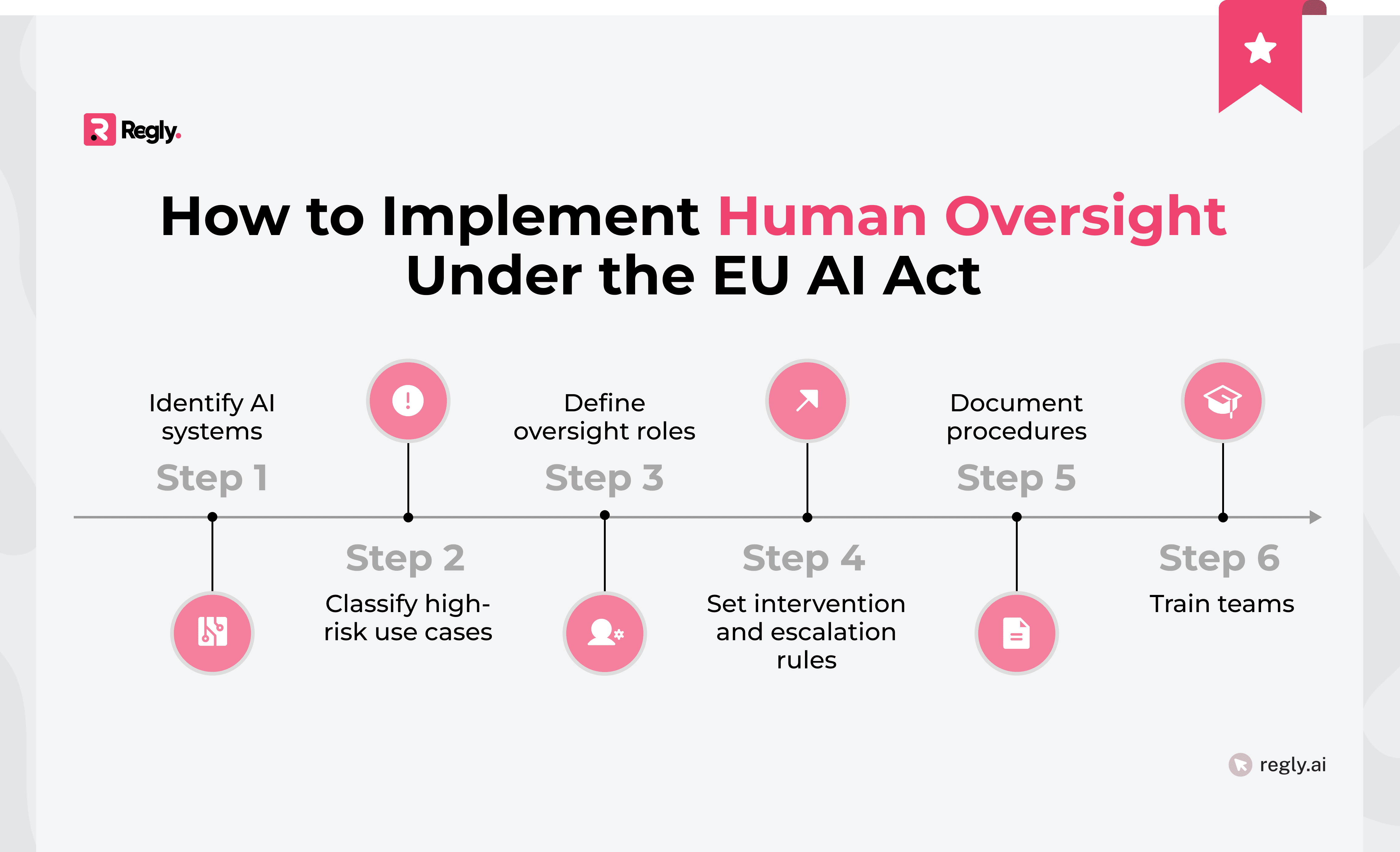

How to Implement Human Oversight Under the EU AI Act

Turning Article 14 into something actionable requires more than policy language. Teams need to translate these requirements into clear roles, workflows, and system controls.

Step 1: Identify High-Risk AI Systems

The first step is to understand which AI systems fall under the EU AI Act’s high-risk category. Not every system will be in scope, so it’s important to focus on those that:

Affect customer outcomes

Financial decisions

Regulatory obligations

Start by mapping where AI is used across the business. This includes areas like credit decisions, fraud monitoring, customer risk scoring, and trading systems. Once identified, assess whether these use cases meet the criteria for high-risk classification under the regulation.

This step sets the foundation for everything that follows. If a system is classified as high risk, it will trigger requirements around oversight, documentation, and control.

Step 2: Define Oversight Roles and Responsibilities

Once high-risk systems are identified, the next step is to assign clear ownership. Human oversight only works if people know what they’re responsible for and when they need to act.

This usually involves multiple teams. Compliance may define requirements, product and engineering may control system behavior, and operations teams may handle day-to-day reviews. Each group should have a defined role tied to how the system is used.

It’s also important to define decision points:

Who reviews flagged outputs?

Who can override a decision?

Who escalates issues?

Without clear answers, oversight can become inconsistent or delayed.

Step 3: Build Intervention and Escalation Mechanisms

Once roles are sorted, teams need a real way to act when something looks off. If a system kicks out a questionable result, there has to be a clear path to review it, escalate it, and respond.

That starts with knowing what counts as a trigger. Certain outputs, thresholds, or patterns should automatically pull a result in for review. A high-risk transaction or an unusual model output, for instance, might get routed straight to someone for a closer look. Escalation paths should be easy to follow. Teams need to know when an issue can stay with operations and when it should move to compliance, risk, or senior management. Without that structure, issues can linger, be handled inconsistently, or fall through the cracks.

Intervention also needs to be simple to carry out. Whether the right step is pausing a process, overriding a decision, or flagging a case for review, teams should be able to take action inside the workflows they already use.

Step 4: Document Oversight Procedures

Oversight needs to be clearly documented so teams know how to act and regulators can understand how controls work. This includes outlining:

When reviews happen

What actions are expected

How decisions are recorded

Documentation should reflect how things actually work, not just policy intent. If teams follow specific workflows or use certain tools, those details should be captured. This makes it easier to apply oversight consistently across the organization.

Exceptions and edge cases need the same treatment. When a system behaves differently under certain conditions, teams should know exactly how to handle it and who to bring in.

Good documentation pulls teams onto the same page and stands up when auditors or regulators come asking. It shows oversight isn't being made up as you go, but follows a process people can actually point to.

Keeping documentation consistent can be difficult, especially as systems and workflows evolve. Tools like Regly’s policy management platform help teams centralize procedures, track updates, and maintain clear records so oversight stays structured and easy to review.

Step 5: Train Oversight Personnel

Oversight comes down to how well teams actually understand the systems they're working with. If people don't know what to watch for or how to react, the controls won't do what they're supposed to. Training needs to cover:

How the system behaves

What the outputs mean

Where issues are likely to appear

Teams also need to know when to push back on a result and how to move it up the chain.

Technical knowledge is only part of it. People need straightforward guidance on the workflow itself, where the decision points sit, and how to use the tools they've been given. That cuts down on guesswork and keeps reviews from looking different every time someone runs one.

Training shouldn’t be a one-time effort. As systems change, teams need updates so they can keep up with new risks and behaviors.

—

For many fintech teams, translating Article 14 into actual workflows is where things get complex. This is where structured compliance platforms like Regly can help. Built by regulatory experts with hands-on fintech experience, Regly helps teams define oversight processes, manage reviews, and document decisions in a way that aligns with regulatory expectations.

Governance and Documentation Requirements

Human oversight doesn’t sit on its own. It needs to be supported by clear governance structures and documentation that show how controls are defined and applied.

1. Oversight Procedures in Technical Documentation

Oversight procedures should be clearly reflected in technical documentation. This includes:

How the system works

Where human review happens

What controls are in place

Documentation should describe decision flows, intervention points, and any thresholds or triggers that guide oversight. It should also explain what information is available to reviewers and how outputs can be interpreted.

This level of detail helps align technical teams and compliance teams. It also makes it easier to explain how oversight is applied if regulators request it.

2. Logging and Monitoring Requirements

Oversight only works if there's a clear record of what the system has been doing. Without documentation, logs, and monitoring, going back to understand how a decision got made or catching a problem early becomes guesswork. Systems should capture key events such as inputs, outputs, overrides, and alerts. This makes it easier to review past decisions and identify patterns that may need attention.

Monitoring needs to flag changes in how the system is behaving, too. If outputs start drifting or performance slips, teams need to see it quickly enough to dig in and respond.

Learn more about document management for compliance teams →

3. Audit Trails for AI Decisions

Audit trails help teams track how decisions were made and who was involved. This becomes important when decisions are questioned, either internally or by regulators.

A complete audit trail should show:

The data used

The system’s output

Any human actions taken

This includes reviews, overrides, and escalations. Each step should be time-stamped and linked to the person or role responsible.

Clear audit trails make it easier to investigate issues and explain outcomes. They also support accountability by showing that oversight isn’t just defined, but actively applied.

Learn more about audit trails →

4. Internal Controls and Risk Management Integration

Human oversight needs to plug into the risk and compliance controls already running. It shouldn't sit off to the side as its own thing.

For most fintech companies, that means connecting AI oversight to existing frameworks, such as risk assessments, incident management, and internal controls. If oversight flags an issue, that issue should move into the same review, escalation, and remediation processes the firm already relies on.

This connection also helps with accountability. When oversight activities are tied to broader control frameworks, it becomes easier to track issues, assign ownership, and follow through on remediation.

Folding oversight into what teams already do keeps it workable. There's no need to spin up a brand new program from scratch, but the controls already in place do need to bend to account for how AI systems actually behave.

Key Enforcement and Supervisory Authorities Under the EU AI Act

Enforcement of the EU AI Act is handled at both the EU and national levels. Different authorities play a role in supervising how requirements, including human oversight, are applied.

EU AI Office

The EU AI Office helps guide how the EU AI Act is applied across different countries. It works with national regulators to keep expectations aligned and avoid conflicting interpretations.

It also provides practical guidance on how companies should apply the rules. This includes areas like high-risk classification and human oversight, which can be hard to interpret without clear direction.

For companies, this means the AI Office will shape how requirements are understood over time. As more guidance is released, it will influence how firms design their controls and respond to regulatory expectations.

National Market Surveillance Authorities

National market surveillance authorities are the regulators responsible for enforcing the EU AI Act within each member state. They review how companies are applying the rules and can look into potential issues or signs of non-compliance.

These authorities review whether high-risk AI systems meet requirements such as human oversight, documentation, and risk controls. If something doesn’t meet expectations, they can request changes or take further action.

For fintech companies that operate across multiple countries, this can mean dealing with more than one regulator. The EU AI Office plays an important role in aligning guidance and overseeing certain obligations for general-purpose AI models, but much of the everyday supervision and enforcement still happens at the national level.

Potential Penalties for Non-Compliance

The EU AI Act includes financial penalties for companies that don’t meet its requirements. The size of the penalty depends on the type of violation and how serious it is.

For high-risk systems, failures around oversight, risk management, or documentation can lead to significant fines. These can reach a percentage of global annual turnover, which makes compliance a board-level concern for many firms.

Penalties go beyond fines. Regulators can restrict or suspend an AI system that doesn't meet the standard, which hits operations hard if the system runs something central to the business.

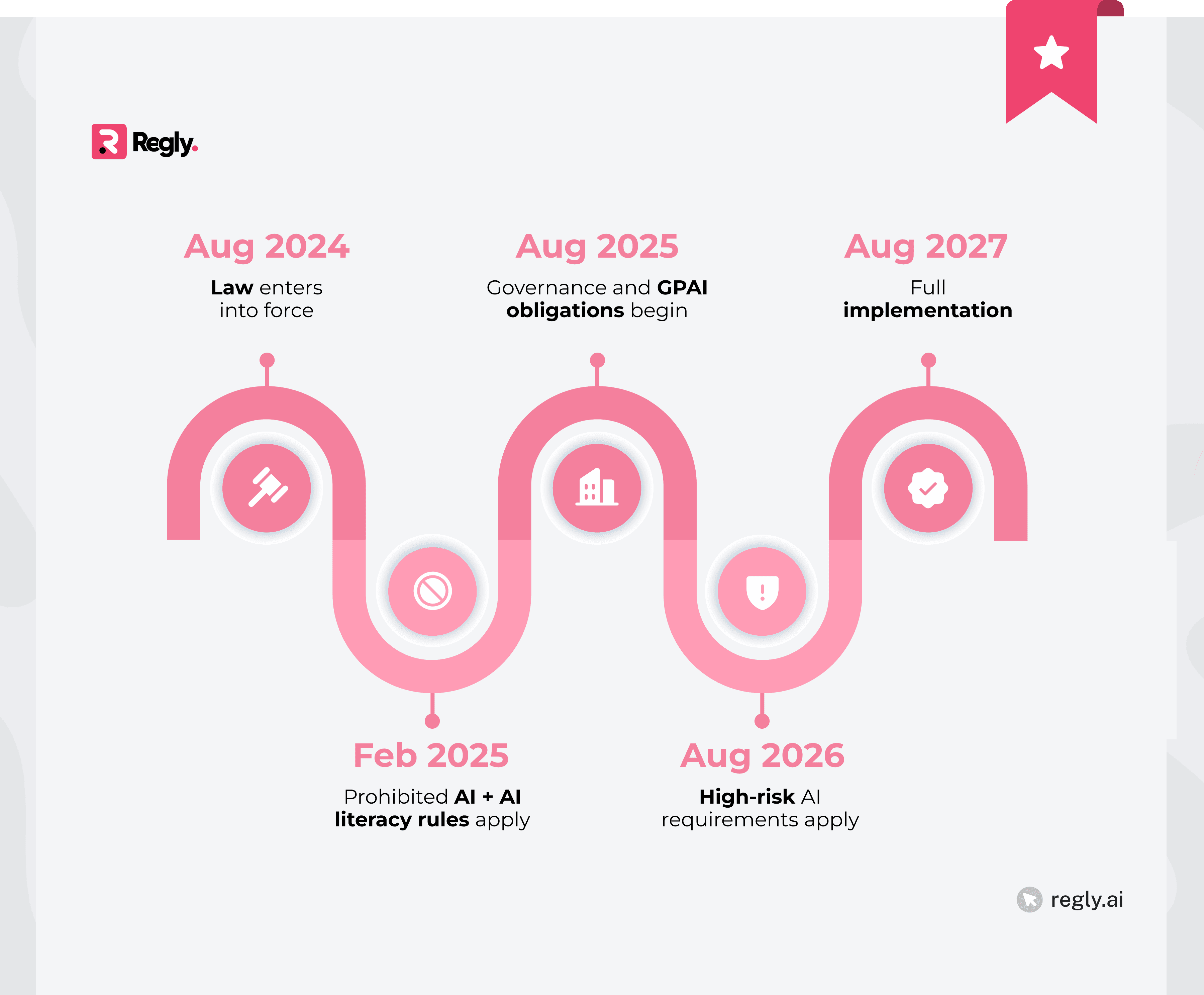

Key Dates and Implementation Timeline for the EU AI Act

The EU AI Act is phased in over several years, with each stage introducing different obligations. The timeline matters because requirements don’t hit all at once, but some areas move faster than others.

August 1, 2024 – Entry into force

The regulation officially became law. From this point, firms should start assessing whether they use high-risk AI and where gaps exist in oversight, documentation, and controls.

February 2, 2025 – Prohibited AI and AI literacy requirements apply

Certain AI use cases are banned, and companies are expected to build internal awareness around AI risks. This is often the first operational step, especially for firms still mapping their AI usage.

August 2, 2025 – Governance and general-purpose AI obligations begin

This stage introduces more structure around how AI is managed. It also starts shaping expectations for documentation and accountability, which connect directly to oversight requirements.

August 2, 2026 – High-risk AI requirements apply

This is the key deadline for most fintech use cases. Requirements around human oversight, risk management, monitoring, and documentation become enforceable for many high-risk AI systems. Systems need to be aligned with Article 14 by this point.

August 2, 2027 – Full application across all systems

Remaining obligations come into force, including those affecting legacy systems. By this stage, firms are expected to have fully integrated compliance into their operations.

For fintech teams, the most important milestone is 2026. That’s when human oversight stops being a planning exercise and becomes a regulatory expectation tied to real enforcement.

—

Article 14 of the EU AI Act emphasizes that AI systems must have human oversight, especially when outputs can meaningfully impact significant decisions. Firms can still rely on automation, but they need to stay in control of how systems behave and how outcomes are handled.

For fintech companies, this comes down to building oversight into everyday operations. It’s not just about policies. It’s about having the right controls, visibility, and workflows in place so teams can act when needed.

As the regulation moves closer to full enforcement, firms that take a practical approach will be in a stronger position. Those who treat oversight as a theoretical requirement may run into problems once regulatory expectations become active supervision.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.