Personal account dealing is a recurring challenge for fintech firms operating in regulated environments. As teams grow and products evolve, employees often gain access to sensitive information, trading activity, or upcoming business decisions.

Without clear controls, personal trading can create conflicts of interest, raise market abuse concerns, and expose the firm to regulatory scrutiny.

Regulators in the UK and EU expect firms to manage personal account dealing through structured policies, monitoring, and oversight. Firms are required to understand who is in scope, what activity needs to be tracked, and how to identify and escalate potential issues.

For fintechs, this becomes more complex due to multi-asset platforms, distributed teams, and fast product cycles.

This article explains how personal account dealing works in practice, the regulatory frameworks that apply, and how fintech firms can build and operate a compliance program that is both practical and aligned with regulatory expectations.

What Is Personal Account Dealing?

Personal account dealing (PA dealing) refers to trading in financial instruments by employees or other relevant persons for their own benefit, rather than on behalf of clients or the firm. The concept is primarily used in UK and EU regulation, but the underlying risk it addresses exists across all financial markets.

The focus is not on whether employees are allowed to invest. It is on how those investments interact with the firm’s obligations, client activity, and access to sensitive information. In practice, regulators expect firms to identify where personal trading could create conflicts or misuse of information and put controls around it.

In regulatory terms, personal account dealing is closely tied to conflicts of interest and market abuse prevention. That is why it sits alongside broader conduct and surveillance requirements, rather than being treated as a standalone policy topic.

Who Is Considered a Relevant Person or Access Person

The scope of personal account dealing rules depends on who the regulator considers “in scope.” In the UK and EU frameworks, this typically includes “relevant persons”, while in the US, similar roles are called “access persons.”

Fintech firms often need to go further. Engineers, product managers, and data teams may have visibility into upcoming listings, pricing changes, or strategic decisions. That visibility can create the same risks regulators are concerned about.

What Counts as a Personal Transaction

A personal account dealing transaction generally includes any trade in financial instruments carried out for the benefit of an employee or a connected person. This goes beyond trades executed directly in the employee’s name.

Regulators typically look at control and benefit, not just ownership. If an employee can influence trading decisions or benefit from the outcome, the activity is likely in scope.

Examples of Personal Account Dealing in Financial Firms

Personal account dealing can arise in different ways depending on how a firm operates. For example, an employee might purchase shares shortly before a large client order is executed in the same security, or a product team member might trade a token before it becomes available on the platform.

In other cases, a compliance officer may use an undeclared external account, or an employee may route trades through a relative’s account to bypass internal approval requirements.

These situations are not hypothetical. They reflect patterns that regulators have identified through enforcement actions and supervisory reviews.

For fintech firms, the issue goes beyond defining these scenarios. It involves understanding where these risks can surface across different teams and putting controls in place that reflect how the business actually functions.

Why Personal Account Dealing Creates Compliance Risk

Personal account dealing turns into a compliance risk when employees trade while having visibility into client activity or confidential information. Investing personally is not the problem. The issue is when those trades put personal interests at odds with the firm’s obligations.

Conflicts Between Employee Trading and Client Interests

A common issue arises when employee trading overlaps with client activity. For example, someone might place a trade in the same instrument as a client while already aware of pending orders or internal recommendations.

What matters here is not just when the trade happens, but what the employee knows at the time. Access to client information, even in a limited form, can influence personal decisions in ways that conflict with the firm’s obligations.

In fintech firms, this exposure is not limited to trading desks. People working on pricing models, execution systems, or product features may also come across information that can affect trading behavior.

Misuse of Material Non-Public Information (MNPI)

Personal account dealing is closely linked to the risk of using material non-public information. MNPI can include knowledge of client orders, upcoming listings, corporate actions, or internal strategic decisions.

Trading based on MNPI is a core regulatory concern across jurisdictions. Even where intent is unclear, patterns of trading around sensitive events can trigger scrutiny.

For fintech firms, MNPI is not limited to front-office teams. Product and engineering teams may have early access to information that can influence market activity. This makes internal access controls and awareness critical.

Learn more about MNPI and conflicts of interest →

Front-Running and Market Abuse Risks

Front-running is a specific form of misconduct where an employee trades ahead of a known client's order to benefit from expected price movement. It is a clear example of how personal account dealing can cross into market abuse.

Market abuse risks extend beyond front-running and include insider dealing and improper disclosure of information. Regulators in the UK and EU often assess personal account dealing within this broader framework.

Even where activity does not meet the legal threshold for market abuse, patterns that resemble it can still lead to internal investigations and regulatory attention.

Reputational and Regulatory Consequences

Gaps in how personal account dealing is handled rarely stay isolated. If monitoring is inconsistent or reviews are not documented, it tends to point to wider weaknesses in how the compliance program is run.

Supervisors often use this area to form a broader view of conduct risk. When firms are reviewed, the expectation is to show how activity is tracked, how issues are escalated, and what happens after a breach is identified.

For fintech firms working across markets, the implications can extend further. It can affect regulatory relationships, due diligence processes, and how the business is viewed by partners or investors. For that reason, this is usually treated as a central part of the compliance setup.

—

The risks around personal account dealing are rarely isolated. They tend to reflect how well a firm understands internal access to information and how effectively it monitors employee activity across teams.

In practice, this is where many fintech firms struggle. Not with defining the rules, but with applying them consistently across different roles and systems.

See how Regly helps fintechs manage outside account and employee compliance tasks →

Key Regulations Governing Personal Account Dealing

The term personal account dealing comes from the UK and EU regulatory frameworks, where it is used directly in the rules. These frameworks focus on managing conflicts, limiting the use of non-public information, and supporting fair market behavior.

UK Personal Account Dealing Rules (FCA)

The UK has one of the more established approaches to personal account dealing. The FCA covers it directly in its Conduct of Business Sourcebook (COBS), alongside wider conduct and market abuse requirements.

FCA COBS Personal Account Dealing Requirements

Under FCA COBS rules, firms must establish arrangements to prevent employees from engaging in personal transactions that create conflicts or involve the misuse of information.

These arrangements typically require firms to:

Identify relevant persons subject to PAD rules

Require disclosure of personal accounts

Monitor employee trading activity

Maintain records of approvals, restrictions, and transactions

The rules are principles-based, which means firms need to interpret them in the context of how their business operates. For fintech firms, this often requires extending controls beyond traditional trading roles.

UK Market Abuse Regulation (UK MAR) and Employee Trading

UK MAR sits alongside PAD rules and shapes how firms approach employee trading risk. It focuses on preventing insider dealing, unlawful disclosure, and market manipulation.

Personal account dealing controls are often used as a first line of defense against market abuse risks. If employees have access to inside information, their personal trading activity becomes a direct area of regulatory interest.

Firms are expected to connect PAD monitoring with broader surveillance systems, particularly where trading patterns could indicate misuse of information.

SM&CR and Individual Accountability

The Senior Managers and Certification Regime (SM&CR) adds an accountability layer to personal account dealing. Senior managers are responsible for how risks, including PAD, are managed within their areas of responsibility.

This means that failures in personal account dealing controls can lead to questions not just about the firm, but about individual accountability.

For fintech firms, where roles and responsibilities may evolve quickly, maintaining clear ownership of PAD controls becomes particularly important.

Area | Regulatory Focus | Regulatory Focus |

|---|---|---|

FCA COBS | Conflicts and employee trading | Identify relevant persons, monitor trades, keep records |

UK MAR | Market abuse prevention | Detect misuse of information and suspicious trading patterns |

SM&CR | Accountability | Assign clear responsibility for PAD oversight |

EU Personal Account Dealing Rules (MiFID II)

In the EU, personal account dealing is framed as “personal transactions” under MiFID II. The focus is similar to the UK, but the terminology differs slightly.

Definition of Personal Transactions Under MiFID II

MiFID II defines personal transactions broadly. It includes trades carried out by employees, as well as transactions executed on their behalf or for their benefit.

This typically covers:

Personal accounts held at any institution

Accounts of connected persons

Situations where the employee has influence or control over trading decisions

The emphasis is on economic interest and influence, not just ownership.

Organizational and Monitoring Requirements

MiFID II requires firms to implement procedures that allow them to detect and review personal transactions. This includes requiring employees to notify the firm of their trades and maintaining records of those transactions.

There is a strong expectation that firms can identify personal trading activity across all accounts, not just those held internally. This is particularly relevant for fintech firms, where employees may use multiple platforms or asset types.

In the EU, MiFID II personal transaction rules operate alongside the Market Abuse Regulation (EU MAR), which addresses insider dealing, unlawful disclosure, and market manipulation. Personal account dealing controls are often used as a first line of defense against these risks.

Requirement | UK (FCA) | EU (MiFID II) |

|---|---|---|

Terminology | Personal account dealing | Personal transactions |

Scope (who) | Relevant persons | Relevant persons and connected accounts |

Objective | Conflicts of interest and conduct risk | Conflicts of interest and conduct risk |

Controls | Pre-approval, restrictions, monitoring | Procedures to prevent conflicts, restrictions, monitoring |

Recordkeeping | Required | Required |

Who Must Follow Personal Account Dealing Rules

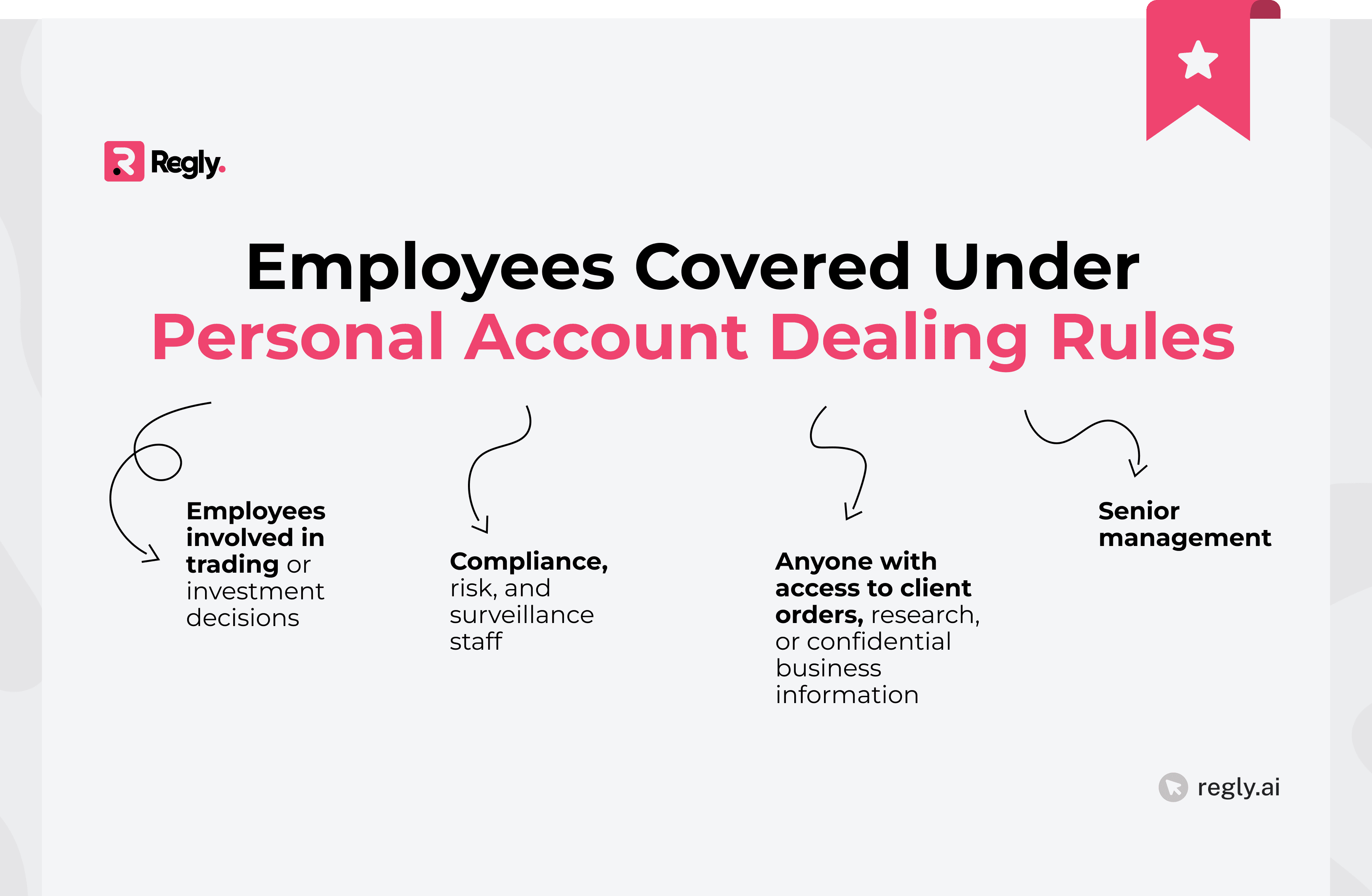

Personal account dealing rules apply based on access, not job title. Regulators focus on who can influence trading decisions or access sensitive information, rather than limiting scope to front-office roles.

Access Persons and Supervised Employees

At the core of most frameworks are individuals directly involved in investment decisions or client activity. This includes portfolio managers, traders, analysts, and others who contribute to recommendations or execution.

These individuals are typically considered high-risk because of their direct influence on trading activity. As a result, they are usually subject to stricter controls such as pre-clearance, reporting requirements, and ongoing monitoring.

In some cases, firms extend this classification to anyone who regularly receives investment-related information, even if they are not making final decisions.

Learn what an access person is in the RIA context →

Senior Management and Compliance Staff

Senior management and compliance teams are often included within the scope of personal account dealing rules. While they may not execute trades for clients, they have visibility into business strategy, internal decisions, and sensitive information.

This creates a different type of risk. The concern is not execution, but access and influence. For example, a senior manager may be aware of upcoming partnerships, capital raises, or product changes that could affect market activity.

Compliance staff presents a separate consideration. They often review employee trading and investigations, which means firms need to address potential conflicts in how their own activity is monitored.

Employees With Access to Confidential Information

Personal account dealing rules also apply to employees who may not be directly involved in trading but have access to confidential or price-sensitive information.

This can include:

Product teams working on new listings or features

Engineering teams with visibility into system-level activity

Data teams analyzing trading patterns or client behavior

In fintech firms, this group is often larger than expected. Access to internal systems or product pipelines can create the same risks regulators are concerned about, even if the employee is not part of a trading function.

Family Members and Controlled Accounts

Regulators extend personal account dealing requirements beyond the employee’s own accounts. The focus is on control and economic benefit.

This typically includes:

Accounts held by spouses or partners

Accounts of dependents

Any account where the employee can influence trading decisions

If an employee can direct or benefit from trading activity, it is generally treated as in scope. This is why firms require disclosure of connected accounts and, in many cases, apply the same controls as they would to personal accounts.

—

The scope of personal account dealing is often broader than firms expect. It is not limited to trading roles, but extends to anyone with access to information that could influence markets or client activity.

The key challenge is identifying all individuals and accounts that fall within scope, based on access and influence rather than titles. This becomes more complex in fintech firms, where information is distributed across product, engineering, and data teams.

See how Regly helps fintechs manage outside accounts →

Types of Personal Account Dealing Restrictions

Personal account dealing rules are implemented through a set of practical restrictions that control how and when employees can trade. These controls are designed to reduce conflicts, limit misuse of information, and create a clear record of activity.

Pre-Trade Approval Requirements

Pre-clearance means employees need to get approval before placing certain trades. This gives compliance a chance to review the request in advance and flag any potential conflicts.

It is usually applied where the risk is higher, such as securities clients who are actively trading, instruments tied to internal recommendations, or transactions like IPOs and private placements.

Reviewing trades upfront allows firms to deal with conflicts before they materialize. It also leaves a record of decisions that can be referenced during audits or regulatory reviews.

Restricted Lists and Watch Lists

Firms often maintain internal lists of securities that employees cannot trade or that require additional scrutiny. These lists are usually divided into restricted lists and watch lists.

A restricted list typically includes securities where trading is prohibited due to active client activity or access to inside information. A watch list may include securities that require closer monitoring but are not fully restricted.

These lists are a key tool for aligning employee trading with what the firm knows internally. They need to be updated regularly to reflect current activity and information flows.

Blackout Periods Around Sensitive Events

Blackout periods are defined windows where employees are not allowed to trade. They are typically scheduled around events that involve sensitive information, such as earnings, product releases, or major client activity.

These restrictions are meant to reduce the risk of trades being influenced by information that is not yet public.

In fintech environments, blackout periods may also be triggered by events like token listings, platform changes, or updates to pricing mechanisms.

Minimum Holding Periods

Blackout periods are time-based restrictions that limit trading during specific events or windows. These are commonly applied around earnings releases, new product launches, or large client transactions.

The goal is to prevent employees from trading when they are more likely to have access to non-public or sensitive information.

In fintech firms, blackout periods may also apply to events such as token listings, platform updates, or changes in pricing models.

Prohibited Transactions

Certain types of transactions may be completely prohibited under personal account dealing rules. This can include trading in specific instruments, participating in certain offerings, or using particular strategies.

Examples may include:

Trading in securities on the restricted list

Participating in IPOs without approval

Short-term trading strategies that create conflicts

These prohibitions are usually tied to areas where the risk cannot be effectively managed through monitoring alone.

Restriction Type | Purpose | Typical Application |

|---|---|---|

Pre-clearance | Review trades before execution | High-risk securities, IPOs |

Restricted lists | Prevent trading in sensitive securities | Active client positions, inside information |

Blackout periods | Limit trading during key events | Earnings, listings, major transactions |

Holding periods | Reduce short-term trading risk | Earnings, listings, major transactions |

Prohibited trades | Eliminate high-risk activity | Employee investment activity |

Personal Account Dealing Reporting Requirements

Personal account dealing frameworks rely heavily on reporting. Without consistent disclosures and transaction data, firms have limited visibility into employee activity. Reporting is what turns policies into something enforceable. It allows compliance teams to track behavior, identify exceptions, and maintain records that can be reviewed internally or by regulators.

Employee Brokerage Account Disclosures

Firms typically require employees to disclose all personal brokerage accounts. This includes accounts held with external providers, not just those linked to the firm.

The goal is to create a complete inventory of where trading activity may occur. Without this, monitoring is incomplete from the start.

Most frameworks expect firms to capture both direct and beneficial ownership of accounts. This includes accounts where employees have control or influence, even if they are not the named holder.

Learn more about outside brokerage accounts →

Transaction Reporting Requirements

Most firms require employees to disclose their personal trades within a specific timeframe. Depending on the setup, this may involve manual reporting or automated data coming from brokerage accounts.

Compliance teams then check these trades against internal activity, including client orders, restricted lists, and relevant business events.

This makes it easier to spot conflicts or patterns that need attention, while also maintaining a clear history of activity.

Holdings Reports and Periodic Certifications

In addition to transaction-level reporting, firms often require employees to submit holdings reports. These provide a snapshot of positions held at a given point in time.

Periodic certifications are also common. Employees may be asked to confirm that:

All accounts have been disclosed

All required trades have been reported

They are following the firm’s personal account dealing policy

These certifications help reinforce accountability and highlight gaps in reporting. They also give compliance teams a structured way to validate employee disclosures.

External Brokerage Accounts and Duplicate Statements

To strengthen oversight, many firms require duplicate statements or direct data feeds from external brokers. This reduces reliance on self-reporting and provides a more complete view of activity.

Where automated feeds are not available, firms may request periodic account statements. These are then reviewed alongside reported transactions.

For fintech firms, this can be more complex. Employees may use multiple platforms, including crypto exchanges or newer trading apps that do not support standard reporting integrations.

Monitoring Personal Account Dealing Activity

Reporting provides the data. Monitoring is where that data is reviewed and acted on. Without a structured review process, personal account dealing controls remain incomplete. Monitoring is what allows firms to detect issues, not just record them. It connects employee trading activity with client behavior, internal information, and known risk events.

Reviewing Employee Trades Against Client Trades

One of the core monitoring steps is comparing employee trades with client transactions. This helps identify situations where personal trading may overlap with client activity.

Reviews usually focus on when the trade happened, how large it was, and whether it aligned with client activity. For instance, whether an employee traded just before or after a client order in the same security.

The aim is to spot situations where timing or positioning raises questions. Even if nothing improper is confirmed, these cases are often looked at more closely.

Identifying Suspicious Trading Patterns

Monitoring goes beyond comparing individual trades. Firms also look at activity over time to understand broader patterns.

This might include repeated trades ahead of key events, consistent gains during sensitive periods, or activity that lines up with internal developments.

In fintech settings, this can extend to newer areas such as crypto markets, token listings, or changes within the platform itself.

Recordkeeping and Audit Trails

Monitoring activity needs to be documented. Each review, decision, and escalation should leave a trace that can be revisited later.

This includes:

Records of trade reviews

Notes on identified issues

Outcomes of investigations

Evidence of follow-up actions

Clear audit trails are critical during regulatory reviews. Firms are expected to show not only that monitoring takes place, but also how decisions are made and documented.

See how Regly Compliance helps fintechs centralize audit trails →

Escalation and Investigation Procedures

Not every flagged trade results in a breach, but each one still needs to be reviewed. That means having a clear process for how issues are handled once they are identified.

In most cases, this starts with a compliance review, followed by gathering context from the employee and assessing whether the activity falls outside policy. The outcome and any follow-up steps are then documented.

Having a consistent approach makes it easier to handle similar situations in the same way and avoids uneven treatment across cases.

Managing Personal Account Dealing in Fintech Environments

Personal account dealing becomes more complex in fintech firms because of how information is distributed and how quickly products evolve. Traditional controls were designed for clearly defined roles and systems. Fintech environments often do not follow that structure.

Distributed Teams and Remote Employees

Many fintech firms operate with distributed teams across locations and time zones. This changes how information is shared and how oversight is applied.

Employees may access systems, data, and trading activity remotely, often outside of traditional supervision structures. This can make it harder to track who has seen what information and when.

Personal account dealing controls need to account for decentralized access to information. Static approvals or location-based supervision are often not enough in this setup.

Multi-Asset Trading Including Crypto

Fintech platforms often support multiple asset classes, including equities, derivatives, and digital assets. Each of these comes with different trading patterns, liquidity profiles, and reporting standards.

Crypto, in particular, introduces additional complexity. Trading can occur across multiple exchanges, some of which may not provide standardized reporting or integration.

This makes it more difficult to maintain a complete view of employee trading activity. Firms need to account for fragmented trading environments and inconsistent data sources.

Engineers and Product Teams With Sensitive Data Access

In many fintech firms, access to sensitive information is not limited to trading or investment teams. Engineers, product managers, and data teams may have visibility into upcoming features, listings, or system changes.

This creates a broader exposure surface. Someone working on a product release or pricing update may have information that could influence trading decisions.

Personal account dealing policies need to reflect where information actually sits within the organization. Limiting controls to traditional roles often leaves gaps.

Rapid Product Launches and Information Asymmetry

Fintech companies tend to move quickly, with regular product updates and releases. This often means information is shared internally before it reaches the market.

Events like token listings, pricing adjustments, or new feature rollouts can create brief periods where employees are working with non-public information.

In these situations, timing matters. Controls such as blackout windows or pre-clearance need to reflect how fast these changes happen.

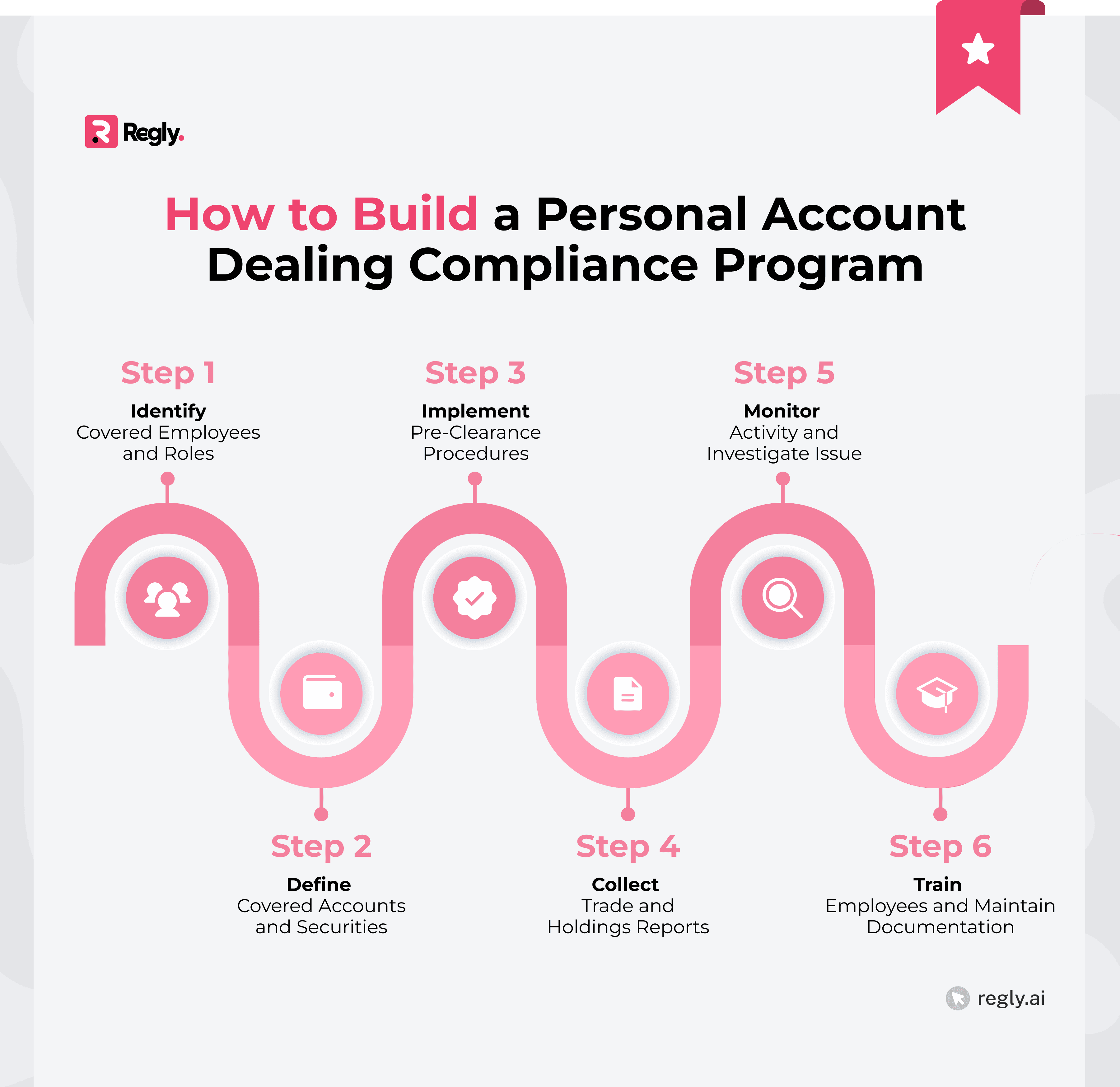

How to Build a Personal Account Dealing Compliance Program

Personal account dealing controls are only effective when they are applied consistently across the organization. That requires more than a written policy. It requires a structured program that reflects how the firm operates.

Step 1: Identify Covered Employees and Roles

The starting point is defining who falls within scope. This should be based on access to information and influence over trading, not just formal titles.

In fintech firms, this often includes a wider group than expected. Product teams, engineers, and data roles may all need to be included, depending on their access.

If the scope is too narrow, the rest of the program will not capture the actual risk. This step sets the foundation for everything that follows.

Step 2: Define Covered Accounts and Securities

Once employees are identified, firms need to determine which accounts and instruments fall under personal account dealing rules.

This includes personal brokerage accounts, accounts held with external providers, and accounts where the employee has influence or beneficial interest.

Firms should also define which securities or asset types require additional controls, especially in multi-asset environments.

Step 3: Implement Pre-Clearance Procedures

Pre-clearance introduces a control point before trades are executed. Employees request approval, and compliance reviews the request based on available information.

This is particularly relevant for higher-risk trades or situations where conflicts are more likely.

Pre-clearance works best when it is tied to real-time information such as client activity and restricted lists. Without that connection, reviews become less effective.

Step 4: Collect Trade and Holdings Reports

Reporting allows firms to track employee activity after trades occur. This includes both transaction-level data and periodic holdings snapshots.

The process should capture activity across all relevant accounts, including external platforms and newer asset classes where possible.

Consistency matters here. Gaps in reporting make monitoring less reliable and increase the chance of missing issues.

Step 5: Monitor Activity and Investigate Issues

Once data is collected, it needs to be reviewed in context. This involves comparing employee trades with client activity, internal information, and known events.

Where potential issues are identified, firms need a process for reviewing and documenting outcomes.

Monitoring is where personal account dealing controls become operational. Without it, reporting remains passive.

Step 6: Train Employees and Maintain Documentation

Employees need to understand what is expected of them and how the rules apply in practice. Training should cover both policy requirements and real-world scenarios.

Documentation is equally important. Firms need to maintain records of disclosures, approvals, reviews, and investigations.

This supports internal oversight and provides evidence during regulatory reviews.

How Technology Helps Manage Personal Account Dealing

As firms scale, manual processes around personal account dealing become harder to maintain. Spreadsheets, email approvals, and fragmented data sources make it difficult to keep a consistent view of employee activity. Technology is often introduced to centralize these processes and reduce reliance on manual tracking.

Automating Employee Trade Reporting

One of the first areas where technology is applied is trade reporting. Instead of relying on employees to submit trades manually, firms can connect brokerage accounts or use structured reporting workflows.

This reduces delays and gaps in reporting. It also standardizes how data is captured across different employees and platforms.

Automated reporting helps create a more complete and timely view of personal account dealing activity. That becomes important when monitoring depends on accurate data.

Monitoring Personal Trading Risks

Technology can support ongoing monitoring by comparing employee trades with internal data. This includes client activity, restricted lists, and known events.

Rather than reviewing trades individually, systems can flag patterns or scenarios that require attention. This allows compliance teams to focus on higher-risk activity.

In fintech environments, this is particularly useful where trading spans multiple asset classes and platforms.

Managing Approvals and Compliance Workflows

Pre-clearance and approvals can become difficult to track when handled through email or informal processes. Technology helps structure these workflows.

Employees can submit requests through a centralized system, and compliance teams can review and respond in a consistent format. Each step is recorded, creating a clear audit trail.

Structured workflows reduce inconsistencies in how approvals are handled across teams. They also make it easier to track outstanding requests and past decisions.

Maintaining Audit-Ready Records

Documentation is a core requirement in personal account dealing programs. Technology helps centralize records of disclosures, approvals, trade reviews, and investigations.

This becomes important during regulatory reviews, where firms are expected to show how controls operate in practice.

Instead of pulling data from multiple sources, firms can rely on a single system to provide a complete view of activity and decisions.

Regly Employee Compliance

Managing personal account dealings often involves multiple moving parts. Account disclosures, trade reporting, approvals, monitoring, and documentation all need to work together.

Regly’s employee compliance solution is designed to centralize these processes into a single workflow. Based on InnReg’s experience of working with 100+ fintechs, it allows firms to manage employee disclosures, track personal trading activity, and maintain records in one place.

For firms operating across products and jurisdictions, this approach helps align personal account dealing controls with how the business actually runs.

—

Personal account dealing is not a standalone compliance task. It sits across conflicts of interest, market abuse, employee conduct, and internal controls.

The challenge for fintech firms is not defining the rules, but applying them in environments where access to information is broad and constantly changing. As teams expand and products evolve, the scope of personal account dealing tends to grow with them.

In practice, effective programs are built around visibility, consistent processes, and systems that reflect how the business actually operates.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.