Regulated fintechs eventually face a regulatory request. It might come during a routine examination, an industry sweep, or a targeted investigation. Regardless of the trigger, the result is the same: regulators want documents, data, and explanations, often on a tight timeline.

For founders and compliance teams, these requests can quickly become overwhelming. The volume of information regulators expect is substantial, and the requests often require coordination across legal, compliance, product, and engineering teams. When documentation is scattered or processes are unclear, responding can turn into a stressful, last-minute exercise.

This guide explains how to manage a regulatory request without exhausting your team. We’ll look at what regulators typically ask for, the compliance obligations behind these requests, the mistakes firms commonly make, and practical ways to build a response process that is structured, repeatable, and easier to handle over time.

What a Regulatory Request Actually Is

A regulatory request is a formal demand from a regulator asking a firm to provide documents, data, explanations, or internal records. These requests are part of routine oversight in financial services. Regulators use them to verify compliance with laws, supervisory obligations, and recordkeeping requirements.

In most cases, a regulatory request is not an accusation of wrongdoing. It is often tied to a scheduled examination, a thematic review across the industry, or follow-up questions from a regulator reviewing filings or disclosures. That said, regulators expect timely and accurate responses. Delays or incomplete submissions can quickly raise additional scrutiny.

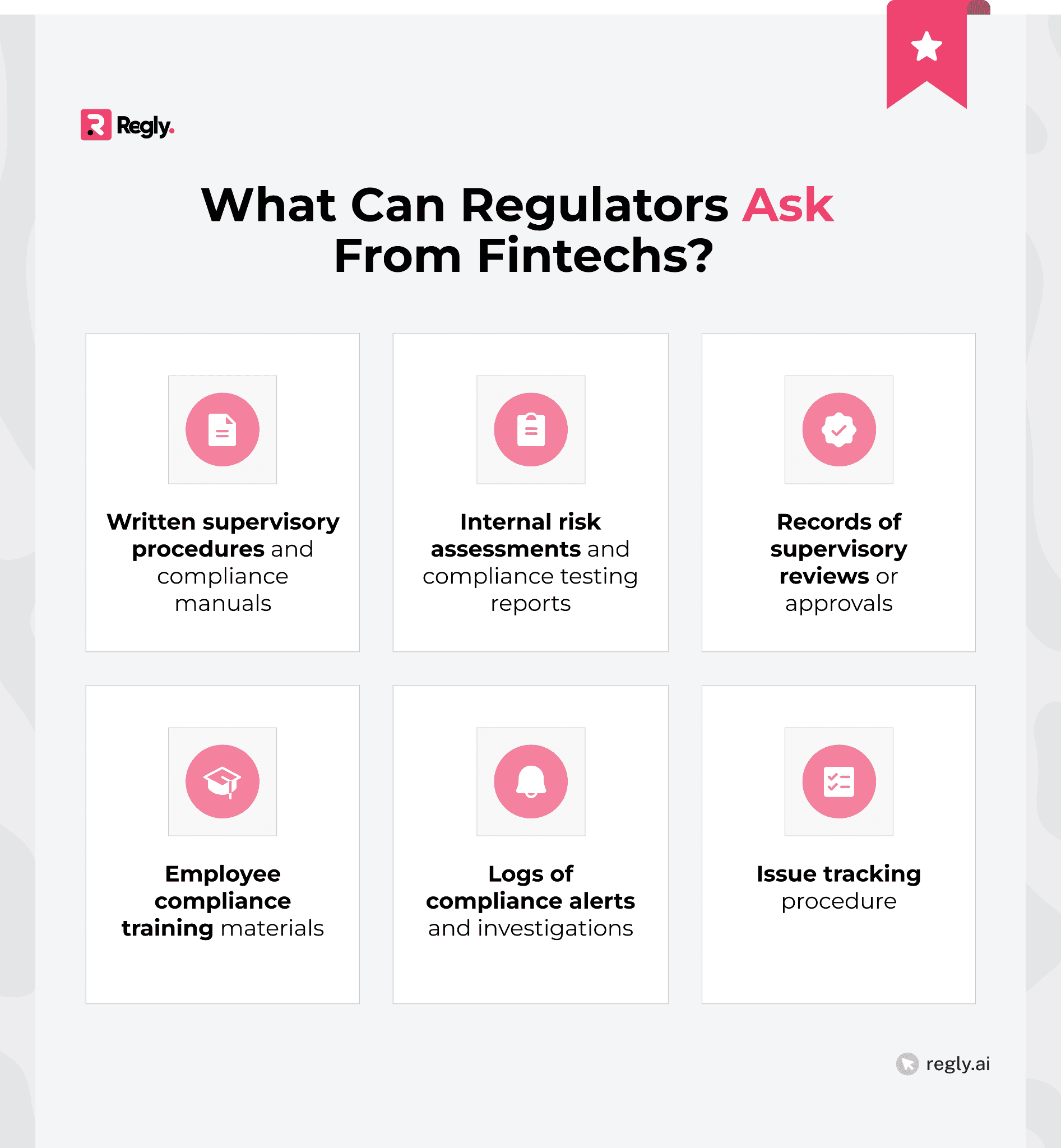

Regulatory requests usually focus on operational evidence. Regulators want to see how a firm actually runs its compliance program. That may include policies and procedures, transaction records, communications, supervisory reviews, marketing materials, or internal reports. The goal is to assess whether the firm’s written controls match its real-world practices.

Examples of Regulatory Requests in Fintech and Financial Services

Regulatory requests appear in many forms across financial services. Some arrive as part of routine examinations. Others follow customer complaints, suspicious activity, or industry-wide reviews. The format may differ, but the objective is the same: regulators want evidence that the firm is operating within the rules.

SEC Examination Document Requests: The Securities and Exchange Commission frequently issues document request lists before or during examinations of broker-dealers and investment advisers. These lists often include written supervisory procedures, compliance manuals, transaction records, and marketing materials. Regulators review these documents to understand how the firm supervises its activities and whether its internal policies align with regulatory expectations.

FINRA Rule 8210 Requests: FINRA has broad authority under Rule 8210 to request documents, data, and testimony from broker-dealers and associated persons. These requests can involve customer account activity, internal communications, supervisory reviews, or information about specific employees. Firms must respond fully and within the required timeframe. Failure to cooperate with a Rule 8210 request can itself result in disciplinary action.

CFPB Civil Investigative Demands (CIDs): The Consumer Financial Protection Bureau issues Civil Investigative Demands when investigating potential violations of consumer financial protection laws. These requests may require extensive documentation, including customer data, marketing materials, internal product documentation, and internal communications. Compared to routine examination requests, these demands are typically more formal and investigative in nature.

State Regulator Information Requests: State financial regulators regularly request information from licensed money transmitters, lending platforms, and digital asset companies. These requests often focus on licensing compliance, transaction monitoring programs, consumer complaints, and anti-money laundering procedures. Because fintech firms often operate across multiple jurisdictions, they may receive similar requests from several states at the same time.

Requests From Banking Regulators: Banking regulators such as the OCC, FDIC, and Federal Reserve may request documentation about vendor management, technology risk controls, customer onboarding procedures, and compliance monitoring during examinations of partner banks or reviews of third-party relationships. These requests often require coordination between the fintech and its banking partner to gather the relevant materials.

Why Regulatory Requests Create Operational Pressure

Regulatory requests often arrive with strict deadlines and detailed instructions. Regulators may ask for dozens of documents, datasets, and explanations at once. Even routine examinations can generate long document request lists that require coordination across multiple teams.

For fintech companies, the operational burden is often higher. Many firms run lean teams while managing complex products, partnerships, and regulatory obligations. A single regulatory request may require input from teams across:

Compliance

Legal

Product

Engineering

Customer support

Data

The requests themselves are rarely limited to one topic. Regulators may ask for policies, transaction records, communications, monitoring reports, and internal decision-making documentation. Gathering these materials quickly can be difficult if records are stored across different systems or owned by different departments.

Why Fintechs Often Feel Unprepared

Many fintech companies move quickly. Products evolve, partnerships change, and teams focus on shipping features and scaling operations. Compliance documentation and regulatory response processes often develop later, sometimes only after the first regulatory request arrives.

Another challenge is fragmented information. Key records may live in different systems across the company. Transaction data may sit with engineering, customer communications with support teams, and marketing approvals with growth teams. When regulators request these materials, assembling them quickly can become difficult.

This fragmentation is one reason many fintech compliance teams move toward centralized compliance infrastructure. Regly can aggregate compliance evidence across teams, making it easier to retrieve records, policies, and supervisory documentation when a regulatory request arrives.

Fintech firms also operate at the intersection of multiple regulatory frameworks. A single product might trigger oversight from securities regulators, consumer protection authorities, state licensing agencies, and banking partners. Each regulator may ask for slightly different documentation, even when reviewing similar activities.

This is where process discipline becomes important. Firms that build structured compliance workflows early tend to handle regulatory requests with less disruption. Platforms like Regly focus on organizing regulatory evidence and workflows, so teams are not rebuilding the response process each time a request appears.

The Regulatory Obligations Behind a Regulatory Request

A regulatory request usually reflects obligations that firms already have under financial services laws and supervisory frameworks. Regulators are not asking for new information to be created. They are asking to review the records, policies, and controls that firms are required to maintain as part of their ongoing compliance programs.

The sections below outline two of the core obligations regulators commonly review when issuing a regulatory request:

Books and Records Requirements

Most regulatory requests are tied to books and records obligations. Financial regulators require firms to maintain detailed records that document how the business operates, how transactions occur, and how compliance oversight is performed.

In the securities industry, these obligations are defined in rules such as:

SEC Rules 17a-3 and 17a-4 for broker-dealers

Advisers Act Rule 204-2 for investment advisers.

These rules require firms to maintain records for specific periods and make them available to regulators upon request. For fintech companies operating in regulated environments, books and records can include a wide range of materials:

Customer account records

Transaction and trading data

Customer communications and marketing materials

Compliance policies and procedures

Supervisory reviews and exception reports

Internal compliance testing and monitoring records

The key point is that regulators expect these records to already exist. When a regulatory request arrives, the firm is expected to retrieve it quickly and present it in an organized format.

For many fintech teams, the challenge is not the existence of records but where they live. Transaction data may sit in product databases, communications in CRM systems, and compliance documentation in separate internal tools.

Some fintech companies address this challenge by maintaining a centralized compliance evidence library. Regly allows compliance teams to map required records to regulatory obligations and store supporting documentation in one structured environment.

Supervisory and Compliance Program Requirements

Regulators also use a regulatory request to evaluate how a firm supervises its activities. Most regulated financial firms are required to maintain a documented compliance program that outlines how risks are monitored and how regulatory obligations are met.

For broker-dealers, this often includes Written Supervisory Procedures (WSPs) that describe how the firm oversees trading activity, communications, and employee conduct. Investment advisers must maintain compliance policies under the Advisers Act Compliance Rule (Rule 206(4)-7).

Payments firms, lenders, and crypto platforms may face similar expectations under state licensing laws, consumer protection rules, or bank partner oversight.

During a regulatory request, regulators often ask for documentation that shows how these controls operate in practice. They are looking for evidence that the firm follows them. When the documentation supporting supervision is incomplete or scattered across teams, responding to a regulatory request can quickly become difficult.

Consequences of Ignoring or Mishandling a Regulatory Request

Regulators expect firms to respond to a regulatory request fully and within the stated timeline. Delays, incomplete submissions, or a lack of cooperation can create additional regulatory exposure.

In some cases, the failure to respond properly becomes a separate compliance issue. For example, FINRA has taken enforcement action against firms that failed to respond to Rule 8210 requests or provided incomplete information. Regulators treat cooperation as part of a firm’s supervisory responsibilities.

Poor handling of a request can lead to several consequences:

Regulatory enforcement risk: Ignoring or failing to respond to a regulatory request may lead to disciplinary actions, fines, or other enforcement measures.

Expanded examinations: If the initial response raises questions or lacks clarity, regulators may broaden the scope of their review and request additional documents.

Repeated follow-up requests: Disorganized submissions often trigger multiple rounds of clarification and additional document requests.

Operational disruption: When responses are assembled at the last minute, teams across compliance, legal, product, and engineering may be pulled into urgent document collection efforts.

The goal is not simply to respond to a regulatory request. It is to respond clearly, completely, and efficiently, without forcing the organization into a prolonged scramble each time regulators ask for information.

Common Types of Regulatory Requests Fintechs Receive

Not all regulatory requests look the same. Some arrive during routine examinations. Others appear when regulators investigate a complaint, review a specific product, or conduct a broader industry sweep.

Understanding the type of request helps teams respond more efficiently. The scope, urgency, and level of scrutiny can vary depending on why the regulator is asking for information. Below are four common types of regulatory requests fintech companies encounter.

Examination Document Requests

These requests typically arrive during routine regulatory examinations. Regulators send a document request list that outlines the information they want to review before or during the exam.

These requests often cover multiple operational areas, including:

Compliance policies and procedures

Transaction records and activity reports

Customer communications and marketing materials

Supervisory reviews and internal controls

Employee training and compliance certifications

Examination requests can be extensive. Regulators may send additional follow-up requests as they review the materials.

Follow-Up Requests

Follow-up requests occur after regulators review an initial submission. If something is unclear or requires further explanation, regulators may request additional documents or clarification.

Common follow-up requests may involve additional transaction samples, expanded communications records, explanations of internal processes, or even clarification of compliance procedures.

Follow-up requests are common and do not necessarily indicate a problem. However, disorganized initial responses often lead to more rounds of questions.

Investigative Requests

Investigative requests usually occur when regulators are reviewing potential violations, complaints, or unusual activity. These requests tend to be more targeted than examination requests.

Regulators may ask for:

Records tied to a specific customer account

Internal communications about a product or marketing campaign

Decision-making documentation for certain business practices

Logs related to alerts, complaints, or investigations

These requests often involve closer coordination with legal and compliance teams.

Sweep Requests

Regulatory sweeps involve industry-wide information requests sent to multiple firms at the same time. Regulators use sweeps to understand how a particular product, practice, or risk area is handled across the market.

Some of the most common sweep topics are crypto asset custody practices, digital marketing and influencer promotions, payment processing risk controls, and customer onboarding and identity verification processes.

Because sweeps target many firms, regulators often request standardized data or responses.

Common Mistakes When Responding to a Regulatory Request

Many regulatory request responses become stressful, not because the request is unusual, but because the process inside the company is unclear. Teams may scramble to locate documents, interpret what regulators are asking for, or coordinate across departments.

Most of these problems follow a few predictable patterns. Understanding them helps compliance teams avoid unnecessary delays and repeated follow-up questions:

Treating the Request as a Legal Task Only

A regulatory request often starts with the legal or compliance team. But the information regulators ask for usually lives across the organization.

Product teams may hold documentation about how a feature works. Engineering may control transaction logs and system data. Customer support may have communication records.

When the response stays confined to legal or compliance, important information may be missed. A more effective approach is to involve the relevant teams early and assign clear responsibilities for gathering materials.

Scrambling to Collect Documents at the Last Minute

Many firms only start organizing materials after the regulatory request arrives. At that point, the team may be working against a tight deadline.

Documents may sit across shared drives, internal tools, product databases, and employee inboxes. Collecting them manually can take days or weeks.

This is where preparation matters. Firms that maintain organized compliance documentation and centralized record storage tend to respond more quickly and with fewer follow-up requests.

Misinterpreting What Regulators Are Asking For

Regulatory requests are sometimes written in broad terms. A request for “customer communications,” for example, may include emails, chat logs, marketing materials, and in-app messages.

If the scope is misunderstood, the firm may submit only part of the requested information. Regulators will then ask for additional materials, which slows the review process.

Carefully reviewing the request and clarifying ambiguous items early can prevent unnecessary back-and-forth.

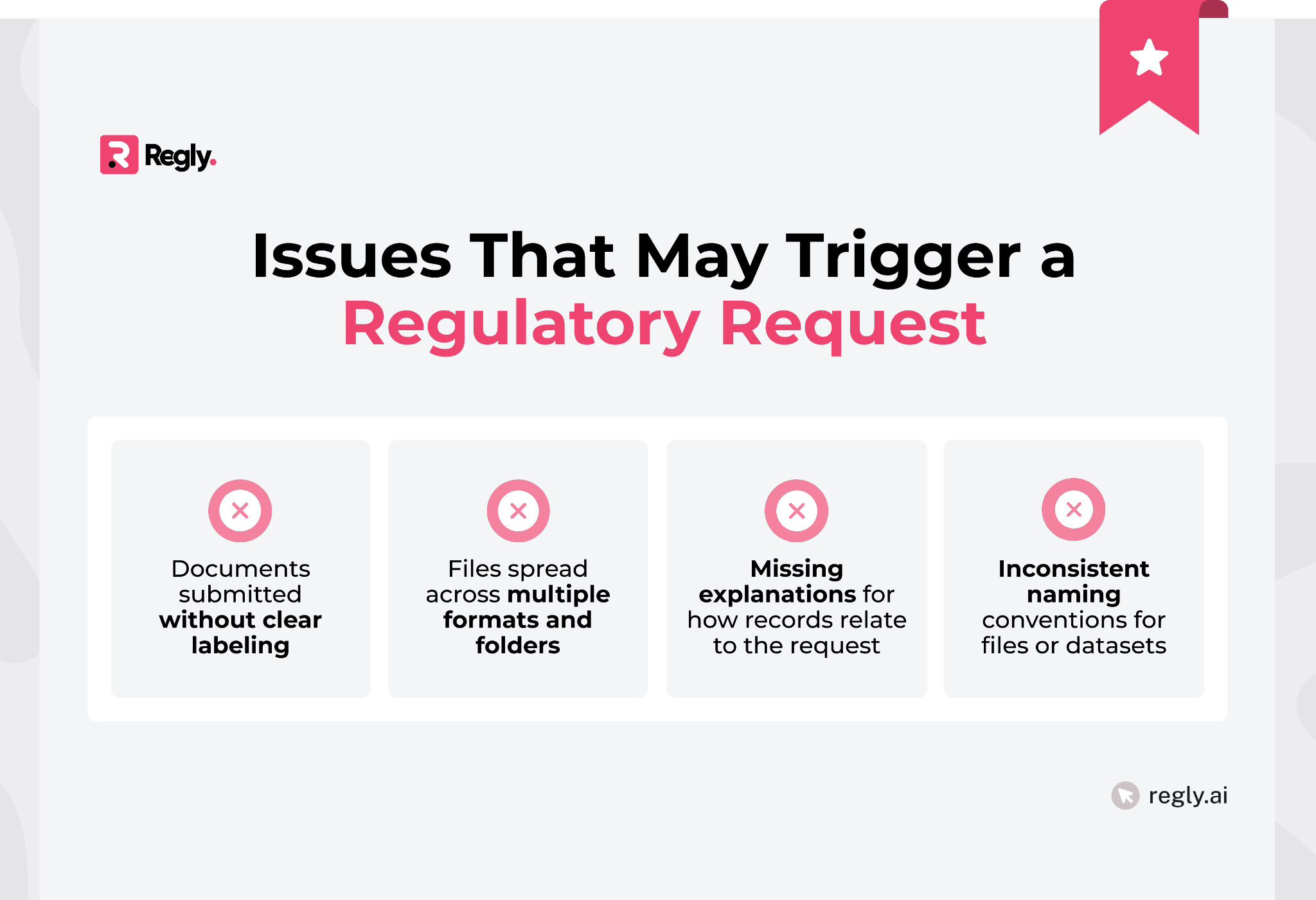

Submitting Incomplete or Poorly Organized Responses

How information is presented matters. Even when firms provide the correct documents, disorganized submissions can create confusion for regulators. A well-structured submission makes the regulator’s review easier. It also reduces the likelihood of additional regulatory requests for clarification.

How to Manage a Regulatory Request Without Burning Out

The key is to treat the response as a structured process, not a one-off scramble. Most successful responses follow a similar workflow. The firm defines the scope, assigns responsibility, collects documents in a coordinated way, and tracks what has been submitted.

The steps below outline a practical process many compliance teams use when managing a regulatory request:

Step 1: Understand the Scope of the Regulatory Request

Start by reviewing the request carefully. Regulators often group requests by topic, such as communications, transactions, marketing, or supervision.

Create a working list of what the regulator is asking for. This helps the team avoid missing items and reduces the risk of follow-up questions.

Many teams find it useful to convert the request into a tracking table:

Request Item | Owner | Source System | Status |

|---|---|---|---|

Customer communications | Customer support | CRM | In progress |

Transaction records | Operations/Finance | Transaction Processing System | Pending |

Compliance policies | Compliance | Internal docs | Completed |

Breaking the request into clear tasks helps teams manage the workload more efficiently. Some compliance teams manage this process manually in spreadsheets. Others use compliance workflow platforms such as Regly, which allow firms to centralize regulatory request information.

Step 2: Assign a Response Lead

A regulatory request should have one central response lead, typically within compliance or legal.

This person coordinates the response, communicates with regulators, and keeps internal teams aligned. Without a clear owner, requests often stall or move in multiple directions at once.

The response lead typically handles:

Communication with the regulator

Internal coordination across teams

Tracking deadlines and deliverables

Reviewing submissions before they are sent

This role is less about doing all the work and more about keeping the process organized.

Step 3: Build a Centralized Document Collection Process

Documents for a regulatory request often live across multiple systems. Pulling them together quickly requires a single collection point.

Many firms create a temporary response workspace, such as a shared folder or internal compliance platform, where all documents are uploaded and reviewed.

Useful practices include:

Creating folders that match the regulator’s request list

Using consistent file naming conventions

Keeping a short explanation for complex datasets

Tracking which version of a document has been submitted

For fintech companies managing frequent regulatory requests, some teams move this process into dedicated compliance tools.

Request a demo for your fintech here →

Step 4: Track Deadlines and Deliverables

Regulatory requests usually come with clear response timelines. Some items may require additional time if they involve complex datasets or archived records.

A simple internal timeline can help prevent last-minute pressure:

Task | Owner | Deadline |

|---|---|---|

Collect customer communications | Support team | Day 5 |

Export transaction logs | Engineering | Day 7 |

Review compliance policies | Compliance | Day 8 |

Final review and submission | Response lead | Day 10 |

Tracking progress in this way gives compliance teams visibility into what is complete and what still requires attention.

Step 5: Document What Was Submitted

Every regulatory request response should leave a clear internal record. This record should have:

The original regulatory request

The documents submitted

Any explanations or written responses

The dates of submission

Follow-up questions from regulators

Maintaining this documentation makes future regulatory requests easier to manage. If regulators ask similar questions later, the firm already has a reference point for its prior response.

Building an Internal Process for Future Regulatory Requests

Handling one regulatory request is manageable. Handling them repeatedly without a defined process is where teams begin to feel the strain. Here’s how to build a process internally to tackle regulatory requests with ease:

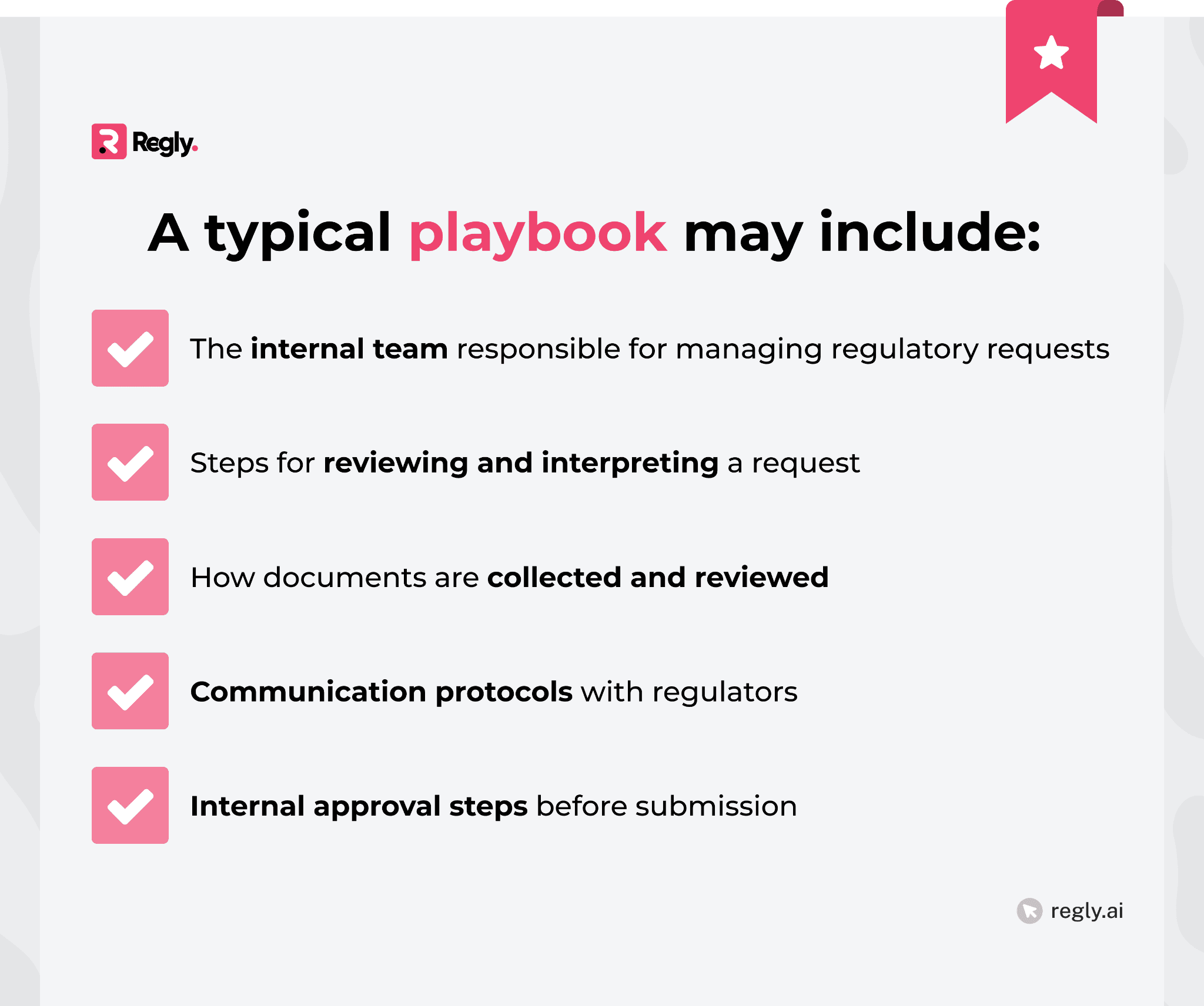

Maintain a Regulatory Response Playbook

A regulatory response playbook outlines how the company handles incoming requests from regulators. It doesn’t need to be complicated. The goal is to document the process so teams do not have to reinvent it each time. Having this documented reduces confusion and shortens response times.

Keep Compliance Documentation Organized

Many regulatory requests involve materials that firms are already required to maintain. Policies, supervisory procedures, training records, and monitoring reports should be stored in a structured and accessible format.

Common practices include:

Maintaining a central repository for compliance policies

Version control for supervisory procedures

Organized storage for compliance testing reports

Clear documentation of internal reviews and approvals

When compliance documentation is organized in advance, regulatory requests become retrieval exercises rather than reconstruction projects.

Establish Cross-Team Communication Channels

Regulatory requests rarely involve a single team. Product, engineering, compliance, legal, and customer operations often all contribute information.

Clear communication channels help reduce delays. Some firms assign department contacts who handle regulatory requests for their area. Others create internal response channels where updates and document requests are tracked.

This structure makes it easier to gather information quickly when regulators ask for it.

Conduct Mock Regulatory Requests

Some firms periodically run internal mock regulatory requests to test their response process.

This exercise may involve creating a sample document request list and asking internal teams to collect the materials within a set timeframe. The goal is to identify gaps in documentation, unclear responsibilities, or delays in retrieving information.

Mock requests can reveal issues that might otherwise surface during a real examination. Addressing those gaps early helps reduce stress when regulators send an actual request.

Tools That Help Teams Manage Regulatory Requests

Responding to a regulatory request usually involves gathering information from different systems, coordinating across departments, and keeping track of deadlines. When these steps are handled manually, the process can become slow and difficult to manage.

Many fintech teams rely on a small set of operational tools to organize documents, assign responsibilities, and maintain a clear record of what was submitted to regulators. Here are four types of tools that can support you in this:

Compliance Management Systems

Compliance management systems (CMS) help centralize the documentation that regulators typically request. Instead of storing policies, procedures, and compliance testing reports across multiple drives or tools, these systems keep them in one structured environment.

Typical materials stored in these systems are compliance policies and procedures, written supervisory procedures, and compliance testing results. In some cases, training records and certifications are also stored within the CMS.

For fintech companies, specialized platforms can simplify this process. Tools like Regly focus on organizing regulatory evidence and compliance workflows so teams can retrieve documents quickly when regulators ask for them.

Document and Evidence Tracking

A regulatory request often requires documents from multiple teams. Engineering may export transaction logs, marketing may provide campaign materials, and customer support may produce communication records.

Without a shared tracking structure, teams can easily lose visibility into what has already been collected.

Many firms create a document request tracker that links each regulatory item to a document owner and storage location. This type of structure helps teams track progress and identify missing documents early.

Workflow and Task Management

Workflow tools help organize this process by assigning tasks and tracking progress. A typical regulatory request workflow might include steps such as:

Reviewing the request and breaking it into items

Assigning owners for each document request

Collecting documents from internal systems

Reviewing materials before submission

Recording what was provided to the regulator

Even simple task tracking tools can make a large regulatory request easier to manage.

Audit Trail and Reporting Tools

After the response is submitted, it is important to maintain a clear record of what was sent. Regulators may follow up months later, asking about the same information.

Maintaining this record saves time when similar regulatory requests appear in future examinations. It also helps compliance teams demonstrate how the response process was handled.

Regulatory Request Trends Fintechs Should Be Watching

Regulatory requests are evolving as fintech business models become more complex. Regulators are asking for more operational data, deeper documentation of internal controls, and clearer explanations of how products work.

Several trends are shaping the types of regulatory requests fintech companies receive today:

Increased Regulatory Data Requests

Regulators are requesting larger datasets than in the past. Instead of reviewing a few transaction samples, they may ask for full transaction exports, monitoring logs, or customer activity datasets.

These requests are often used to analyze patterns across large volumes of activity. Compliance teams may need to work closely with engineering or data teams to extract the requested information in the correct format.

Focus on Crypto and Digital Asset Activities

Crypto and digital asset firms are facing growing scrutiny from regulators. Requests often focus on how platforms handle custody, transaction monitoring, market activity, and disclosures.

Regulators may ask for:

Wallet and custody procedures

Trade execution data

Listings review processes for digital assets

Monitoring systems used to detect suspicious activity

Even fintech companies that are not primarily crypto-focused may receive questions if they interact with digital asset services.

Greater Scrutiny of Marketing and Customer Communications

Marketing practices have become a major focus area for regulators. Requests frequently include materials related to advertising, influencer campaigns, and customer disclosures.

Regulators can often request to review website and app marketing content, social media promotions, customer onboarding disclosures, and influencer agreements. In these cases, the aim is to evaluate whether marketing statements accurately reflect the product and associated risks.

Requests for Technology and Vendor Documentation

As fintech companies rely on complex technology stacks and external vendors, regulators increasingly request documentation about technology infrastructure and third-party oversight.

The requests can be around vendor risk assessments or incident response procedures. Regulators may also ask for system access controls and monitoring logs to understand how firms are managing operational risk across their technology stack.

Practical Checklist: Preparing for Your Next Regulatory Request

Preparing for a regulatory request is easier when the key records and processes already exist. The checklist below highlights the materials regulators commonly ask for during examinations or investigations:

Compliance policies and supervisory procedures are current

Customer records and transaction data can be retrieved quickly

Customer communications are archived and searchable

Marketing materials and disclosures are documented

Compliance monitoring and testing records are maintained

Employee compliance training records are available

Vendor and third-party documentation is organized

There is a defined process for handling a regulatory request

Previous regulatory request responses are archived

If several of these items require manual searching across systems, that is often a sign that the regulatory response process needs additional structure before the next request arrives.

Maintain a centralized compliance evidence repository so documents requested by regulators can be retrieved quickly. Regly helps fintech teams structure this process across policies, monitoring reports, and operational records.

—

Regulatory requests are a normal part of operating in financial services. What determines how disruptive they become is not the request itself, but how prepared the organization is to respond.

For fintech companies, the challenge is often operational. Records may sit across product systems, compliance tools, internal drives, and communication platforms. Without a structured workflow, responding to a regulatory request can quickly pull multiple teams away from their core responsibilities.

This is where purpose-built compliance infrastructure can help. Regly, developed by the regulatory experts behind InnReg, was designed specifically for regulated fintech companies. The platform helps teams organize compliance documentation, track regulatory evidence, and manage response workflows in one place.

If your team is looking for a more structured way to handle regulatory requests and other compliance tasks, exploring how Regly fits into your compliance operations may be a practical next step.

Ready to Get Started?

Schedule a demo today and find out how Regly can help your business.