Conflict of Interest in Fintech: What It Is and How to Manage It

Published on

Mar 17, 2026

13

min read

Conflicts of interest are a core concern for fintechs. When a company or employee has competing interests that could compromise their objectivity, the result isn’t just bad optics. It’s a regulatory risk, a trust issue, and in some cases, a trigger for enforcement.

Managing conflicts of interest, however, can be complex. Compensation structures, product design, partnerships, and operations can create friction between what’s best for the client and what’s best for the business.

This article unpacks what conflicts of interest look like in the fintech ecosystem: how regulators define them, where they tend to show up, and what practical steps firms can take to address them.

What Is a Conflict of Interest in Financial Services?

A conflict of interest occurs when a person or entity has multiple obligations, relationships, or incentives that could compromise their ability to act in someone else’s best interest.

In financial services, this usually means putting a firm's or an employee's gain ahead of a client’s interest (intentionally or not).

Conflicts can be direct or indirect. A direct conflict might involve an advisor recommending a product that pays them more, even if it's not the best fit for the client. An indirect one could be a fintech platform steering users toward partners that offer referral payments.

In many cases, the conflict isn’t the issue. Failing to manage or disclose it is. Regulators understand that conflicts exist in every business model. What they expect is transparency and a structure that prevents those conflicts from leading to harm.

For fintechs, this gets especially complicated. Rapid growth, novel products, and hybrid business models (think crypto + trading + lending) can all create overlaps that introduce conflict. Identifying them early and documenting them clearly is a necessary first step in building any credible compliance program.

Why Conflicts of Interest Matter for Fintechs

Fintech firms are built on innovation, speed, and scale. But those same traits can introduce blind spots when it comes to regulatory expectations. Conflicts of interest are one of the most common and costly risks in that gap.

They can lead to real-world harm: customers paying more than they should, biased product recommendations, or hidden incentives that compromise transparency. Regulators see this as more than a disclosure issue. It’s a matter of conduct and fairness.

Conflicts don’t just live at the business or product level. They show up in employee behavior, too. Personal trading, side businesses, financial interests, and even vendor relationships can introduce individual-level conflicts that trigger firmwide compliance risk. That’s why many fintechs adopt policies governing outside business activities, gifts and entertainment, and personal account trading.

It’s a core part of employee compliance, which gets significant attention. If you’re building or refreshing that side of your program, we recommend reviewing our guides on Outside Business Activities and employee trade monitoring.

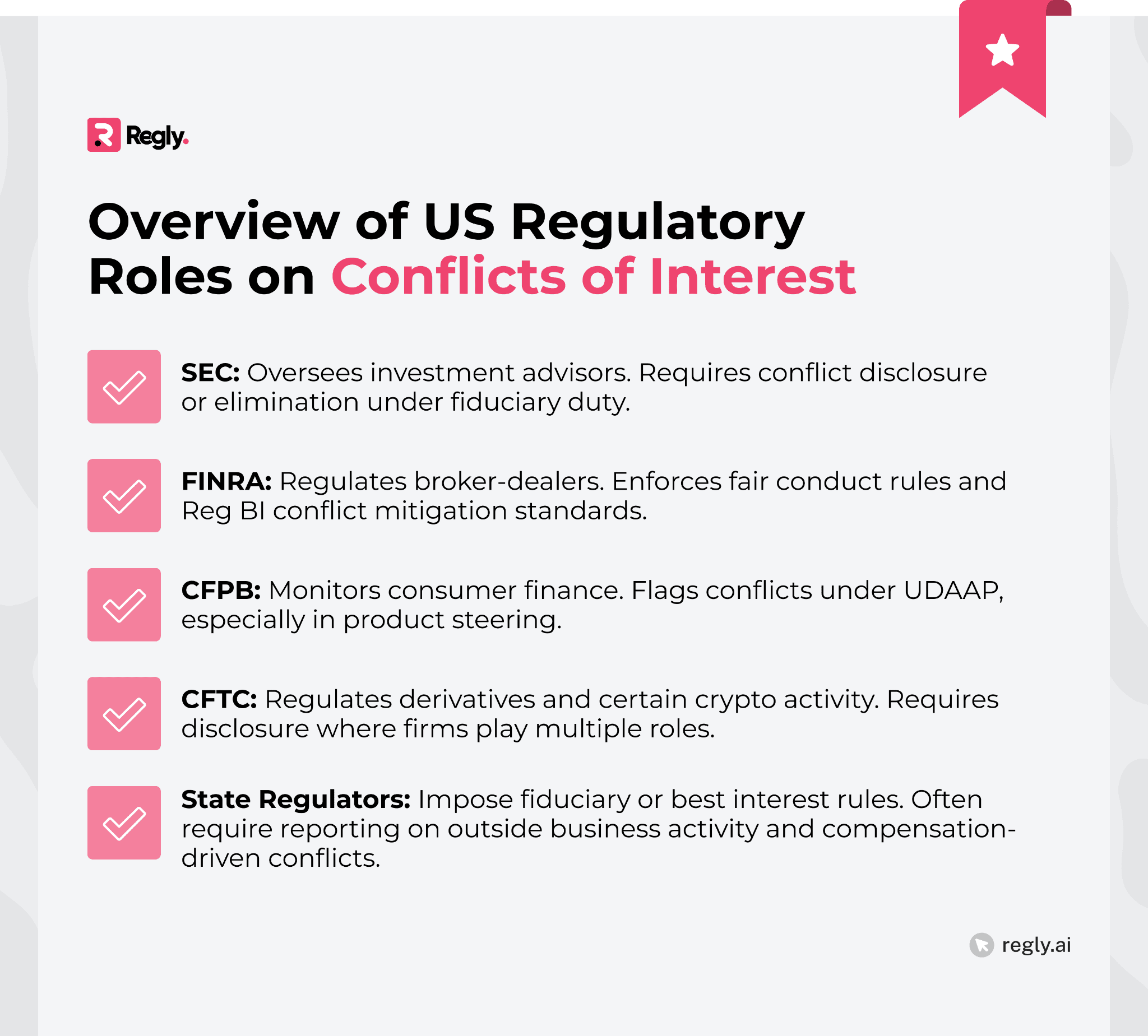

Key US Regulators and Their Stance on Conflicts of Interest

Several US regulators oversee how fintechs manage conflicts of interest, depending on their licensing and business model. Each has its own rules, but transparency and mitigation are common themes.

SEC: Fiduciary Duty and Adviser Conflicts

Registered investment advisors are held to a fiduciary standard under the Investment Advisers Act of 1940. That standard is broad, but its core is clear: advisors must act in the best interest of their clients at all times.

Conflicts of interest are a direct threat to that standard. The Securities and Exchange Commission (SEC) expects firms to either eliminate conflicts or disclose them in a way that allows the client to make an informed decision. Vague language, buried disclosures, or technical jargon don’t meet the bar.

Common SEC focus areas include:

Use of proprietary products or affiliated funds

Revenue-sharing and referral arrangements

Personal trading by investment personnel

Dual registration with a broker-dealer

Disclosure alone is not always enough. If a conflict materially benefits the firm and harms the client, the SEC may expect stronger mitigation or expect the firm to avoid the arrangement altogether.

FINRA: Broker-Dealer Rules and Reg BI

For broker-dealers, conflicts of interest are addressed under both FINRA rules and Regulation Best Interest (Reg BI). These requirements apply when dealing with retail customers, and they go beyond simple disclosure.

Financial Industry Regulatory Authority (FINRA) has long required firms to uphold fair dealing and honest practices under Rule 2010. But Reg BI, introduced by the SEC, raised the bar. Under Reg BI, brokers must act in the customer’s best interest when making recommendations, and they must identify, disclose, and mitigate conflicts that might influence those recommendations.

Key areas of regulatory focus include:

Compensation structures that reward the sale of certain products

Revenue-sharing with third parties

Sales contests and production quotas

Order routing decisions (e.g., payment for order flow)

Reg BI draws a line on certain conflicts. Sales contests tied to specific products or short-term volume targets are off-limits. Broader compensation systems that push one option over another may also raise concerns, depending on how they're structured.

For fintech broker-dealers, especially those relying on volume-based revenue streams, this means pressure-testing business models. Disclosure is part of the equation, but how you manage internal incentives matters just as much.

CFPB, CFTC, and State Regulators

Not all conflicts of interest fall under the SEC or FINRA. Other regulators step in depending on the type of activity, especially in lending, derivatives, and state-regulated financial products.

The Consumer Financial Protection Bureau (CFPB) looks closely at consumer-facing practices, including how companies design and recommend financial products. If a firm pushes users toward higher-cost options simply because they’re more profitable, that can raise red flags under UDAAP standards.

The Commodity Futures Trading Commission (CFTC), which oversees derivatives markets, expects registered entities to disclose conflicts, particularly if the firm plays more than one role in a transaction, like acting as both broker and counterparty.

At the state level, regulators may apply fiduciary or best interest standards in areas like insurance sales or investment advice. Many also require firms to track and report outside business activities or potential conflicts tied to compensation.

Global Regulatory Overview

If a fintech is present in international markets, it needs to understand how other regulators approach them.

In the UK, the Financial Conduct Authority (FCA) expects firms to keep a clear, written policy on conflicts and review it regularly. The EU’s MiFID II rules go further, requiring firms to spot potential conflicts and either prevent them or explain them clearly to clients.

Similar themes appear across Asia. Authorities in Hong Kong, Singapore, and Australia have rules on personal trading, proprietary products, and situations where firms sit on both sides of a deal.

Common Types of Conflicts of Interest in Fintech

Conflicts of interest in fintech often stem from how products are structured, how firms make money, or how employees engage with outside activities. Some are obvious, others are buried in day-to-day operations.

Conflict Source | Description | Why It’s a Risk |

|---|---|---|

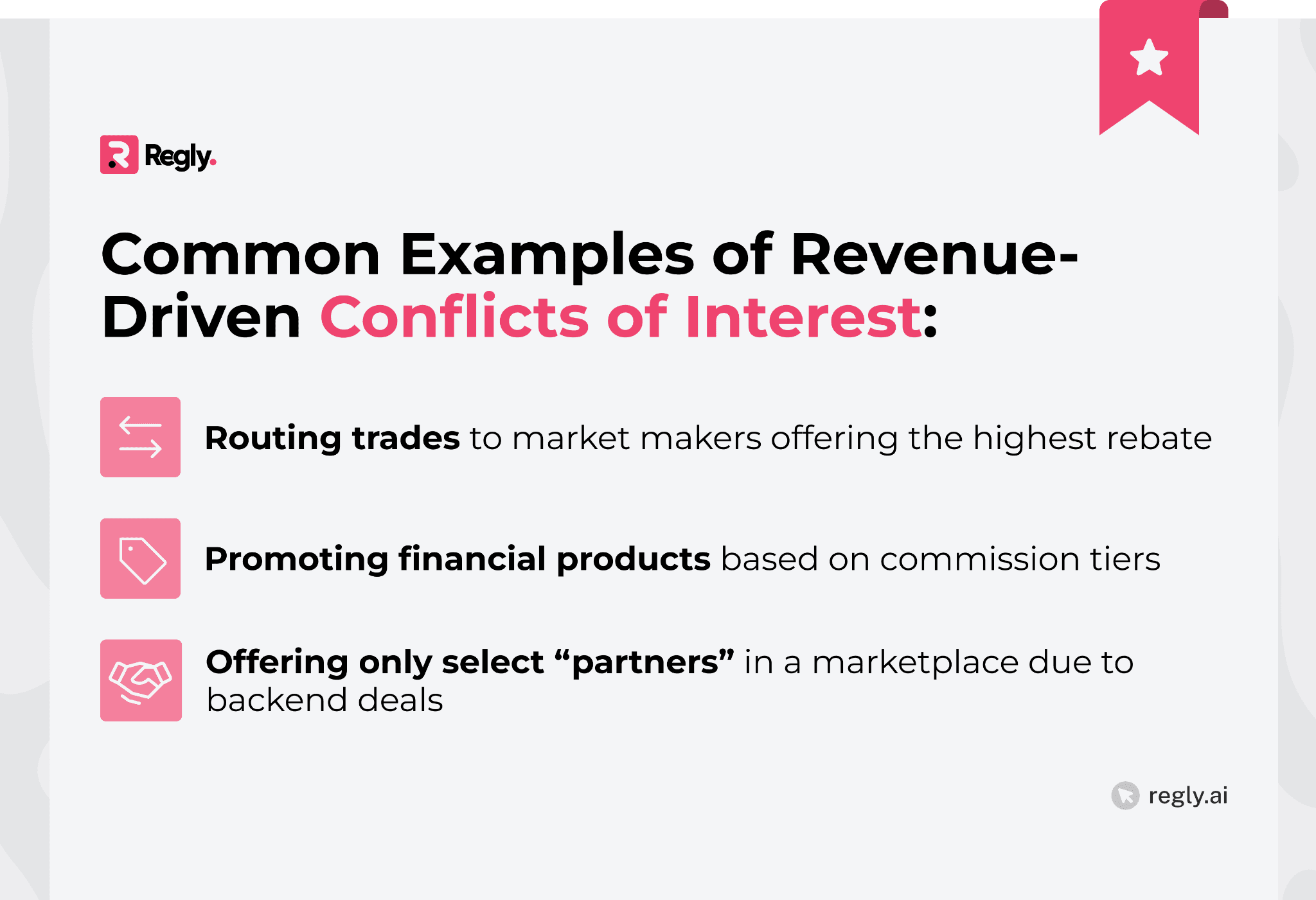

Payment for Order Flow | Routing trades to market makers that pay the highest rebates | May prioritize firm revenue over best execution for customers |

Commission-Based Product Promotion | Promoting financial products with higher commissions | Creates bias in recommendations, potentially misaligning with customer needs |

Limited Marketplace Offerings | Offering only selected partners based on backend referral or distribution deals | Reduces customer choice and may mislead users about objectivity |

Platform or UX Design Influenced by Revenue | Designing features to steer users toward more profitable products or actions | Subtly manipulates user behavior for firm benefit, often without clear disclosure |

Inadequate Incentive Testing | Failing to test how revenue incentives shape marketing, sales, or support interactions | Allows hidden bias to affect user outcomes, creating exposure during audits or reviews |

Revenue-Driven Conflicts

Many fintechs rely on business models that generate revenue through third parties. That includes payment for order flow (PFOF), referral partnerships, or product distribution arrangements that benefit the firm when users take certain actions.

The risk? Those incentives can shape platform design or sales behavior in ways that don’t clearly align with user interests. If the more profitable option isn’t the best one for the customer, and that influence isn’t disclosed, you’ve likely got a conflict worth addressing.

Disclosure helps. However, it is not enough, and compliance teams should pressure-test how incentives impact decision-making across UX, marketing, and support, and assess whether guardrails are in place.

Dual Roles and Affiliate Dealings

Fintech companies that span several business lines or have overlapping relationships with outside firms often run into conflict risks.

When a team promotes a product linked to an affiliate, or a founder sits on the board of a partner, the lines between roles can blur quickly.

Customers may not realize those connections exist, and that lack of transparency raises questions, especially if the arrangement benefits the firm more than the end user.

What matters isn’t just whether harm occurred, but whether decisions could appear biased. That perception alone can put a firm at risk if these relationships aren’t properly flagged and managed.

Outside Business Activities and Personal Interests

Conflicts of interest don’t just live at the entity level. Employee activities can create serious exposure, especially in lean fintech teams where oversight is often informal.

Outside business activities (OBAs), like serving on a board, holding a side consulting role, or launching a startup, can raise concerns if they compete with the firm’s interests or pull attention away from regulated responsibilities. These aren’t always intentional conflicts, but they still matter.

Personal trading accounts can raise red flags, even when rules aren’t technically broken. If an employee is buying or selling the same securities the firm covers, it may look like they’re using privileged information. That’s why many firms treat outside brokerage accounts as a compliance priority, especially where optics matter as much as outcomes.

Learn more about outside brokerage accounts →

That’s why many compliance programs require disclosure and pre-approval for OBAs, personal trading accounts, and certain outside financial interests. Managing this early (before conflicts turn into questions) is a core part of building a resilient compliance culture.

Learn more about outside business activities →

Information Misuse and MNPI

Material nonpublic information (MNPI) is any information about a company or security that hasn’t been publicly disclosed and could influence investment decisions. Trading on or leaking MNPI is a major regulatory risk and one of the most serious forms of conflict of interest.

In fintechs, MNPI exposure can come from multiple angles: internal access to trading data, deal pipelines, partnerships, or even client interactions. When employees use or share this information in a way that benefits themselves or someone else, it crosses a line.

Even without intent to misuse information, the combination of access and decision-making authority can be enough to trigger concerns. Strong internal controls and regular training help reduce that exposure.

Fintechs working in investment advisory, digital assets, or deal execution should build MNPI safeguards into both their compliance and product workflows, not just legal documentation.

Client-vs-Client Scenarios

Conflicts of interest don’t always involve the firm and the client. Sometimes, the friction arises between two clients, and the issue becomes how the firm chooses to navigate those situations.

This can happen when one client’s activity affects another’s outcome. For example, an advisory firm managing both sides of a funding round, or a platform giving preferential treatment to certain users based on deal volume or status. Even in digital environments, algorithmic prioritization or selective support can raise similar concerns.

The core issue is fairness. If clients are being treated unequally and the difference stems from financial benefit to the firm or favoritism, regulators may view it as a conflict. These scenarios are particularly relevant for fintechs operating marketplaces, B2B2C models, or embedded services where multiple clients rely on the same infrastructure.

Firms should be able to explain how they allocate resources, handle competing demands, and maintain neutrality in their services, especially when incentives differ behind the scenes.

Gifts, Influence, and Vendor Bias

Some conflicts start small. A vendor picks up dinner. A partner sends over event tickets.

These moments build goodwill. However, they can also make it harder to stay objective. If someone is reviewing a proposal from the same firm that just sponsored their offsite, the line gets fuzzy.

That’s where internal guardrails matter, but so does having a culture where people flag things before they become problems.

Learn more about gifts and entertainment policies →

What Regulators Expect: Disclosure, Mitigation, Elimination

Regulators don’t just want to see that a firm has identified a conflict. They expect firms to take the next step by either mitigating the risk, explaining it clearly, or walking away from the arrangement.

The right response depends on the nature of the conflict and how much it impacts users. Disclosure is a baseline, not a shield.

When Disclosure Isn’t Enough

Disclosure has its limits. If a conflict gives the firm a material benefit while putting the client at a disadvantage, regulators may expect stronger action. In some cases, that means adjusting business practices or stepping away entirely.

Clarity matters, but so does intent. A vague or buried disclosure won’t protect you if the structure itself is problematic.

The Role of Policy, Training, and Monitoring

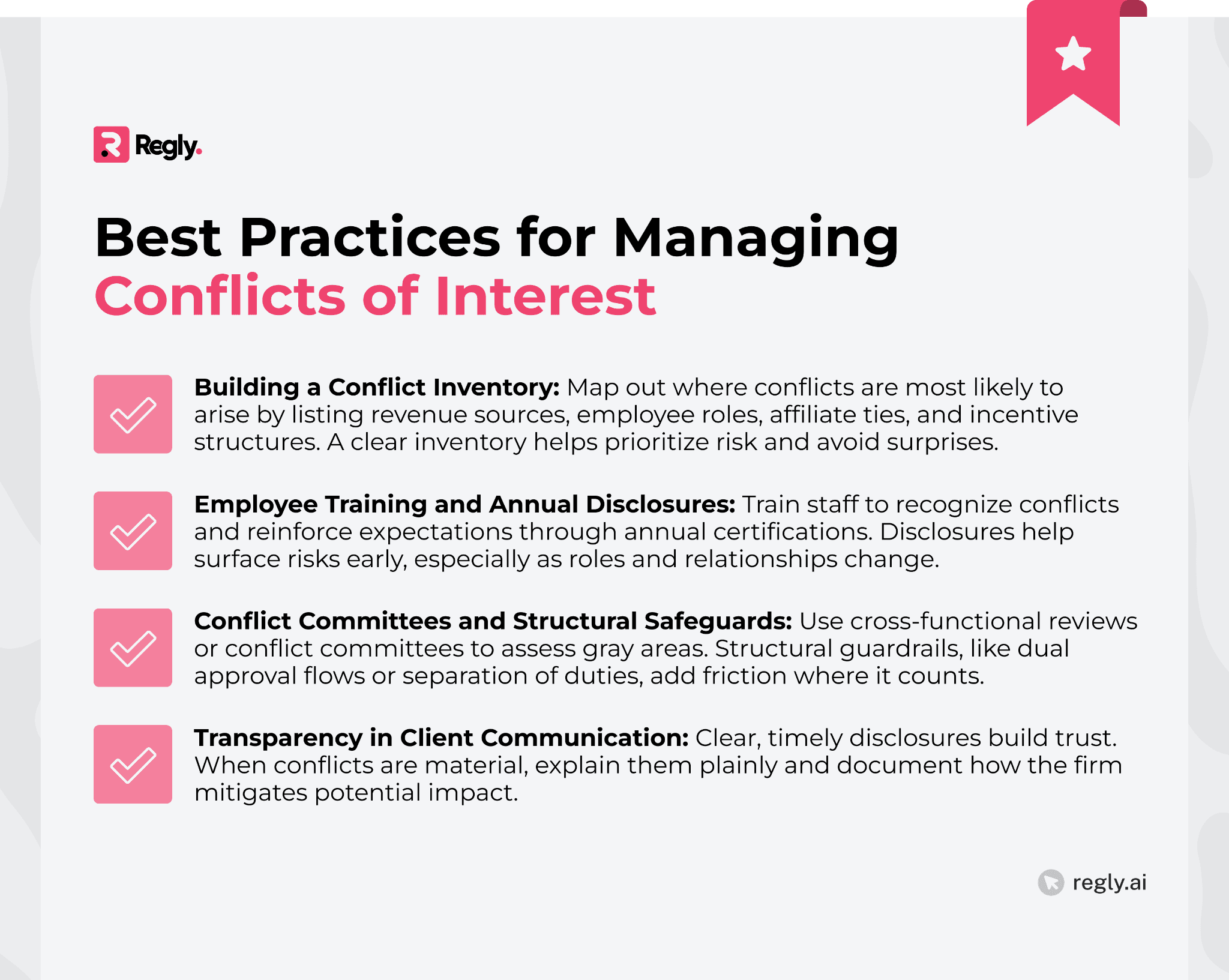

Managing conflicts of interest isn’t just about spotting them. It’s about showing your work. Regulators want to see that firms have formal policies in place, that those policies are communicated effectively, and that employee behavior aligns with them over time.

The first step is getting policies down in writing. They need to lay out what counts as a conflict, what must be disclosed, and what actions employees are expected to take. But a written policy isn’t much use if no one reads it or knows what to do with it.

That’s where tracking and training come in. Fintechs should know who’s reviewed what, when, and whether high-risk teams are getting the right guidance. Platforms like Regly Compliance make this easier by logging activity, collecting acknowledgments, and keeping updates organized without chasing PDFs or inbox threads.

Employee trade monitoring fills the gap between policy and practice. It means watching for red flags, testing controls, and following up when something doesn’t look right. That could involve trade surveillance, disclosure reviews, or pattern analysis across teams and departments. For lean fintechs, even basic checks, like reviewing employee trading activity against product coverage or checking for gaps in outside business disclosures, can go a long way.

Employee-level compliance is where breakdowns often happen. People forget to disclose side gigs, open brokerage accounts without approval, or hold roles that quietly evolve into conflicts. A strong program will make it easy to surface these things early. This guide on outside business activities and this one on outside brokerage accounts cover the most common risk areas and what to watch for.

Compliance isn’t just a policy. It’s a system. And without clear training, monitoring, and documentation, even well-intentioned firms can fall short of expectations.

See how Regly helps automate employee compliance workflows →

Fintech Compliance Challenges Related to Conflicts of Interest

Conflict of interest issues often emerge not from bad intent, but from overlooked details. As fintechs scale, even simple gaps in process or communication can create exposure.

Fast Growth, Lean Teams, and Overlooked Conflicts

Fintech moves fast. Teams scale, roles shift, and new business lines spin up quickly, all of which make it easy to miss where conflicts of interest are hiding in plain sight.

A founder juggles multiple roles. An employee quietly sits on a client’s board. A growth team pushes product in ways that blur the line between performance and pressure. These are the kinds of situations that go unnoticed when there’s no clear playbook.

In small teams, oversight often happens on the fly. A quick message, a calendar note, a mental reminder. But “informal” isn’t the same as “effective.” And when everyone’s moving fast, it’s easy for real risk to get lost in the shuffle.

Building scalable compliance doesn’t mean slowing down. But it does mean putting a few guardrails in place before you really need them.

Misunderstanding Regulatory Expectations

Not all conflict of interest issues stem from intent. Sometimes the problem is simply not knowing what regulators expect.

Many fintech leaders assume disclosure alone is enough. In reality, that’s often just the starting point. Regulators may require firms to actively mitigate or even eliminate certain conflicts, especially when there’s a clear risk to customers.

Without a strong understanding of how rules apply across SEC, FINRA, CFPB, or global equivalents, well-meaning teams can fall out of bounds. This is especially true in newer business models where regulatory guidance isn’t always black and white.

Clear internal guidance helps close that gap. So does reviewing enforcement actions and commentary to stay ahead of where scrutiny is heading. Compliance teams that stay plugged in to regulatory trends tend to spot risks sooner and course correct before it’s an issue.

Weak Monitoring and Lack of Documentation

Spotting a conflict is just the beginning. What matters later is how your team handled it, and whether there’s a clear record to show for it.

In the early stages, it's easy to rely on quick check-ins or memory. But that doesn’t hold up when regulators come asking. They’re not just interested in the result; they want the full picture: what was flagged, who reviewed it, what was decided, and how.

Good documentation doesn’t need to be complicated. It just needs to exist and be easy to find when it counts.

See how Regly’s employee compliance module can help you with monitoring and documentation →

Best Practices for Managing Conflicts of Interest

There’s no universal solution, but certain practices show up consistently in strong compliance programs.

Regly’s employee compliance module helps bring structure to all of the above. It makes it easy to assign disclosures and training, track completion, and collect attestations across your team. With built-in tools for managing outside accounts, monitoring personal trading, and storing documents in one place, Regly helps firms document what matters and spot issues early. For lean teams, it’s a scalable way to move from good intentions to clear records.

—

Conflicts of interest aren’t rare. What matters is how fintechs handle them. Having a clear process, documenting decisions, and staying ahead of evolving expectations is what separates firms that pass scrutiny from those that get stuck in it.

If your compliance program is still relying on memory, scattered emails, or siloed tools, now’s the time to tighten things up. The right structure doesn’t slow growth. It supports it.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.